- Vaxcyte recently reported in The Lancet Infectious Diseases that its 31-valent pneumococcal conjugate vaccine candidate VAX-31 showed strong immune responses and a safety profile similar to Prevnar 20 in a Phase 1/2 study of 1,015 adults aged 50 and older, and has since advanced the high-dose regimen into the OPUS Phase 3 adult program.

- An important insight from these data is that VAX-31 met or exceeded regulatory immunogenicity criteria for all 31 serotypes at higher doses while covering substantially more disease-causing strains than existing adult pneumococcal vaccines, potentially broadening protection if future trials and regulators support its use.

- We’ll now explore how VAX-31’s progression into the OPUS Phase 3 adult program could influence Vaxcyte’s investment narrative and long-term outlook.

We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Vaxcyte Investment Narrative Recap

To own Vaxcyte, you need to believe that broader-coverage pneumococcal vaccines like VAX-31 can clear late stage trials, earn supportive guidelines and eventually convert into commercial uptake, while the company manages heavy pre revenue spending. The newly published Phase 1/2 adult data strengthens the near term OPUS Phase 3 catalyst by reinforcing both safety and immunogenicity, but it does not remove the central risk of high cash burn and the need to fund multiple large trials and manufacturing buildout.

Among recent updates, the February 2026 follow on equity filings of up to US$500 million matter most here, because they sit alongside rising R&D and manufacturing costs and a stated cash runway to at least the end of 2028. Against the strong VAX-31 data now in The Lancet Infectious Diseases and the ongoing OPUS-1, OPUS-2 and OPUS-3 trials, this additional capital highlights how dependent the story remains on future clinical success to support those investments.

Yet even with encouraging VAX-31 data in hand, the biggest issue investors should be aware of is the risk that rising costs and potential delays could...

Read the full narrative on Vaxcyte (it's free!)

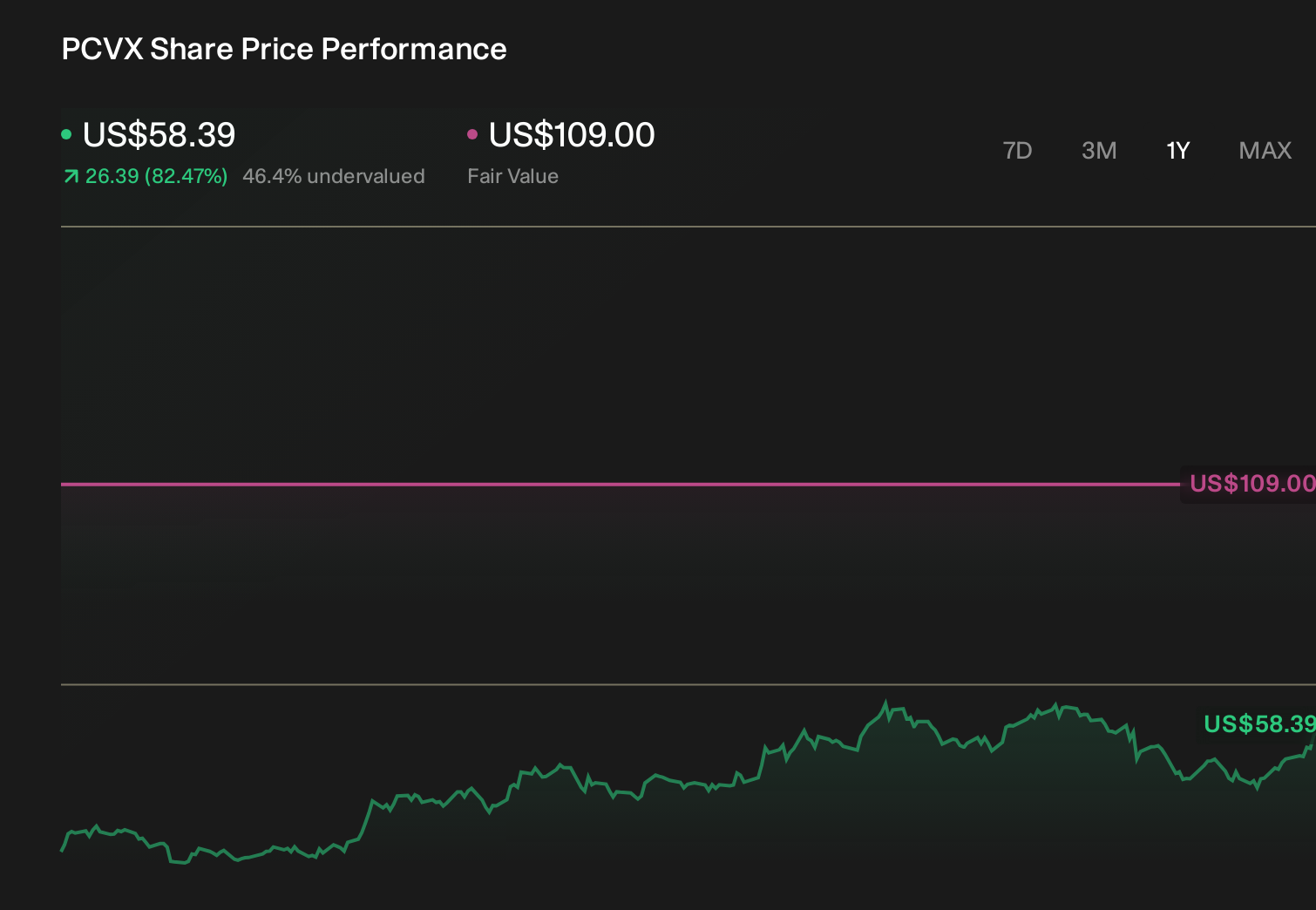

Vaxcyte’s narrative projects $224.6 million in revenue and $28.1 million in earnings by 2029. This implies an earnings increase of about $795 million from -$766.6 million today.

Uncover how Vaxcyte's forecasts yield a $109.00 fair value, a 99% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already factoring in about US$424 million of revenue and roughly US$46 million of earnings by 2029, so this new VAX-31 data could either reinforce that faster OPUS Phase 3 path or, if issues emerge later, highlight how ambitious those forecasts were compared with the more cautious views on trial, policy and manufacturing risk.

Explore 4 other fair value estimates on Vaxcyte - why the stock might be worth less than half the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Vaxcyte research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free Vaxcyte research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Vaxcyte's overall financial health at a glance.

No Opportunity In Vaxcyte?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com