- In March 2026, Ormat Technologies completed two Rule 144A convertible note offerings totaling US$750,000,000, including US$600,000,000 of 1.5% senior unsecured notes and US$150,000,000 of zero-coupon senior unsecured notes, both due March 15, 2031, while also advancing new storage operations and long-term geothermal contracts.

- Beyond bolstering its funding base, Ormat’s launch of the Shirk storage facility and higher-priced, extended Casa Diablo-IV PPAs deepen contracted visibility across geothermal and battery assets.

- We’ll now examine how Ormat’s US$750,000,000 in new convertible notes may reshape its investment narrative around growth and financing.

We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Ormat Technologies Investment Narrative Recap

To own Ormat Technologies, you need to believe in contracted, long-term cash flows from geothermal and storage projects that justify its current valuation and capital intensity. The new US$750,000,000 in Rule 144A convertible notes strengthens liquidity for that build out, but it does not materially change the near term balance between growth execution as a key catalyst and high leverage as a central risk.

Among the recent announcements, the Shirk 80MW / 320MWh storage facility stands out as most connected to this financing story. Shirk’s 15 year agreement with the City of Riverside and eligibility for a 40% Investment Tax Credit, supported by Ormat’s hybrid tax equity structure with Morgan Stanley Renewables, show how new capital can be tied directly to contracted storage revenues and tax benefits that support the growth narrative.

Yet, beneath these long term contracts, investors should be aware of the risk that Ormat’s high capital needs and leverage could become more challenging if funding costs or...

Read the full narrative on Ormat Technologies (it's free!)

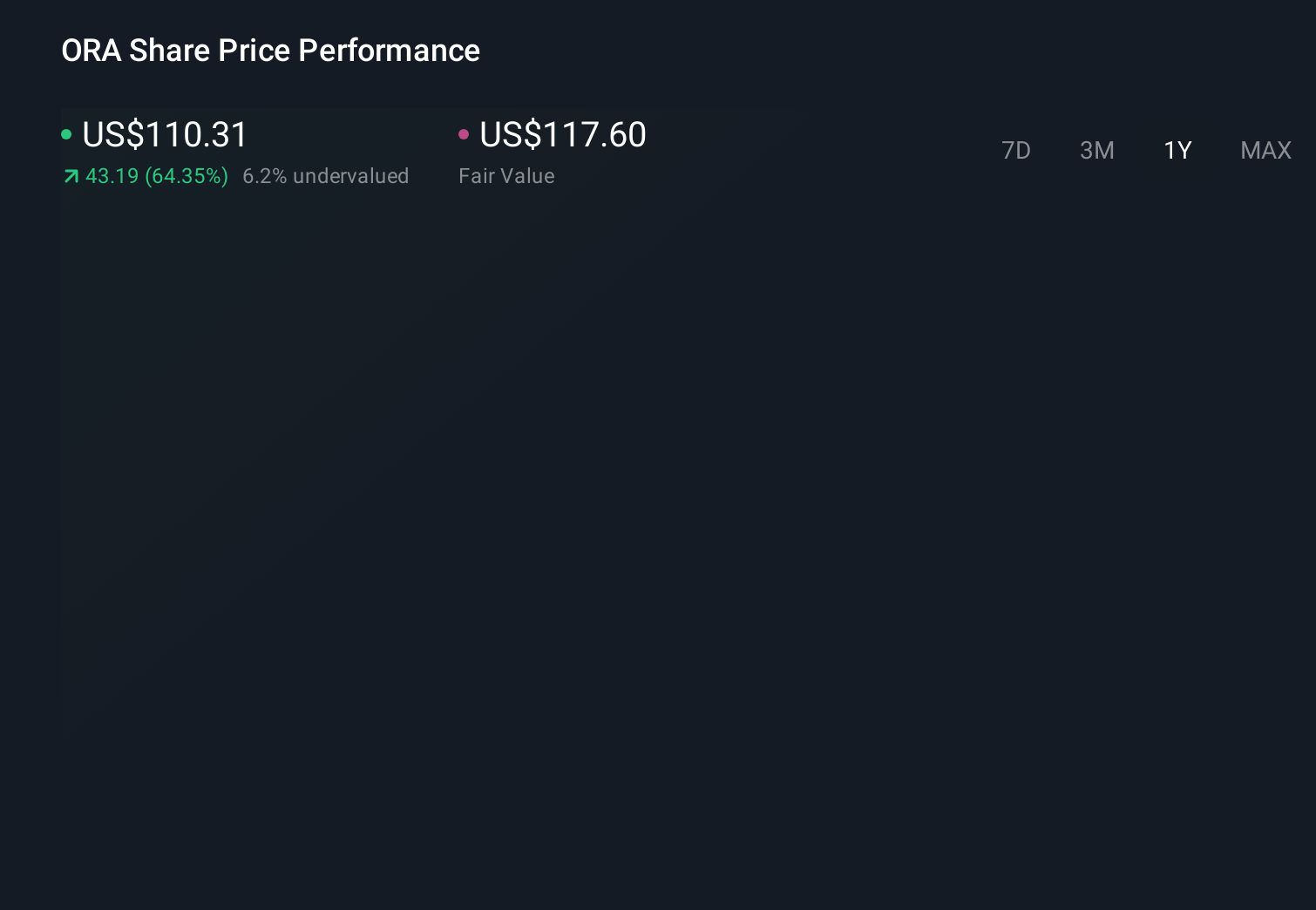

Ormat Technologies' narrative projects $1.3 billion revenue and $215.3 million earnings by 2029. This requires 8.5% yearly revenue growth and an earnings increase of about $91 million from $123.9 million today.

Uncover how Ormat Technologies' forecasts yield a $128.00 fair value, a 20% upside to its current price.

Exploring Other Perspectives

Three fair value estimates from the Simply Wall St Community span a very wide band, from about US$9 to US$128 per share, underlining how differently individual investors see Ormat’s prospects. Against that spread, the recent US$750,000,000 in convertible notes and growing roster of long term PPAs put the focus squarely on whether Ormat can translate funding and contracts into durable earnings and balance sheet resilience over time.

Explore 3 other fair value estimates on Ormat Technologies - why the stock might be worth as much as 20% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Ormat Technologies research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Ormat Technologies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ormat Technologies' overall financial health at a glance.

Interested In Other Possibilities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- This technology could replace computers: discover 24 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com