- In March 2026, IQVIA Holdings launched IQVIA.ai, a unified agentic AI platform built with NVIDIA technologies to embed healthcare-grade AI directly into life sciences workflows across clinical, commercial, and real-world domains.

- This collaboration positions IQVIA.ai as a centralized “digital command center” that ties together intelligent agents, automation, and decision support within a single, compliance-focused architecture for regulated healthcare settings.

- Next, we’ll explore how IQVIA.ai’s agent-based architecture and NVIDIA partnership could reshape IQVIA’s investment narrative around AI-enabled differentiation.

Explore 24 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

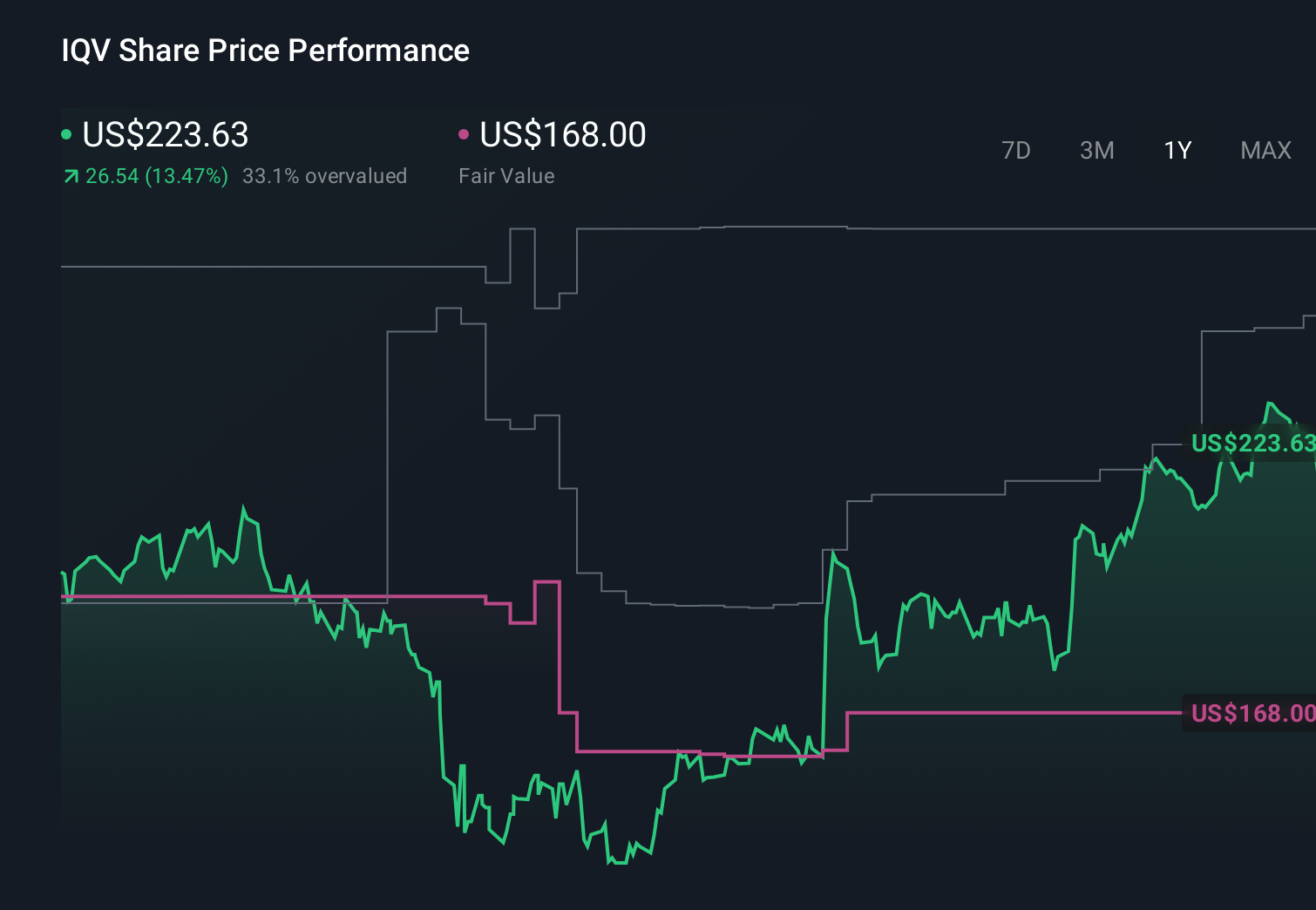

IQVIA Holdings Investment Narrative Recap

To own IQVIA, you need to believe its data, software, and CRO services can stay essential to global drug development while withstanding pricing pressure, margin headwinds, and high leverage. The launch of IQVIA.ai with NVIDIA directly targets the key near term catalyst of AI-enabled differentiation, but it does not by itself remove the biggest risk today: intense CRO competition that pressures pricing and profitability.

Among recent announcements, the 2024 expansion of IQVIA’s partnership with Salesforce on Life Sciences Cloud is particularly relevant. Together with IQVIA.ai, it highlights a push to embed IQVIA’s data and AI directly into pharma workflows, which could reinforce switching costs and support demand, even as client budgets stay sensitive and CRO pricing remains tight.

Yet even with IQVIA.ai, investors should be aware that rising CRO competition and thinner margins could still...

Read the full narrative on IQVIA Holdings (it's free!)

IQVIA Holdings' narrative projects $18.4 billion revenue and $1.8 billion earnings by 2028.

Uncover how IQVIA Holdings' forecasts yield a $250.00 fair value, a 50% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already modeling IQVIA’s earnings rising to about US$2.3 billion by 2028, and see IQVIA.ai plus proprietary agents as a potential accelerator, while others worry that mounting CRO price pressure and client concentration could blunt those expectations, so it is worth comparing how different forecasts might shift after this news.

Explore 4 other fair value estimates on IQVIA Holdings - why the stock might be worth as much as 88% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your IQVIA Holdings research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free IQVIA Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate IQVIA Holdings' overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

- Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

- AI is about to change healthcare. These 36 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com