Carrollton hub plans put Fastenal’s logistics build out in focus

Fastenal (FAST) is starting construction of a much larger Southeast regional operations and logistics center in Carrollton, Georgia, replacing its Atlanta facility and introducing next generation warehouse technologies to support future distribution needs.

See our latest analysis for Fastenal.

The new Carrollton project comes as Fastenal’s share price sits at US$44.89, with a 90 day share price return of 7.32% and a 1 year total shareholder return of 18.91%. This points to momentum that has been building rather than fading over the past few years.

If this logistics expansion has you thinking about where else supply chains and infrastructure might create opportunities, it could be worth scanning 25 power grid technology and infrastructure stocks

With Fastenal trading close to its US$44.99 analyst price target and the stock already delivering strong multi year returns, the key question is whether today’s valuation leaves any upside on the table or if markets are already fully pricing in future growth.

Most Popular Narrative: 0.1% Undervalued

Fastenal’s most followed narrative pegs fair value at about $44.92, almost exactly in line with the last close at $44.89. This makes the Carrollton build out especially interesting for what it signals about long term execution.

The company is expanding its Fastenal Managed Inventory (FMI) technology which currently represents over 43% of revenue, aiming to enhance revenue growth by increasing efficiency in customer supply chains. Fastenal aims to increase its digital footprint to represent 66-68% of sales, up from 61%, potentially boosting revenue by optimizing purchasing and operational efficiency.

Want to understand why such a small gap between price and fair value still attracts attention? The story leans heavily on compound revenue growth, firmer margins, and a rich future earnings multiple that is usually reserved for higher growth sectors. Curious how those pieces fit together into a single valuation narrative.

Result: Fair Value of $44.92 (ABOUT RIGHT)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still clear pressure points, including tariff and freight costs, as well as shifts toward digital purchasing that could challenge margins and the current high P/E narrative.

Find out about the key risks to this Fastenal narrative.

Another View On What The Price Is Saying

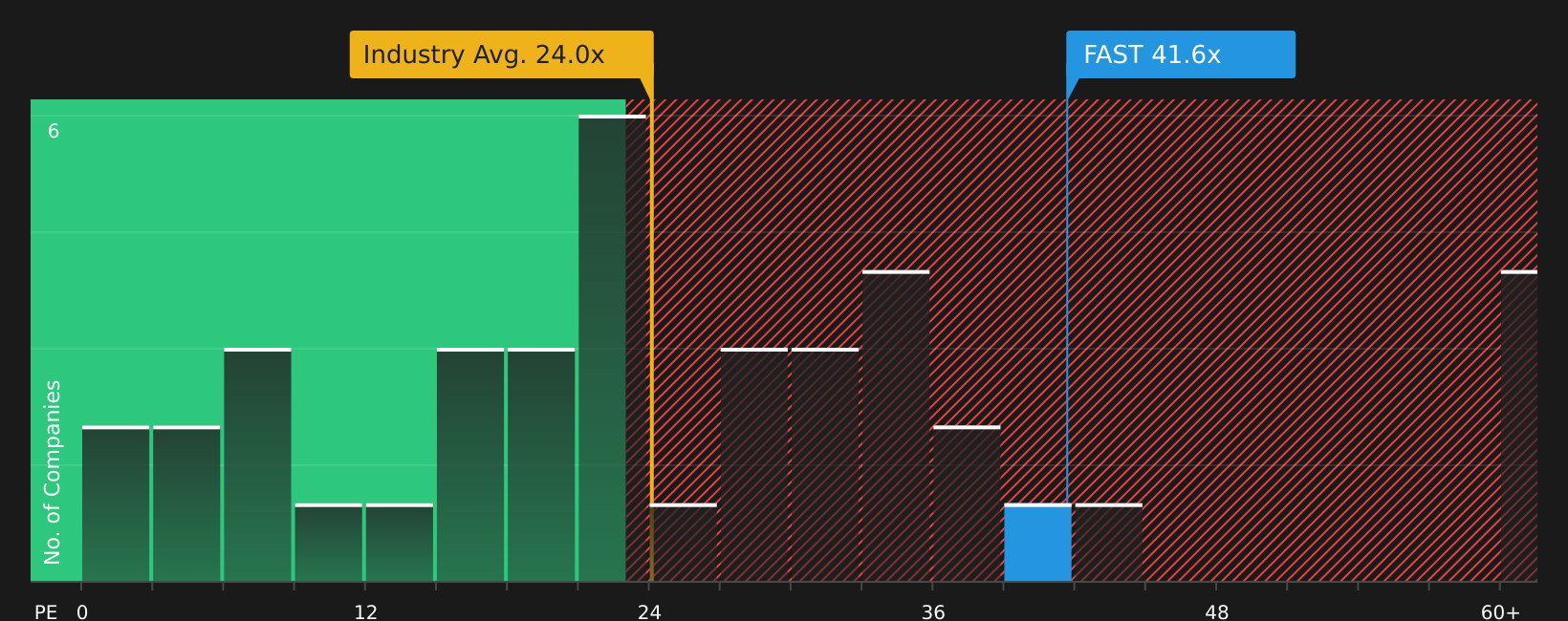

While the narrative based fair value pins Fastenal around $44.92, the current P/E of 41x tells a tougher story. That is richer than the estimated fair ratio of 32.3x, the US Trade Distributors average of 20.5x, and a 23x peer average. This points to clear valuation risk if sentiment cools.

For a closer look at how those earnings multiples stack up against what the numbers imply as a fair ratio, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If all of this feels finely balanced between opportunity and concern, now is the time to look at the details yourself and decide where you stand, starting with 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If you stop at just one stock, you risk missing out on other opportunities that might fit your goals even better, so broaden your radar with a few focused screens.

- Spot potential underpriced quality by scanning 58 high quality undervalued stocks that pair fundamentals with appealing valuations.

- Strengthen your income watchlist by checking out 13 dividend fortresses that put regular payouts front and center.

- Prioritize resilience by reviewing 73 resilient stocks with low risk scores designed to keep overall portfolio risk in check.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com