- CNH Industrial N.V.’s Board of Directors has declared a reduced cash dividend of US$0.10 per share, subject to shareholder approval at the 2026 Annual General Meeting, with a proposed record date of May 21, 2026, and expected payment on May 29, 2026.

- Around the same time, CNH Industrial was removed from the FTSE All-World Index (USD), a change that can influence institutional ownership patterns and trading flows.

- Next, we’ll examine how the reduced dividend proposal shapes CNH Industrial’s existing investment narrative and expectations for margin improvement.

This technology could replace computers: discover 24 stocks that are working to make quantum computing a reality.

CNH Industrial Investment Narrative Recap

To own CNH Industrial today, you need to believe that its mix of agricultural and construction equipment, plus growing tech offerings, can ultimately support better profitability despite recent earnings pressure. The reduced US$0.10 dividend and removal from the FTSE All-World Index may unsettle income-focused and index-tracking holders, but do not fundamentally alter the near term focus on margin recovery and execution risks around weaker North American ag demand and elevated inventories.

The clearest link to this news is CNH’s recent capital return pattern. Alongside an ongoing US$500.00 million buyback program, the proposed cut in the annual dividend highlights a shift in how cash is being returned and preserved. For investors watching catalysts around margin improvement and earnings stabilization, this combination of lower cash payouts and continued repurchases raises fresh questions about how confidently management sees the current profit profile and balance sheet flexibility.

Yet beneath CNH’s tech story and margin ambitions, investors should be aware of how rising tariffs and input costs could still...

Read the full narrative on CNH Industrial (it's free!)

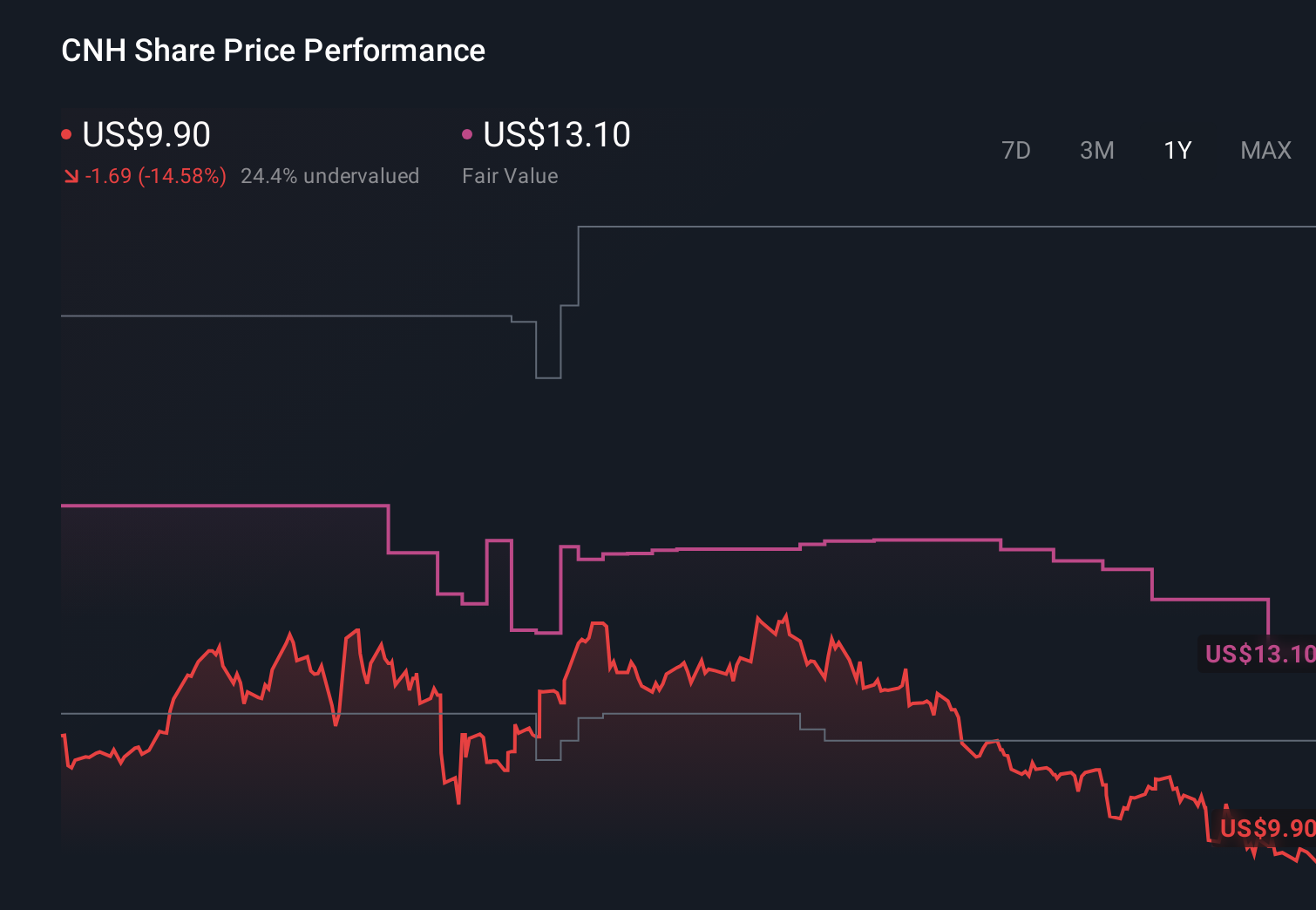

CNH Industrial's narrative projects $18.7 billion revenue and $1.6 billion earnings by 2028.

Uncover how CNH Industrial's forecasts yield a $13.99 fair value, a 25% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting earnings to climb toward about US$2.3 billion by 2028, yet today’s dividend cut and index removal may prompt you to rethink how resilient that view really is.

Explore 6 other fair value estimates on CNH Industrial - why the stock might be worth less than half the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your CNH Industrial research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free CNH Industrial research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CNH Industrial's overall financial health at a glance.

Interested In Other Possibilities?

Our top stock finds are flying under the radar-for now. Get in early:

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- AI is about to change healthcare. These 36 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com