Over the last 7 days, the United States market has experienced a 1.6% decline, though it remains up by 15% over the past year with earnings projected to grow by 16% annually. In this context, identifying small-cap stocks that are potentially undervalued and exhibit insider action can offer intriguing opportunities for investors seeking to navigate these dynamic market conditions.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Enovis | NA | 0.6x | 46.58% | ★★★★★★ |

| Financial Institutions | 8.4x | 2.6x | 45.40% | ★★★★★☆ |

| AVITA Medical | NA | 1.7x | 35.86% | ★★★★★☆ |

| Franklin Financial Services | 10.7x | 2.6x | 1.26% | ★★★★☆☆ |

| Union Bankshares | 9.6x | 2.0x | 23.55% | ★★★★☆☆ |

| Ultralife | NA | 0.6x | 30.38% | ★★★★☆☆ |

| German American Bancorp | 13.9x | 4.6x | 47.02% | ★★★☆☆☆ |

| New Peoples Bankshares | 9.4x | 2.2x | 41.69% | ★★★☆☆☆ |

| Aldeyra Therapeutics | NA | NA | 42.05% | ★★★☆☆☆ |

| Douglas Emmett | 106.9x | 1.6x | 42.97% | ★★★☆☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

1st Source (SRCE)

Simply Wall St Value Rating: ★★★★☆☆

Overview: 1st Source is a financial institution primarily engaged in commercial banking operations, with a market capitalization of approximately $1.52 billion.

Operations: The primary revenue stream is commercial banking, generating $421.22 million. Operating expenses are a significant cost component, with general and administrative expenses reaching $188.12 million in the most recent period. The net income margin has shown an upward trend from 24.25% to 37.24% over the analyzed periods, indicating improved profitability relative to revenue growth.

PE: 10.6x

1st Source, a smaller player in the financial sector, showcases potential value with their recent financial performance. For 2025, they reported net income of US$158.28 million, up from the previous year's US$132.62 million, and increased earnings per share to US$6.41 from US$5.36. Insider confidence is evident with share purchases during this period and a completed buyback program totaling 233,033 shares for $13.95 million by December 2025. Despite modest net charge-offs of $0.28 million in Q4 2025, their consistent dividend growth—now at $0.40 per share—signals strength amidst challenges faced by similar-sized companies in the industry.

- Get an in-depth perspective on 1st Source's performance by reading our valuation report here.

Examine 1st Source's past performance report to understand how it has performed in the past.

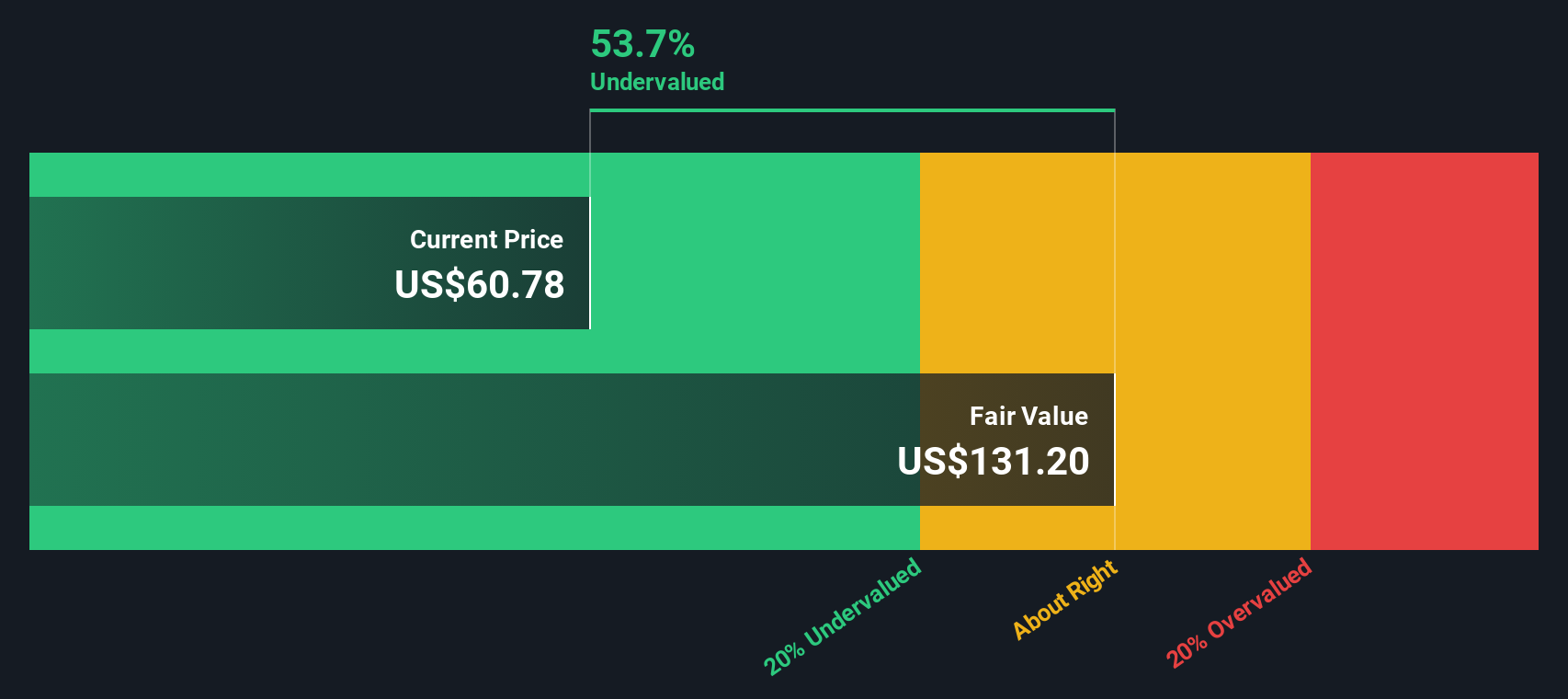

Enovis (ENOV)

Simply Wall St Value Rating: ★★★★★★

Overview: Enovis is a company that specializes in providing innovative medical technology solutions, focusing on reconstructive and prevention and recovery segments, with a market cap of approximately $2.73 billion.

Operations: Enovis generates revenue primarily from its Reconstructive and Prevention and Recovery segments, totaling approximately $2.25 billion. The company's gross profit margin has shown an upward trend, reaching 60.88% in the latest period. Operating expenses are significant, with General & Administrative expenses being a major component, contributing to the overall cost structure.

PE: -1.1x

Enovis, a smaller player in the market, has been drawing attention with its recent activities and financial performance. Despite reporting a net loss of US$1.18 billion for 2025, sales increased to US$2.25 billion from the previous year. The company recently completed a significant share buyback program, repurchasing over 6 million shares since 2018 for US$200 million, reflecting strategic confidence in its future prospects. Enovis forecasts revenue growth to reach up to US$2.37 billion in 2026, signaling potential upward momentum amidst ongoing challenges and industry dynamics.

- Take a closer look at Enovis' potential here in our valuation report.

Explore historical data to track Enovis' performance over time in our Past section.

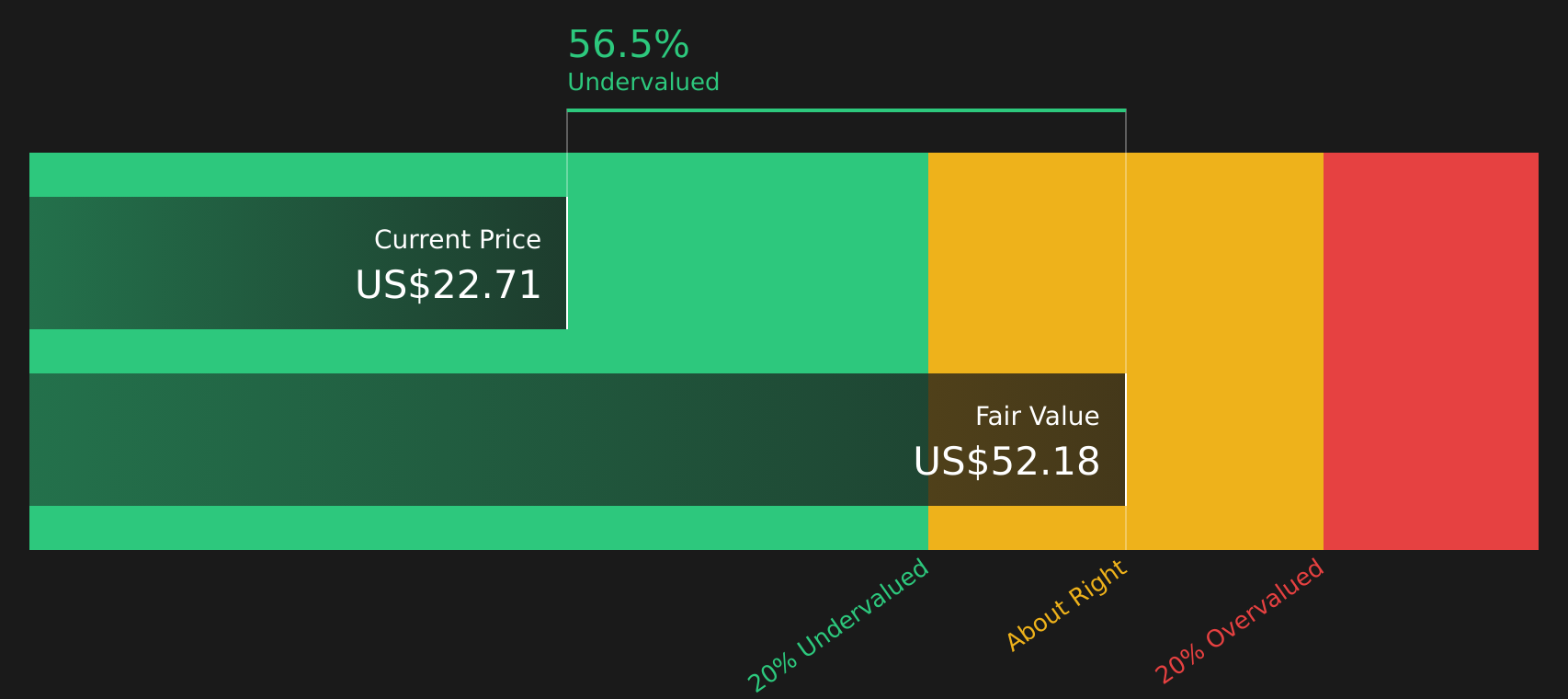

Horace Mann Educators (HMN)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Horace Mann Educators is an insurance company that provides life, retirement, property and casualty, and supplemental group benefits services with a market cap of approximately $1.13 billion.

Operations: The company's revenue streams are primarily driven by Property & Casualty, Life & Retirement, and Supplemental & Group Benefits segments. Over the years, it has experienced fluctuations in its gross profit margin, with recent figures showing a rise to 38.12% as of December 2025. Operating expenses have shown an upward trend, reaching $410.9 million by the end of 2025.

PE: 10.7x

Horace Mann Educators, known for its commitment to supporting educators, has shown insider confidence with recent share purchases. From October to December 2025, the company repurchased 153,925 shares for US$6.84 million. Financially, Horace Mann reported a revenue increase to US$1.7 billion in 2025 and net income rose to US$162 million from the previous year’s US$103 million. Their new Horace Mann Club initiative enhances educator support through financial tools and wellness programs at no cost, reflecting their dedication beyond financial metrics.

- Dive into the specifics of Horace Mann Educators here with our thorough valuation report.

Evaluate Horace Mann Educators' historical performance by accessing our past performance report.

Summing It All Up

- Access the full spectrum of 63 Undervalued US Small Caps With Insider Buying by clicking on this link.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com