- Earlier this week, F.N.B. Corporation expanded its public finance offerings by launching municipal bond underwriting through its broker-dealer subsidiary, FNB America Securities LLC, aimed at helping municipalities fund large, long-term projects with tax-exempt debt.

- This move broadens F.N.B.’s capital markets capabilities and uses its data-driven market intelligence to structure tailored financing solutions for local governments and nonprofits.

- We’ll now examine how adding municipal bond underwriting to F.N.B.’s capital markets platform might influence its diversified, fee-based investment narrative.

AI is about to change healthcare. These 36 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

F.N.B Investment Narrative Recap

To own F.N.B., you need to believe in a regional bank that leans heavily on digital innovation and growing fee-based businesses to complement traditional lending. The new municipal bond underwriting offering supports that diversified, fee-income story, but does not materially change the immediate focus on credit quality, especially in commercial real estate, or the ongoing cost pressure from technology investments.

This underwriting launch ties most closely to F.N.B.’s broader Capital Markets build-out, including the 2025 acquisition of Raptor Partners. Together, these moves deepen F.N.B.’s fee-generating capabilities across investment banking, loan syndications, and now municipal finance, which all sit alongside its Clicks-to-Bricks digital push and could influence how resilient earnings appear relative to core lending and deposit competition.

However, investors should also be aware that F.N.B.’s regional concentration and exposure to local economic swings could...

Read the full narrative on F.N.B (it's free!)

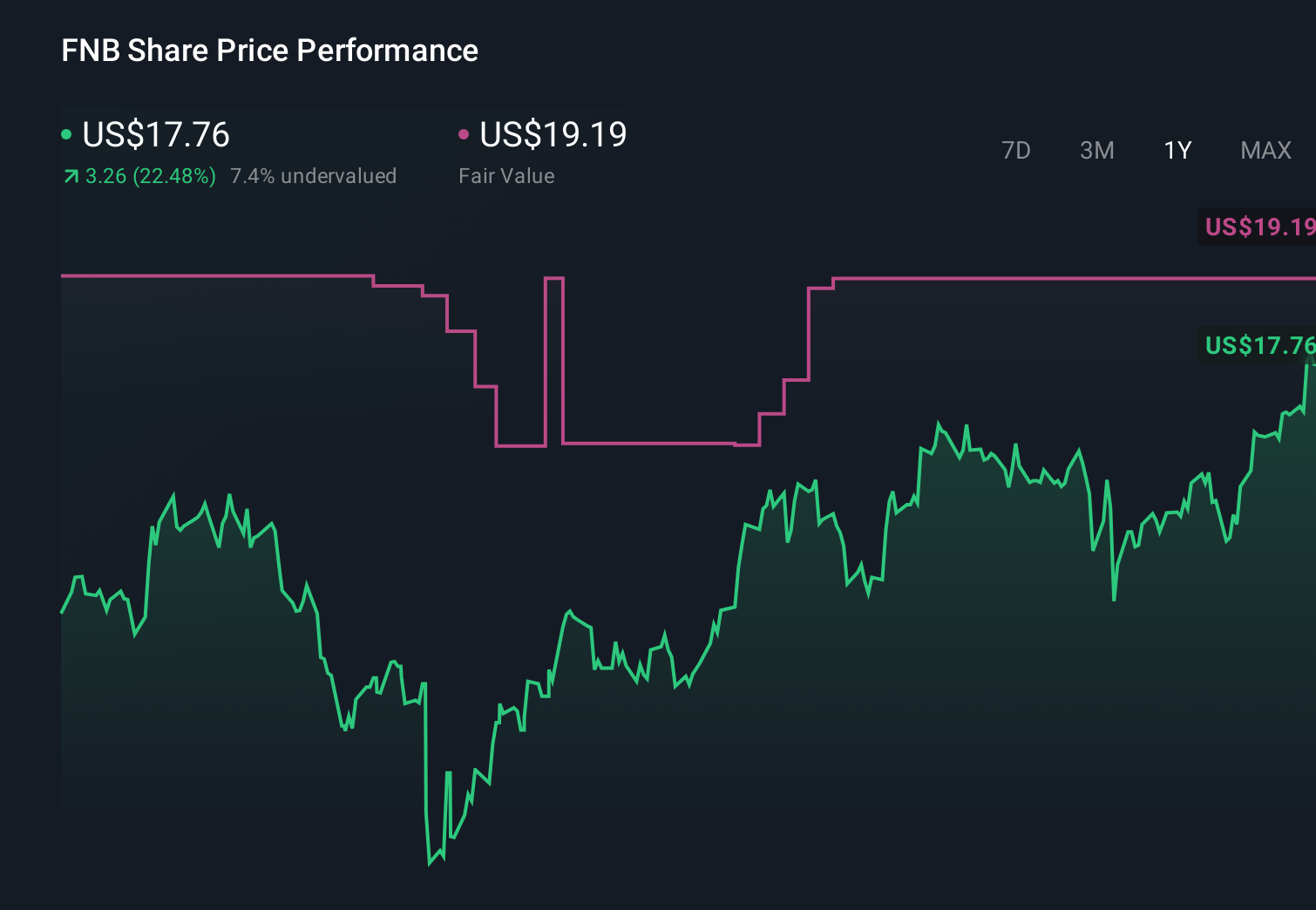

F.N.B's narrative projects $2.3 billion in revenue and $764.9 million in earnings by 2029.

Uncover how F.N.B's forecasts yield a $20.06 fair value, a 21% upside to its current price.

Exploring Other Perspectives

Four members of the Simply Wall St Community currently see F.N.B.’s fair value between US$20.06 and US$63.31, with views spread across this wide range. When you weigh those opinions against F.N.B.’s growing, diversified Capital Markets and digital initiatives, it underlines why taking in several perspectives on the bank’s future earnings mix can be useful.

Explore 4 other fair value estimates on F.N.B - why the stock might be worth over 3x more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your F.N.B research is our analysis highlighting 6 key rewards that could impact your investment decision.

- Our free F.N.B research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate F.N.B's overall financial health at a glance.

No Opportunity In F.N.B?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Rare earth metals are the new gold rush. Find out which 26 stocks are leading the charge.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com