Event context and recent performance

Delek Logistics Partners (DKL) has drawn investor attention after recent trading saw a 1.9% decline in the latest session, following a period where the unit price has moved higher over the past 3 months and year.

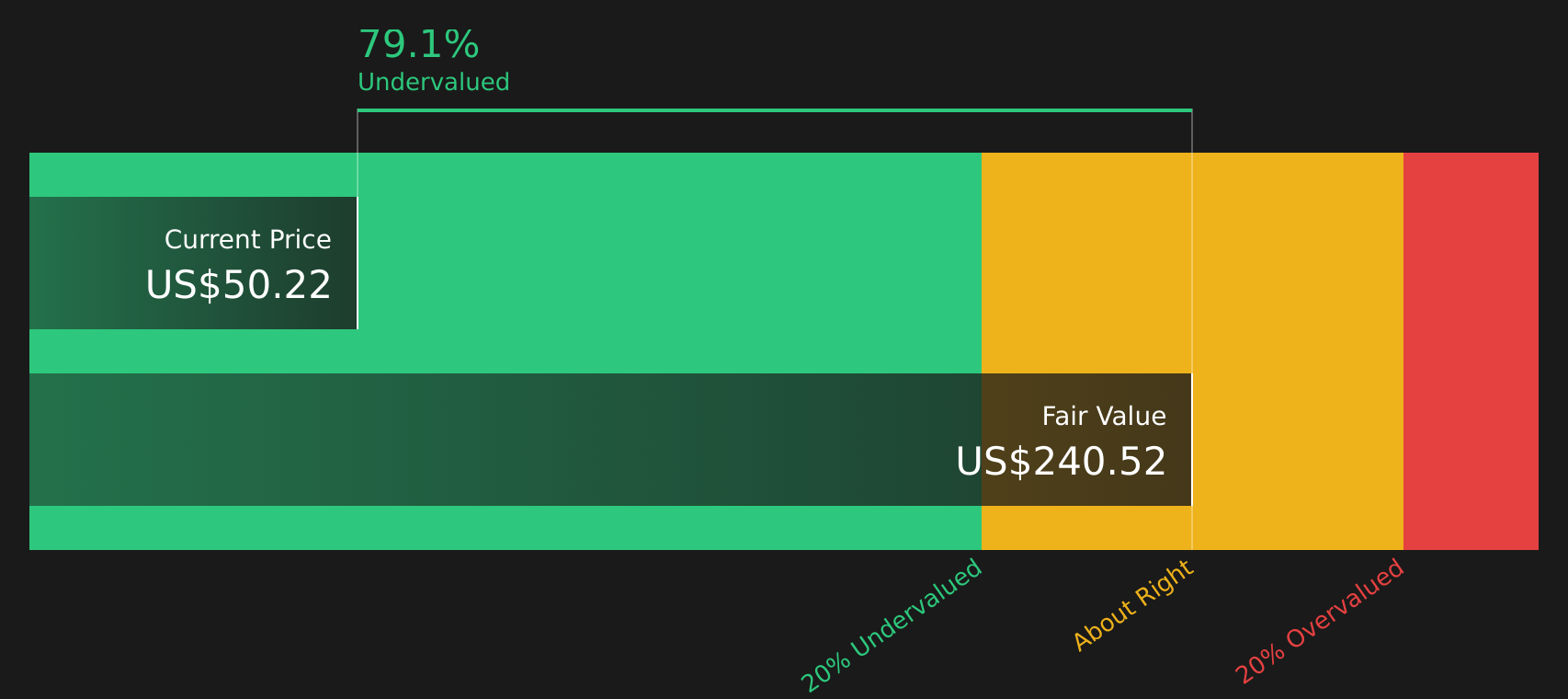

See our latest analysis for Delek Logistics Partners.

While the latest 1.9% daily share price decline to US$53.12 has cooled near term sentiment, the 90 day share price return of 18.44% and 1 year total shareholder return of 34.55% suggest momentum has been building rather than fading.

If you are weighing DKL alongside other energy related ideas, it can be helpful to scan a wider field of power and infrastructure names through 26 power grid technology and infrastructure stocks

With DKL trading around US$53.12, sitting above the current analyst price target and supported by an intrinsic value score of 4 and an intrinsic discount flag, investors may wonder if there is still a buying opportunity here or if the market is already pricing in future growth.

Most Popular Narrative: 13% Overvalued

The widely followed fair value estimate for Delek Logistics Partners sits at $47, compared with the latest close at $53.12. This narrative suggests the market is pricing in a premium that depends heavily on future project execution and cash flows.

The full commissioning and expected ramp to capacity of the new Libby 2 gas plant in the Delaware Basin, along with associated investments (amine unit and AGI wells), positions Delek Logistics to capitalize on rising energy demand and stable domestic energy infrastructure needs, likely boosting gathering and processing volumes, EBITDA, and revenue growth.

This raises questions about what revenue path, margin uplift, and future P/E level are implied in that fair value, and how far out Libby 2 cash flows contribute to the narrative.

Result: Fair Value of $47 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on Libby 2 ramping as planned and customer volumes holding up, with any delays or contract pushback potentially undermining those cash flow assumptions.

Find out about the key risks to this Delek Logistics Partners narrative.

Another View on Value

The analyst narrative points to Delek Logistics Partners trading around 13% above a fair value of $47, yet the SWS DCF model paints a very different picture, with the units priced at $53.12 versus an estimated future cash flow value of $369.37, implying deep undervaluation. Which lens do you trust more when cash flows and sentiment disagree?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

With sentiment split between premium pricing and deep value, it makes sense to check the underlying data yourself and decide where you stand. If you want a clear snapshot of both the potential upside and the concerns investors are watching, start with these 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If DKL has your attention, do not stop here. Broaden your watchlist with other focused ideas that could suit different goals and risk levels.

- Target income first by reviewing companies in the 12 dividend fortresses that combine higher yields with business models designed to keep those payouts coming.

- Hunt for value opportunities by scanning the screener containing 26 high quality undiscovered gems where solid fundamentals may not yet be fully appreciated by the wider market.

- Prioritise resilience by checking the 67 resilient stocks with low risk scores so you are not missing businesses that score well on financial strength and downside protection.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com