Republic Services (RSG) is back in focus after recent commentary highlighted a slowdown in demand, with annualized revenue growth of 5.3% over the past two years trailing its five year trend.

See our latest analysis for Republic Services.

Recent trading reflects that cooling demand story, with a 30 day share price return of a 2.6% decline and a 1 year total shareholder return of an 8.6% decline. This contrasts with a much stronger 5 year total shareholder return of 130.1% and suggests that long term momentum has eased for now.

If this shift in momentum has you looking beyond waste services, it could be a time to scout for opportunities in robotics and automation via our stock screener, starting with 33 robotics and automation stocks.

So with demand cooling, recent returns under pressure and the share price sitting below some valuation estimates, is Republic Services now trading at a discount, or is the market already pricing in all the growth ahead?

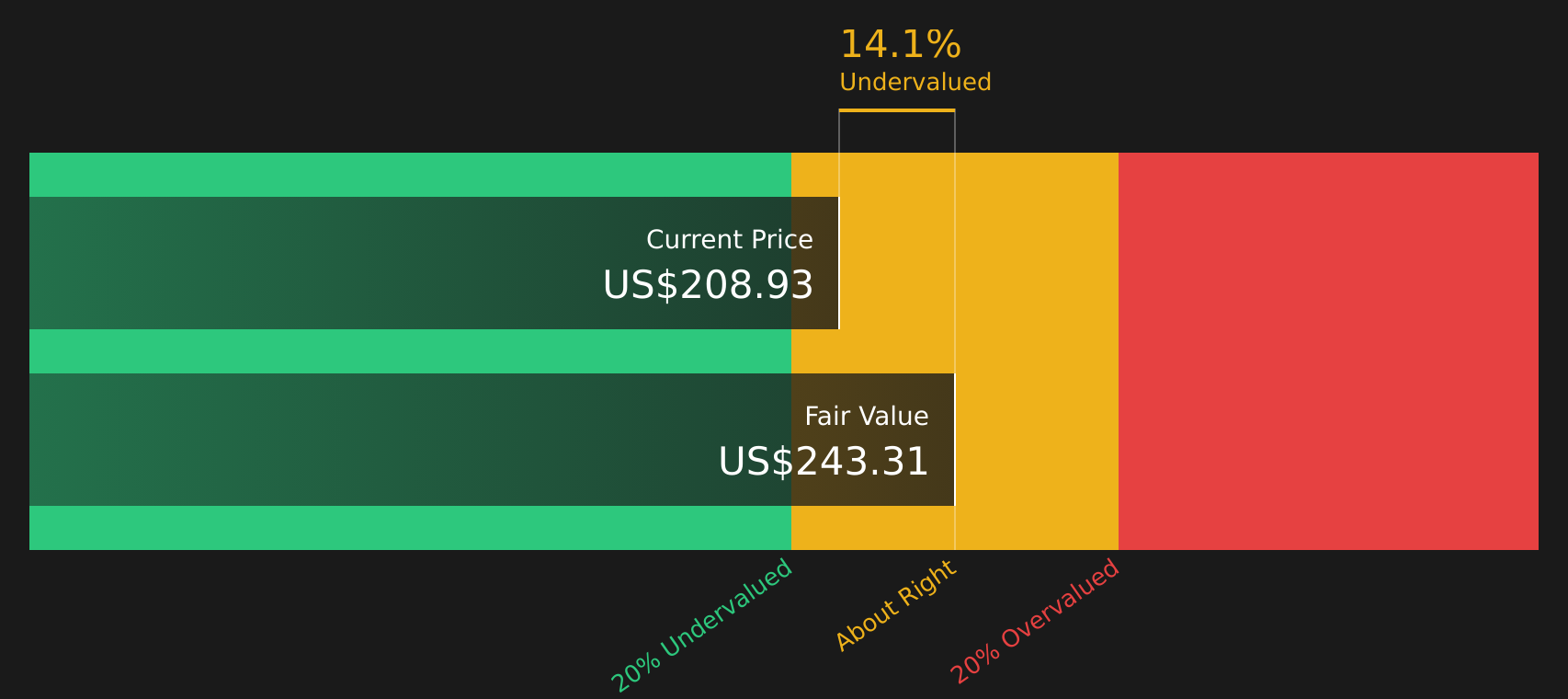

Most Popular Narrative: 12.1% Undervalued

At a last close of $215.83 versus a narrative fair value of $245.46, Republic Services is framed as undervalued, with that gap tied to clear growth projects and margin assumptions.

Sustainability efforts such as the development of Polymer Centers and the Blue Polymers joint venture could drive future revenue growth by enhancing plastic circularity and decarbonization. These operations are expected to contribute to earnings starting in the second half of 2025.

Curious what kind of revenue path, margin lift and future earnings multiple are needed to support that higher fair value? The full narrative lays out specific growth, profitability and valuation assumptions behind the $245.46 figure.

Result: Fair Value of $245.46 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are clear watchpoints, including softer construction and manufacturing volumes, as well as execution risks around the planned US$1b acquisition pipeline, that could challenge this upbeat narrative.

Find out about the key risks to this Republic Services narrative.

Another Angle On Valuation

While the narrative fair value suggests Republic Services is 12.1% undervalued at $215.83 versus $245.46, the current P/E of 31.2x sends a different signal. It sits above the Commercial Services industry at 22.6x and above a fair ratio of 27.1x, which points to valuation risk if sentiment cools.

RSG also trades below the Simply Wall St estimate of future cash flow value at $262.62, so the story looks more generous when viewed through the SWS DCF model. The question is which anchor you trust more when expectations change quickly: earnings multiples or long term cash flows.

Look into how the SWS DCF model arrives at its fair value.

Next Steps

Mixed signals on value and sentiment can be confusing. Check the underlying data, weigh the trade offs, and see the full picture with 3 key rewards and 1 important warning sign

Ready to hunt for your next idea?

If you stop at one stock, you miss the bigger opportunity set. Put a few minutes into fresh ideas and give yourself more options to work with.

- Spot potential value plays with strong fundamentals by scanning 61 high quality undervalued stocks that could complement or contrast with Republic Services in your portfolio.

- Strengthen your focus on resilience by reviewing companies in the 67 resilient stocks with low risk scores and see which ones line up with your comfort on volatility and downside.

- Target sturdier financial profiles by running through the solid balance sheet and fundamentals stocks screener (39 results) so you are not relying on just one type of business risk.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com