- If you are wondering whether Align Technology's current share price lines up with its underlying value, this article will walk you through what the numbers are saying.

- The stock last closed at US$166.38, with returns of 6.6% year to date, 4.5% over the past year, and declines of 3.9% over the last week, 12.5% over the last month, 50.2% over three years, and 69.5% over five years. This performance raises questions about how investors are reassessing its prospects and risks.

- Recent news coverage has focused on Align Technology in the context of orthodontic and dental markets, including ongoing interest in clear aligners and digital treatment planning. This backdrop helps explain why the share price has seen both enthusiasm and caution as investors react to changing expectations for demand and competition.

- Align Technology currently scores a valuation check of 3 out of 6. The next sections will compare different valuation approaches and then finish with a more complete way to think about what the stock might be worth.

Approach 1: Align Technology Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business could be worth by projecting its future cash flows and then discounting those amounts back to today using a required return. It is essentially asking what the stream of future cash flows is worth in present dollar terms.

For Align Technology, the model uses a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month Free Cash Flow is about $459 million. Analyst inputs and Simply Wall St extrapolations project annual Free Cash Flow reaching about $869 million in 2035, with intermediate years such as 2026 and 2029 at $830 million and $852 million. All of these figures are expressed in US$.

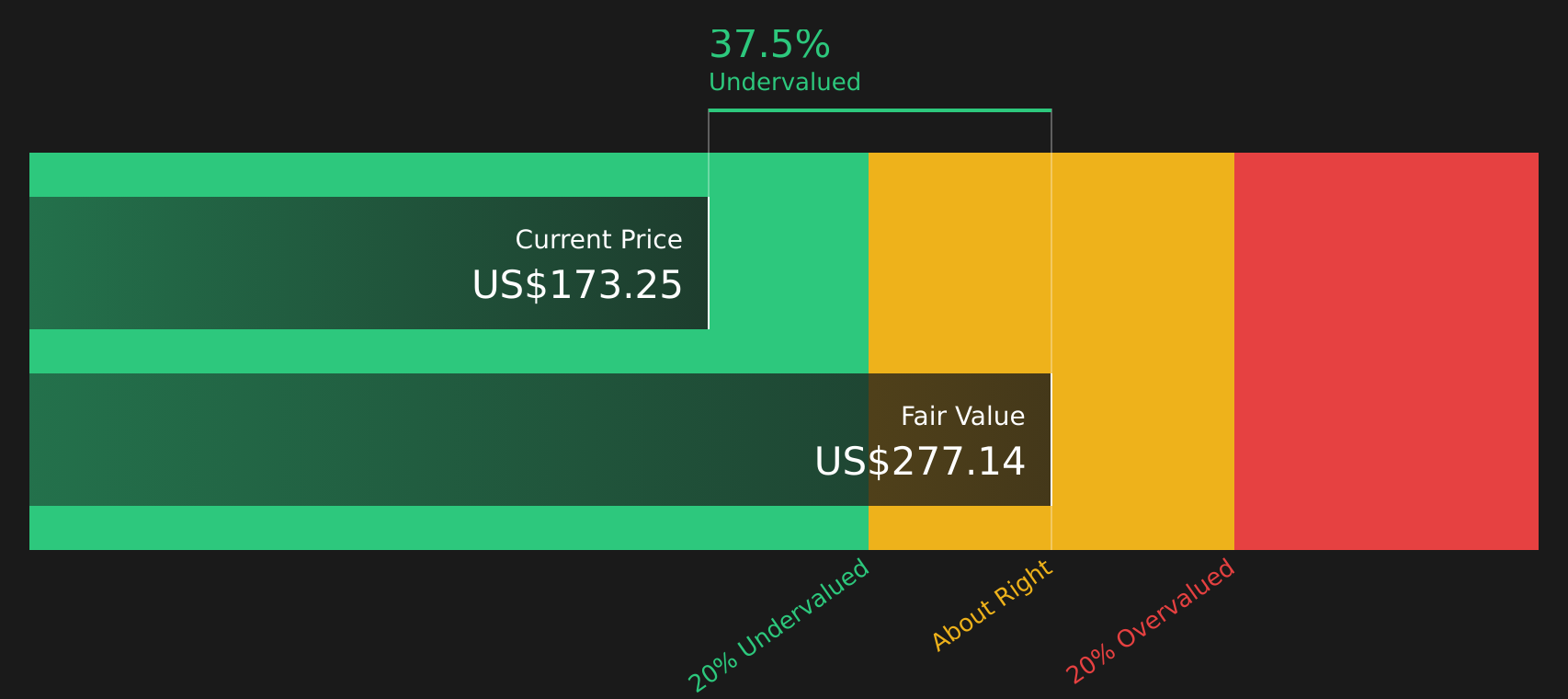

Pulling these projected cash flows together, the DCF model arrives at an estimated intrinsic value of about $215.87 per share. Compared with the recent share price of $166.38, this implies Align Technology trades at roughly a 22.9% discount, which suggests that the shares may be undervalued based on this cash flow view.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Align Technology is undervalued by 22.9%. Track this in your watchlist or portfolio, or discover 62 more high quality undervalued stocks.

Approach 2: Align Technology Price vs Earnings

For profitable companies, the P/E ratio is a useful yardstick because it links what you pay for each share to the earnings that business is currently generating. A higher or lower P/E can make sense depending on how the market views a company’s growth potential and risk profile, so there is no single “right” number that fits every stock.

Align Technology currently trades on a P/E of 28.90x. That sits slightly above the Medical Equipment industry average P/E of 27.18x and above the peer group average of 23.35x. On those simple comparisons, the shares look somewhat more expensive than many peers, which suggests the market may be assigning a premium to its earnings.

Simply Wall St’s Fair Ratio for Align Technology is 26.08x. This is a proprietary estimate of what P/E might be reasonable after considering factors such as earnings growth, profit margins, industry, market capitalization and key risks. Because it is tailored to the company’s specific profile rather than broad group averages, the Fair Ratio can be more informative than a basic industry or peer comparison. With the current P/E at 28.90x versus a Fair Ratio of 26.08x, the shares screen as slightly overvalued on this metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Align Technology Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives bring this to life by letting you link your view of Align Technology’s story to a simple forecast for revenue, earnings and margins, and then directly to a Fair Value that you can compare with the current share price.

On Simply Wall St’s Community page, Narratives turn different opinions into clear numbers. One investor who focuses on premium orthodontics holding up in a cost sensitive world might build a Narrative with a Fair Value closer to US$225, while another who worries more about competition and pricing pressure might lean toward a Fair Value nearer US$152.60 or even US$140. Both views stay current because the Fair Values refresh automatically as new news, earnings and analyst assumptions are added.

For Align Technology however we will make it really easy for you with previews of two leading Align Technology Narratives:

Fair value: US$201.69

Implied discount vs last close: about 17.5% undervalued

Revenue growth assumption: 4.96% per year

- Analysts frame Align as a recovery story, with demand for clear aligners and scanners supported by new clinical uses, broader dentist adoption and wider international access.

- They expect higher margins to come from digital workflows, automation, and more efficient production, while buybacks gradually reduce the share count.

- The narrative leans on a 2029 earnings outlook that supports a consensus fair value around US$201.69, provided revenue, margins and valuation multiples line up with analyst assumptions.

Fair value: US$154.62

Implied premium vs last close: about 7.6% overvalued

Revenue growth assumption: 4.80% per year

- This view sees Align operating in a cost sensitive world where inflation, tighter budgets and cheaper rivals make it harder to justify premium pricing.

- Competition from lower cost aligners and direct to consumer models, together with regional pricing differences, is treated as a real test of how resilient margins and branding are.

- The fair value of about US$154.62 reflects a belief that investors should focus less on past expansion and more on whether earnings quality and pricing power can hold up against rising pressure.

Do you think there's more to the story for Align Technology? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com