Genesis Energy (GEL) is facing a sexual assault lawsuit in Harris County State Court that names the company and a current board member, with Jane Doe seeking US$50 million in compensatory and punitive damages.

See our latest analysis for Genesis Energy.

The lawsuit lands at a time when Genesis Energy’s share price, now at US$17.78, has pulled back 2.79% over one day but still carries an 11.96% year to date share price return and an 18.10% one year total shareholder return. This builds on a 146.28% five year total shareholder return that reflects a long period of strong compounding despite recent volatility in sentiment around governance risks.

If this legal setback has you reassessing risk, it can help to broaden your watchlist with other infrastructure linked opportunities such as 26 power grid technology and infrastructure stocks

With Genesis Energy trading at US$17.78, at a discount to the average analyst price target and with an intrinsic value estimate that is even higher, you have to ask: is there mispricing here, or is the market already looking ahead?

Preferred Price to Sales Ratio of 1.3x: Is it justified?

On the numbers, Genesis Energy looks inexpensive on a P/S basis, yet the market is still pricing in governance questions and an unprofitable bottom line.

The key yardstick here is the price to sales ratio, which compares the company’s market value to its revenue. For a midstream partnership with lumpy earnings and a recent net loss of $89.664 million on $1.63b of revenue, sales based measures can give a cleaner read than earnings based ratios that are distorted by interest, depreciation and one off items.

Genesis Energy trades on a P/S of 1.3x, which is well below both the US Oil and Gas industry average of 2.1x and a peer average of 3.6x. This points to a heavy discount against other operators in the space. However, Simply Wall St’s fair P/S estimate sits lower at 0.9x, so the current multiple is above that fair ratio level and could compress if the market leans toward that benchmark.

Explore the SWS fair ratio for Genesis Energy

Result: Price-to-sales of 1.3x (UNDERVALUED)

However, the ongoing sexual assault lawsuit and the recent net loss of US$89.664 million on US$1.63b of revenue could easily unsettle the current pricing story.

Find out about the key risks to this Genesis Energy narrative.

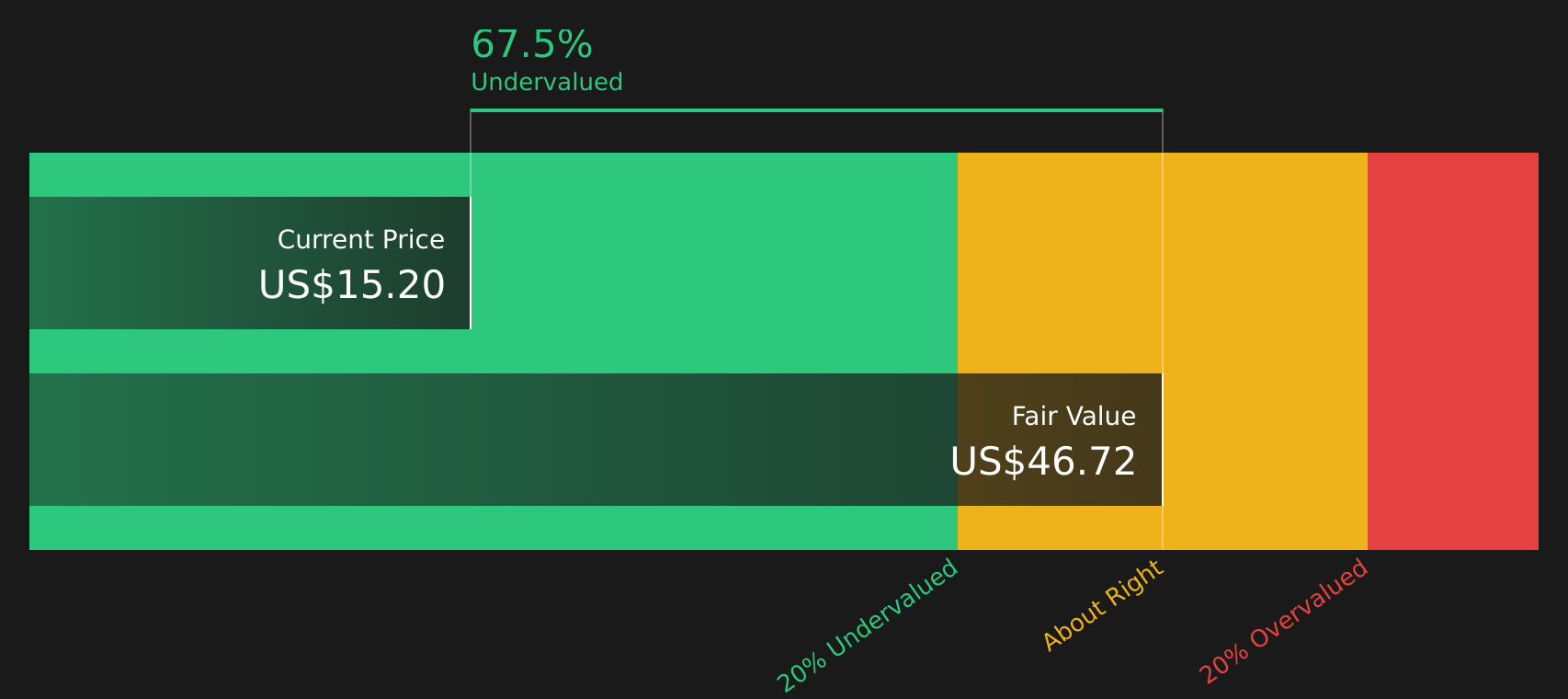

Another View: SWS DCF Points to Deep Undervaluation

The P/S ratio suggests Genesis Energy is inexpensive but not a screaming bargain, yet our DCF model paints a very different picture. With the shares at $17.78 and a future cash flow value estimate of $50.17, the SWS DCF model implies the units trade at a steep discount. Is the cash flow outlook too optimistic, or is sentiment too gloomy?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Genesis Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 62 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The mix of governance concerns, valuation signals and cash flow estimates can feel hard to reconcile, so move quickly to review the data yourself and weigh both sides. To see that balance set out clearly, take a look at the 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

Do not stop your research with Genesis Energy alone. Widen your net with targeted stock ideas that fit different goals and risk levels using the Simply Wall St Screener.

- Target potential value opportunities by scanning through 62 high quality undervalued stocks that combine strong fundamentals with more appealing pricing.

- Strengthen your income focus by reviewing 12 dividend fortresses built around higher yielding companies that may support more consistent cash returns.

- Dial down risk by checking 64 resilient stocks with low risk scores featuring companies with more resilient profiles and lower risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com