- Earlier this month, Ormat Technologies, Inc. completed two Rule 144A convertible note offerings totaling US$750,000,000, including zero-coupon and 1.5% senior unsecured notes due March 15, 2031.

- This mix of zero-coupon and low-coupon convertible debt materially expands Ormat’s financial flexibility while potentially introducing future equity dilution if the notes are converted.

- We’ll now explore how this sizeable 2031 convertible issuance could influence Ormat’s investment narrative around growth, funding, and dilution.

Uncover the next big thing with 32 elite penny stocks that balance risk and reward.

Ormat Technologies Investment Narrative Recap

To own Ormat Technologies, you need to believe in its ability to turn long term geothermal and storage projects into steady cash flows while managing heavy capital needs. The new US$750,000,000 zero and low coupon convertible notes strengthen near term funding capacity, but they also add the possibility of future equity dilution, which sits alongside execution risk in the electricity segment as a key issue to watch.

The recent start of commercial operations at the Shirk energy storage facility in California ties directly into this funding move, as it highlights Ormat’s push to grow its storage footprint underpinned by long duration contracts and investment tax credits. Together, these developments frame the 2031 convertible notes as an important tool for backing Ormat’s capital intensive growth ambitions while investors keep an eye on margin trends and policy support.

Yet investors should also be aware that if high capital spending continues while funding costs rise or project returns disappoint, then...

Read the full narrative on Ormat Technologies (it's free!)

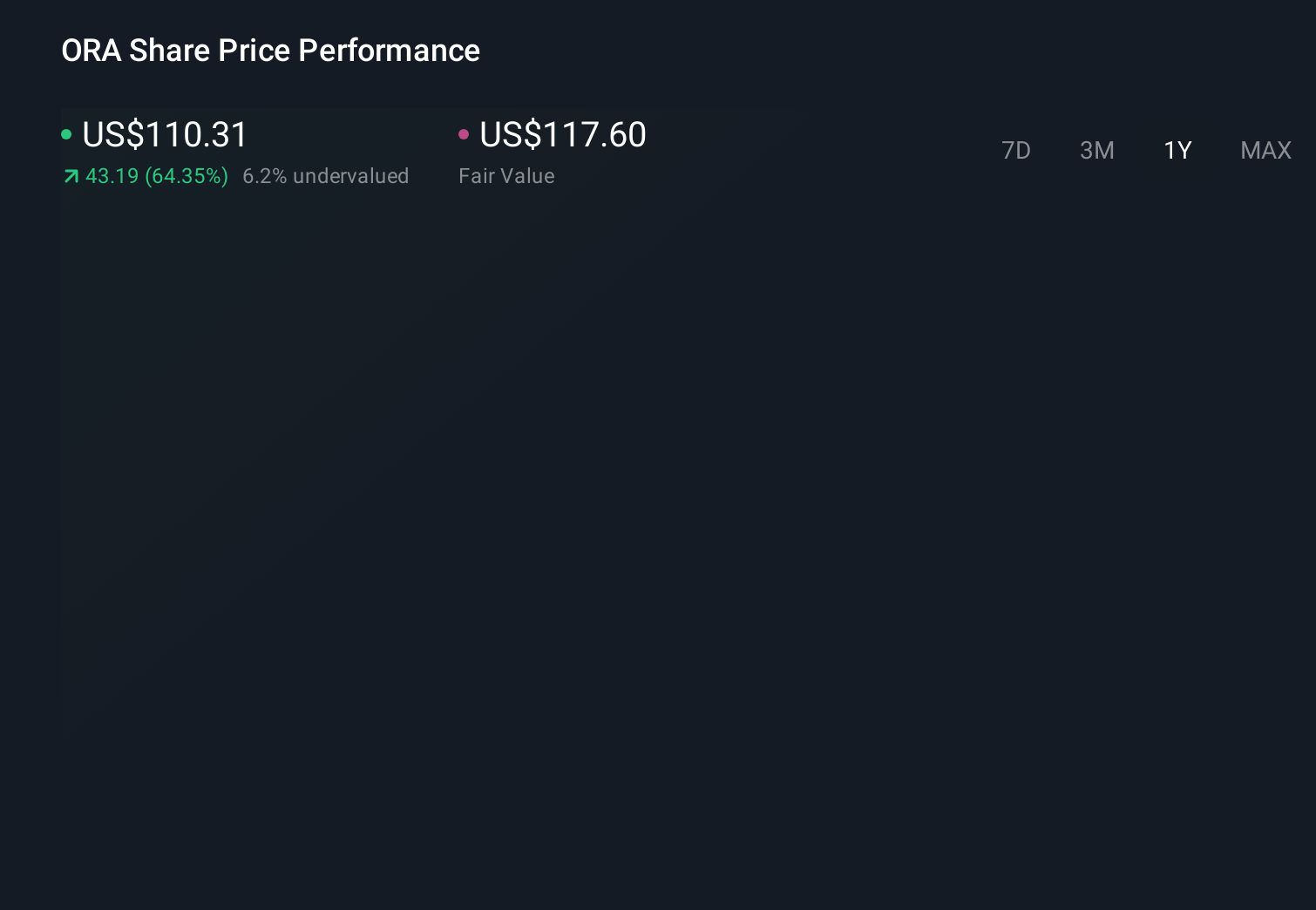

Ormat Technologies' narrative projects $1.3 billion revenue and $215.3 million earnings by 2029.

Uncover how Ormat Technologies' forecasts yield a $128.00 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Three fair value estimates from the Simply Wall St Community span a wide range, from about US$9 to US$128 per share, underlining how far opinions can diverge. Against this backdrop, Ormat’s heavier reliance on debt funded growth after the new 2031 convertibles invites you to weigh how funding risk could influence both future returns and the resilience of its business model.

Explore 3 other fair value estimates on Ormat Technologies - why the stock might be worth less than half the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Ormat Technologies research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Ormat Technologies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ormat Technologies' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Explore 22 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Outshine the giants: these 22 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com