- In late March 2026, Paychex reported third-quarter revenue of US$1,808.9 million and net income of US$560.3 million, alongside updates on completing two share repurchase authorizations totaling US$400 million and US$352.22 million, and highlighted its cybersecurity focus ahead of an RSA Conference presentation.

- While revenue and quarterly earnings per share increased year over year, nine-month net income and EPS were slightly lower, underscoring that growth in sales has not yet translated into higher cumulative profitability.

- We’ll now examine how this mix of strong quarterly growth, softer nine‑month profits, and substantial buybacks could influence Paychex’s investment narrative.

The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Paychex Investment Narrative Recap

To own Paychex, you need to believe that its broad HR and payroll platform, plus the Paycor acquisition and AI initiatives, can turn solid revenue growth into durable, cash‑backed earnings per share. The latest quarter supports that revenue story, but softer nine‑month profits keep execution risk in focus. In the near term, the key catalyst is whether Paycor integration and AI tools lift margins, while the biggest risk remains that rising costs and slower client activity keep earnings flat. For now, this earnings print does not materially change that balance.

The most relevant recent announcement is the completion of two buyback authorizations totaling about US$752 million, alongside a new US$1,000 million program. Against a year where earnings growth has been uneven and the share price has lagged, these repurchases can amplify per share metrics if profits improve, but they also matter because they commit a meaningful slice of the company’s US$1.8 billion cash and investment balance at a time when...

Read the full narrative on Paychex (it's free!)

Paychex's narrative projects $7.5 billion revenue and $2.3 billion earnings by 2029. This requires 5.6% yearly revenue growth and an earnings increase of about $0.7 billion from $1.6 billion today.

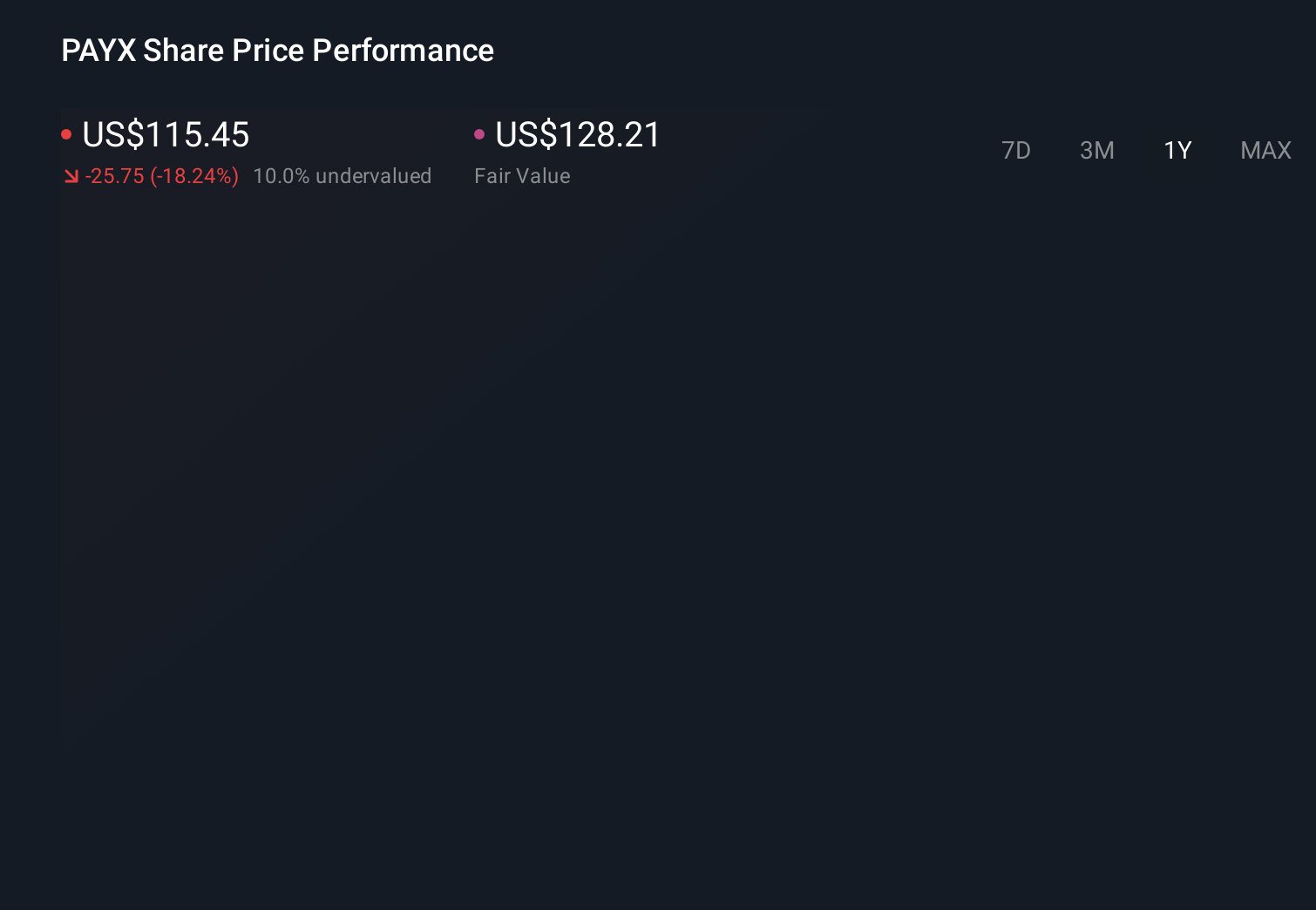

Uncover how Paychex's forecasts yield a $102.80 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts were already assuming only about 5.5 percent annual revenue growth and US$2.2 billion earnings by 2029, so compared with the more cautious view that Paychex’s 800,000‑client base could see flat employment levels and slower volume growth, their narrative is markedly more pessimistic; after this quarter’s revenue jump but softer nine‑month profit, it is worth asking whether those forecasts and the risk around volume driven revenue might now look closer to the mark, or need to be revisited entirely.

Explore 6 other fair value estimates on Paychex - why the stock might be worth as much as 75% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Paychex research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Paychex research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Paychex's overall financial health at a glance.

Seeking Other Investments?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 21 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Uncover the next big thing with 32 elite penny stocks that balance risk and reward.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 25 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com