- If you are wondering whether Mohawk Industries at around US$95 a share looks cheap or expensive right now, this article walks you through what the current price could mean for you as an investor.

- The stock has been under pressure recently, with returns of a 6.4% decline over 7 days, 23.9% decline over 30 days, 12.9% decline year to date, and 16.5% decline over the last year, while the 3 year and 5 year returns stand at a 3.9% decline and 52.6% decline.

- Recent coverage around Mohawk has focused on how the company is positioned in the Consumer Durables space and how sentiment toward housing and renovation activity is affecting the flooring and surfaces segment. This context helps explain why some investors are reassessing both the risks and potential rewards at the current share price.

- Simply Wall St currently assigns Mohawk Industries a valuation score of 5 out of 6, and the rest of this article will compare what different valuation approaches say about that price tag, before finishing with a fuller way to think about value that goes beyond a single number.

Find out why Mohawk Industries's -16.5% return over the last year is lagging behind its peers.

Approach 1: Mohawk Industries Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company could be worth by projecting its future cash flows and discounting them back to today’s value.

For Mohawk Industries, the latest twelve month Free Cash Flow is about $559.9 million. Analysts and Simply Wall St projections suggest Free Cash Flow in the $600 million to $700 million range over the next decade, including $601.5 million in 2026 and $712.1 million in 2035, with interim years such as 2027 at $682.5 million and 2028 at $655 million. These projections use a 2 Stage Free Cash Flow to Equity model, where near term estimates come from analysts and the later years are extrapolated.

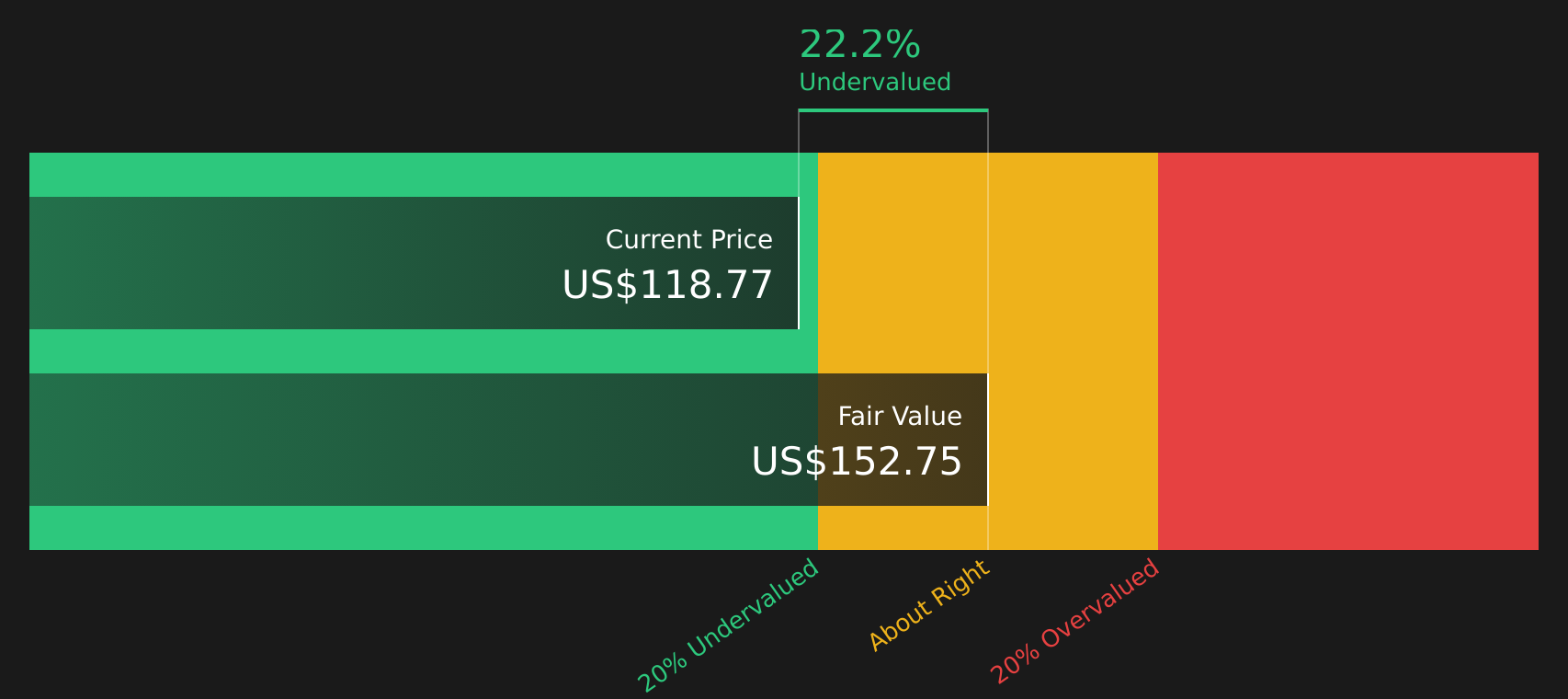

Discounting those projected cash flows back to today gives an estimated intrinsic value of about $150.36 per share. Compared with the current share price of roughly $95, this DCF output implies the stock is about 36.6% undervalued on these assumptions.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Mohawk Industries is undervalued by 36.6%. Track this in your watchlist or portfolio, or discover 62 more high quality undervalued stocks.

Approach 2: Mohawk Industries Price vs Earnings

For profitable companies, the P/E ratio is a useful shortcut because it links what you pay for the stock to the earnings the business is already generating. It helps you see how many dollars of price you are paying for each dollar of current earnings.

What counts as a “normal” P/E ratio usually reflects how the market views a company’s growth prospects and risk. Higher growth and perceived stability often justify a higher P/E, while lower growth or higher risk tend to align with a lower multiple.

Mohawk Industries currently trades on a P/E of about 15.8x. That sits above the Consumer Durables industry average of roughly 11.5x and below the peer group average of around 18.0x. Simply Wall St also provides a proprietary “Fair Ratio” of 25.5x, which represents the P/E that might be expected given factors such as earnings growth, industry, profit margins, market cap and company specific risks.

This Fair Ratio is more tailored than a simple comparison with peers or industry averages because it adjusts for Mohawk’s own characteristics rather than assuming all companies should trade on the same multiple. Comparing the current 15.8x P/E to the Fair Ratio of 25.5x points to the shares trading below that model implied level.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Mohawk Industries Narrative

Earlier the article mentioned that there is an even better way to understand valuation. Narratives are introduced here as short, clear stories that you set around Mohawk Industries, linking your view of its future revenue, earnings and margins to a financial forecast and a fair value. You can then compare that fair value with the current price to help you decide if the stock looks attractive or not. All of this is done within an easy tool on Simply Wall St’s Community page that updates when new information like earnings or news arrives. One investor might build a more optimistic Mohawk Narrative closer to the US$160 analyst target, while another might lean toward a more cautious view nearer US$121, and both can see how their story translates into numbers in real time.

Do you think there's more to the story for Mohawk Industries? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com