Over the last 7 days, the United States market has dropped 3.5%, yet it has seen a robust rise of 14% over the past year, with earnings forecasted to grow by 15% annually. In this dynamic environment, identifying stocks with strong fundamentals and growth potential can be key to uncovering undiscovered gems worth exploring in March 2026.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Morris State Bancshares | 1.94% | 4.43% | 2.90% | ★★★★★★ |

| Cashmere Valley Bank | 31.17% | 5.25% | 1.74% | ★★★★★★ |

| Oakworth Capital | 26.12% | 15.98% | 13.01% | ★★★★★★ |

| ASA Gold and Precious Metals | NA | 12.65% | 41.20% | ★★★★★★ |

| Sound Financial Bancorp | 16.27% | 0.75% | -13.28% | ★★★★★★ |

| Affinity Bancshares | 42.51% | 1.82% | 1.11% | ★★★★★★ |

| First Northern Community Bancorp | NA | 7.53% | 11.34% | ★★★★★★ |

| Seneca Foods | 38.64% | 2.39% | -18.65% | ★★★★★☆ |

| NameSilo Technologies | 12.63% | 14.48% | 3.12% | ★★★★★☆ |

| Pure Cycle | 5.42% | 9.36% | -2.03% | ★★★★★☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

John B. Sanfilippo & Son (JBSS)

Simply Wall St Value Rating: ★★★★★☆

Overview: John B. Sanfilippo & Son, Inc., through its subsidiary JBSS Ventures, LLC, is involved in processing and distributing tree nuts and peanuts in the United States with a market capitalization of approximately $906.78 million.

Operations: JBSS generates revenue primarily from selling various nut and nut-related products and bars, totaling $1.14 billion.

John B. Sanfilippo & Son, a player in the food sector, has demonstrated robust financial health with earnings growth of 44.2% over the past year, outpacing the industry average of -1.1%. The company trades at a value 15.7% below its estimated fair value and boasts high-quality earnings. Debt management appears sound with a net debt to equity ratio at 11.4%, deemed satisfactory, while interest payments are well covered by EBIT at 26 times coverage. Recent events include announcing a special dividend of $1.50 per share, returning approximately $17.6 million to shareholders in May 2026.

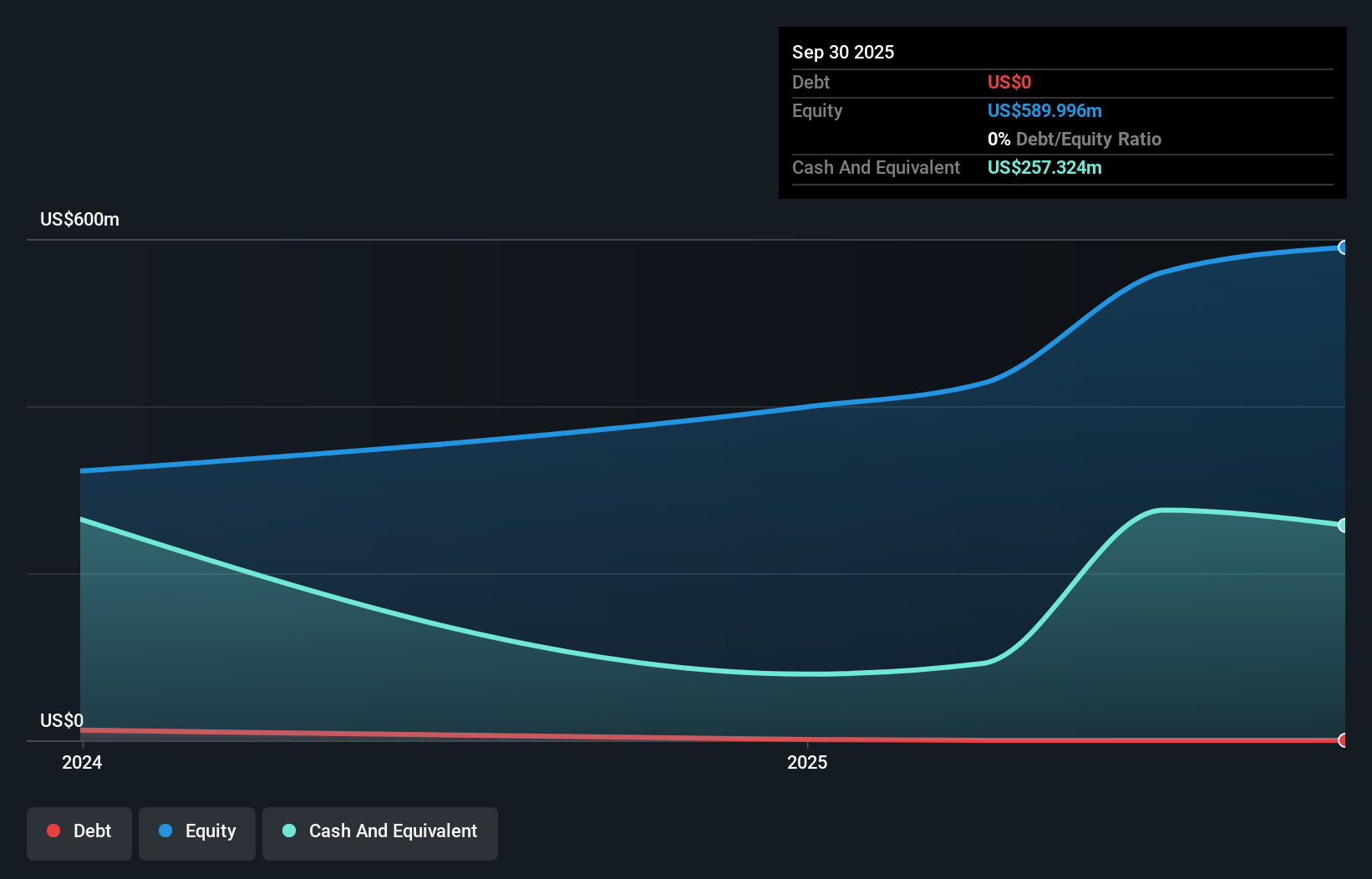

Ategrity Specialty Insurance Company Holdings (ASIC)

Simply Wall St Value Rating: ★★★★★★

Overview: Ategrity Specialty Insurance Company Holdings offers excess and surplus lines insurance and reinsurance products to small and medium-sized businesses in the United States, with a market cap of approximately $914.23 million.

Operations: ASIC generates revenue primarily from its insurance business, totaling $424.34 million.

Ategrity Specialty Insurance Company Holdings, a notable contender in the insurance sector, showcases robust financial health with high-quality earnings and no debt concerns. Its earnings surged 56.5% last year, outpacing the industry average of 25.8%. Trading at 52.7% below estimated fair value, Ategrity appears undervalued. Recent performance highlights include a full-year revenue increase to US$424 million from US$343 million and net income rising to US$74 million from US$47 million previously. The company announced a share repurchase program worth up to US$50 million, signaling confidence in its growth trajectory and shareholder value enhancement strategy.

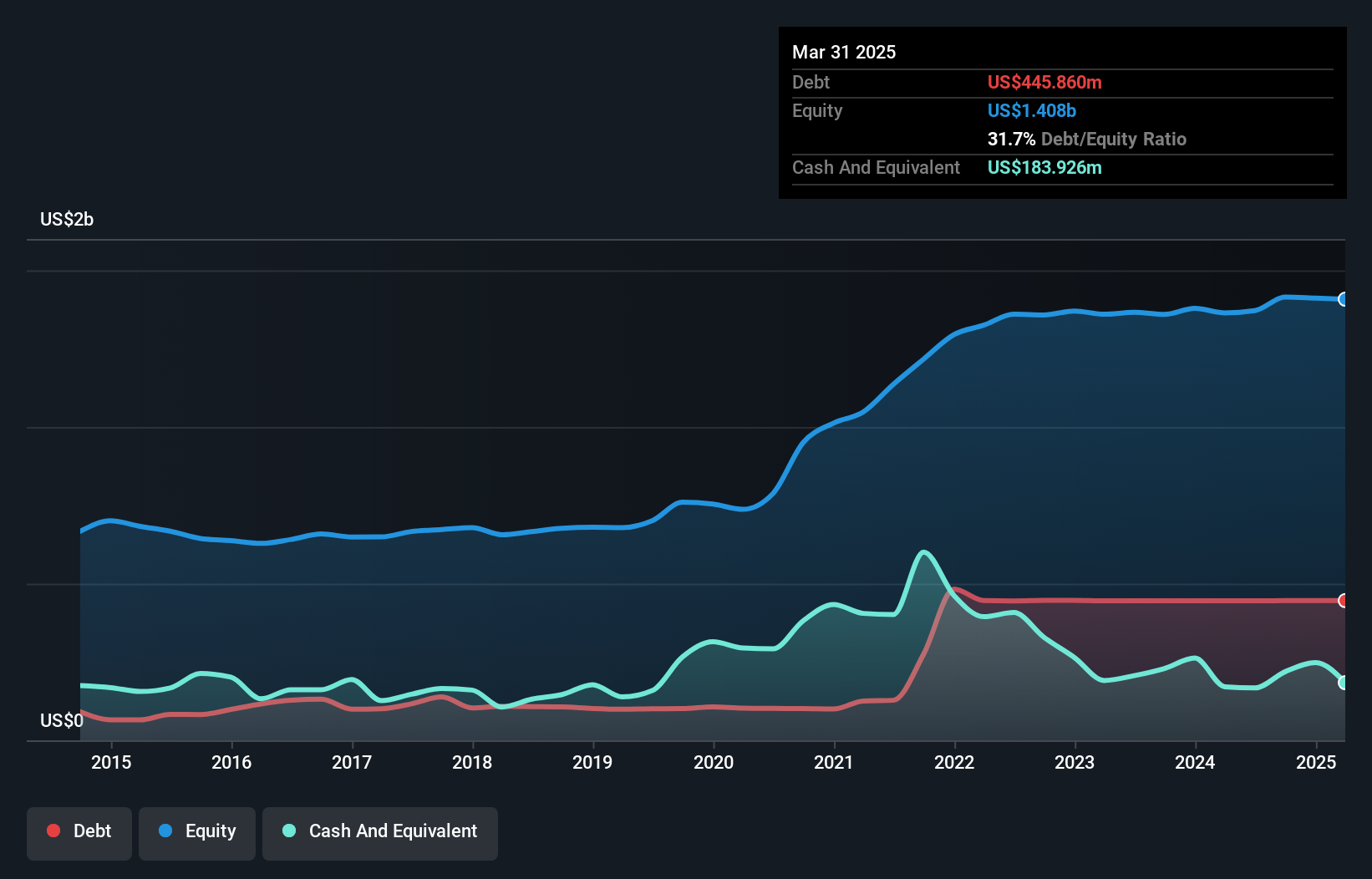

Stewart Information Services (STC)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Stewart Information Services Corporation operates through its subsidiaries to offer title insurance and real estate transaction services both in the United States and internationally, with a market cap of approximately $1.80 billion.

Operations: Stewart Information Services generates revenue primarily from its Title segment, which includes mortgage services, amounting to $2.48 billion, and Real Estate Solutions at $438.37 million.

Stewart Information Services appears to be making strides with its strategic focus on acquisitions and digital enhancements, aiming for a stronger foothold in the title and real estate services market. The company reported a significant revenue increase to US$2.92 billion last year, up from US$2.49 billion, alongside net income growth to US$115.54 million from US$73.31 million previously. With a price-to-earnings ratio of 16.1x, below the broader market's 18.2x, Stewart seems undervalued relative to peers while also boasting high-quality earnings and robust EBIT covering interest payments 9 times over. However, potential challenges like rising operational costs could impact profitability despite these positive metrics.

Next Steps

- Gain an insight into the universe of 333 US Undiscovered Gems With Strong Fundamentals by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com