Over the last 7 days, the United States market has dropped 3.5%, but it has seen a rise of 14% over the past year, with earnings projected to grow by 15% annually in coming years. In light of these conditions, identifying stocks with strong financial health and growth potential is crucial for investors seeking opportunities beyond mainstream options. Penny stocks, though an outdated term, still represent a niche investment area that can offer surprising value and potential returns when backed by robust balance sheets.

Top 10 Penny Stocks In The United States

| Name | Share Price | Market Cap | Rewards & Risks |

| ATRenew (RERE) | $4.69 | $1.07B | ✅ 4 ⚠️ 0 View Analysis > |

| LexinFintech Holdings (LX) | $2.075 | $349.15M | ✅ 3 ⚠️ 2 View Analysis > |

| Tuya (TUYA) | $2.28 | $1.41B | ✅ 5 ⚠️ 1 View Analysis > |

| FinVolution Group (FINV) | $4.71 | $1.18B | ✅ 4 ⚠️ 1 View Analysis > |

| Tuniu (TOUR) | $0.78 | $89.32M | ✅ 2 ⚠️ 2 View Analysis > |

| Information Services Group (III) | $3.11 | $179.26M | ✅ 3 ⚠️ 1 View Analysis > |

| Golden Growers Cooperative (GGRO.U) | $5.00 | $77.45M | ✅ 2 ⚠️ 5 View Analysis > |

| Niagen Bioscience (NAGE) | $4.28 | $337.04M | ✅ 3 ⚠️ 1 View Analysis > |

| LifeVantage (LFVN) | $4.40 | $55.06M | ✅ 4 ⚠️ 3 View Analysis > |

| Village Farms International (VFF) | $2.65 | $308.48M | ✅ 5 ⚠️ 1 View Analysis > |

Click here to see the full list of 366 stocks from our US Penny Stocks screener.

Underneath we present a selection of stocks filtered out by our screen.

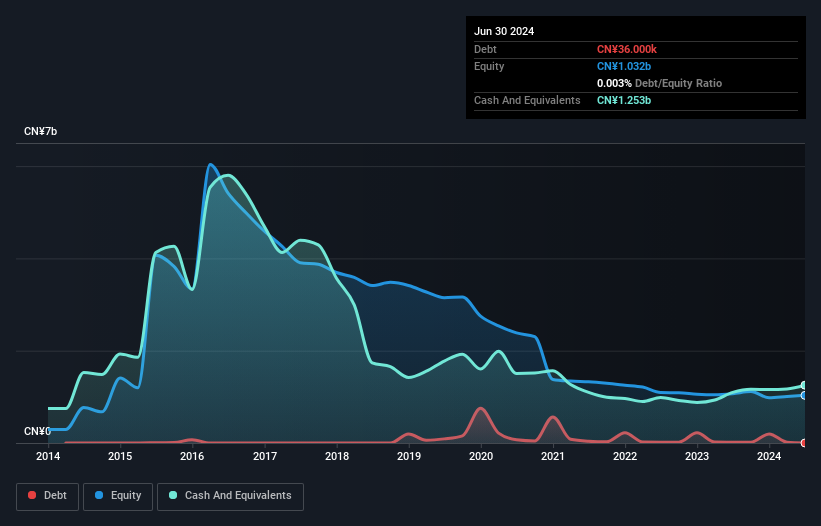

Tuniu (TOUR)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Tuniu Corporation, along with its subsidiaries, operates as an online leisure travel company in the People’s Republic of China and Hong Kong, with a market cap of $89.32 million.

Operations: The company generates revenue primarily from its travel services segment, which accounted for CN¥577.97 million.

Market Cap: $89.32M

Tuniu Corporation, with a market cap of $89.32 million, has experienced stable weekly volatility and its short-term assets exceed liabilities, indicating strong liquidity. The company's debt is well-covered by operating cash flow and it has reduced its debt to equity ratio to 0% over the past five years. Despite having high-quality earnings and no significant shareholder dilution recently, Tuniu's net profit margin declined from last year and it reported negative earnings growth over the past year. Revenue guidance for Q1 2026 suggests modest growth, reflecting cautious optimism in an evolving market landscape.

- Take a closer look at Tuniu's potential here in our financial health report.

- Learn about Tuniu's future growth trajectory here.

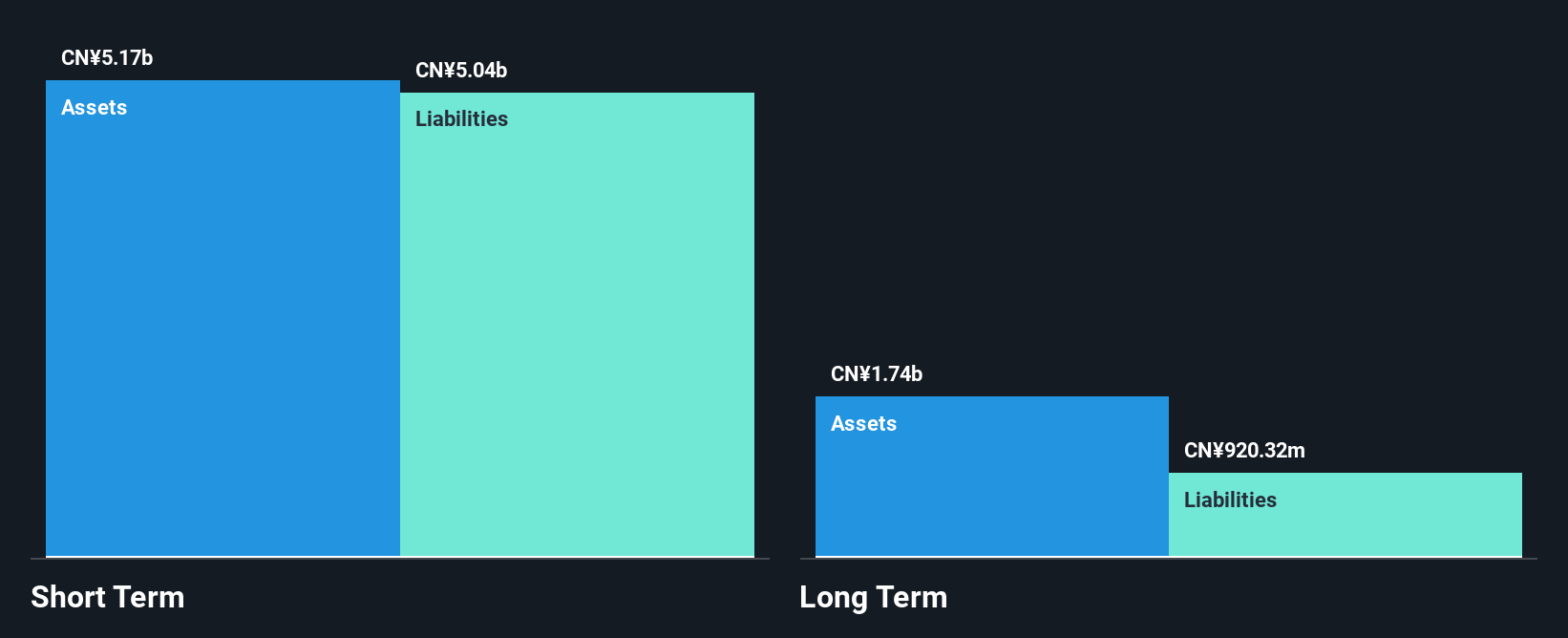

Citizens (CIA)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Citizens, Inc. is a diversified financial services company offering life, living benefits, and final expense insurance along with other financial products to individuals and small businesses across the U.S., Latin America, and Asia, with a market cap of $230.37 million.

Operations: The company's revenue is primarily derived from its International Insurance segment at $175.66 million, followed by Domestic Insurance at $79.05 million, and a smaller contribution from Other Non-Insurance Enterprises amounting to $0.91 million.

Market Cap: $230.37M

Citizens, Inc., with a market cap of US$230.37 million, reported an increase in quarterly revenue to US$72.07 million and net income of US$7.34 million, reflecting improved profitability compared to the previous year. Despite having no debt and maintaining high-quality earnings without shareholder dilution, the company's short-term assets fall short of covering its liabilities, posing liquidity challenges. While Citizens' profit margins have slightly decreased from last year and earnings growth was negative over the past year, forecasts suggest a potential annual growth rate of 11.08%. The management team is seasoned with an average tenure of six years.

- Click here and access our complete financial health analysis report to understand the dynamics of Citizens.

- Examine Citizens' earnings growth report to understand how analysts expect it to perform.

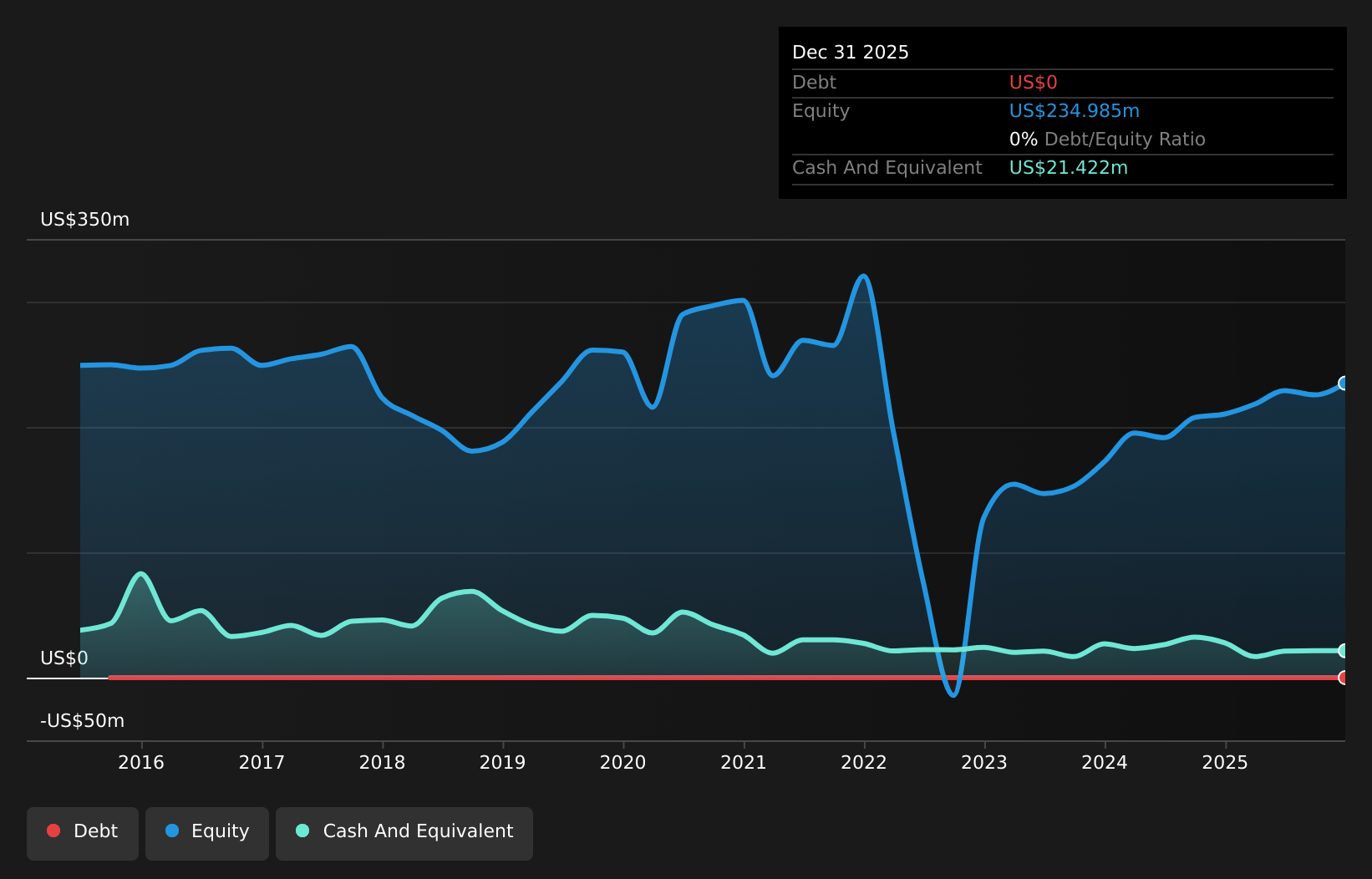

Dingdong (Cayman) (DDL)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Dingdong (Cayman) Limited is an e-commerce company based in China, with a market cap of approximately $537.91 million.

Operations: The company's revenue primarily comes from its online retail segment, generating CN¥24.02 billion.

Market Cap: $537.91M

Dingdong (Cayman) Limited, with a market cap of approximately US$537.91 million, has shown robust growth in its earnings, which increased by 43.3% over the past year and outpaced industry averages. The company trades at a favorable price-to-earnings ratio of 13.2x compared to the broader US market and maintains high-quality earnings with no significant shareholder dilution recently. Despite recent executive changes, including a new CEO appointment, Dingdong remains financially stable with more cash than debt and short-term assets exceeding liabilities. However, net income decreased to CN¥31 million in Q4 2025 from CN¥89.18 million the previous year.

- Jump into the full analysis health report here for a deeper understanding of Dingdong (Cayman).

- Review our growth performance report to gain insights into Dingdong (Cayman)'s future.

Summing It All Up

- Embark on your investment journey to our 366 US Penny Stocks selection here.

- Ready To Venture Into Other Investment Styles? The latest GPUs need a type of rare earth metal called Dysprosium and there are only 25 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com