Sanmina (SANM) shares closed at $129.64 on the NasdaqGS, with the stock showing mixed near term performance, including a 4.5% gain over the past day and weaker returns over the past month and past three months.

See our latest analysis for Sanmina.

That 4.5% 1 day share price gain comes after weaker short term share price returns, while the 1 year total shareholder return of 70.5% suggests longer term momentum has been much stronger than recent trading implies.

If Sanmina’s recent moves have you reassessing your watchlist, this could be a useful time to size up opportunities in power and electronics supply chains using our 26 power grid technology and infrastructure stocks

With Sanmina trading at $129.64 against a published analyst price target of $180.00, and with annual revenue and net income growth both above 20%, is there still an opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 34.4% Undervalued

Sanmina's most followed narrative assigns a fair value of $197.50 per share, well above the recent $129.64 close, framing the latest pullback as a possible valuation gap.

The imminent acquisition of ZT Systems is expected to add $5–6 billion of annual run-rate revenue, positioning Sanmina to double its net revenue within three years and capitalize on explosive growth in data center and AI infrastructure investment, this should provide a multi-year boost to overall revenue and EPS accretion from synergies and integration.

Curious what kind of revenue curve and profit margin path would support that valuation jump, and how rich a future earnings multiple the narrative leans on.

Result: Fair Value of $197.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upside case still depends heavily on smooth integration of ZT Systems and consistent orders from a handful of large customers that collectively generate more than half of revenue.

Find out about the key risks to this Sanmina narrative.

Another Take On Value

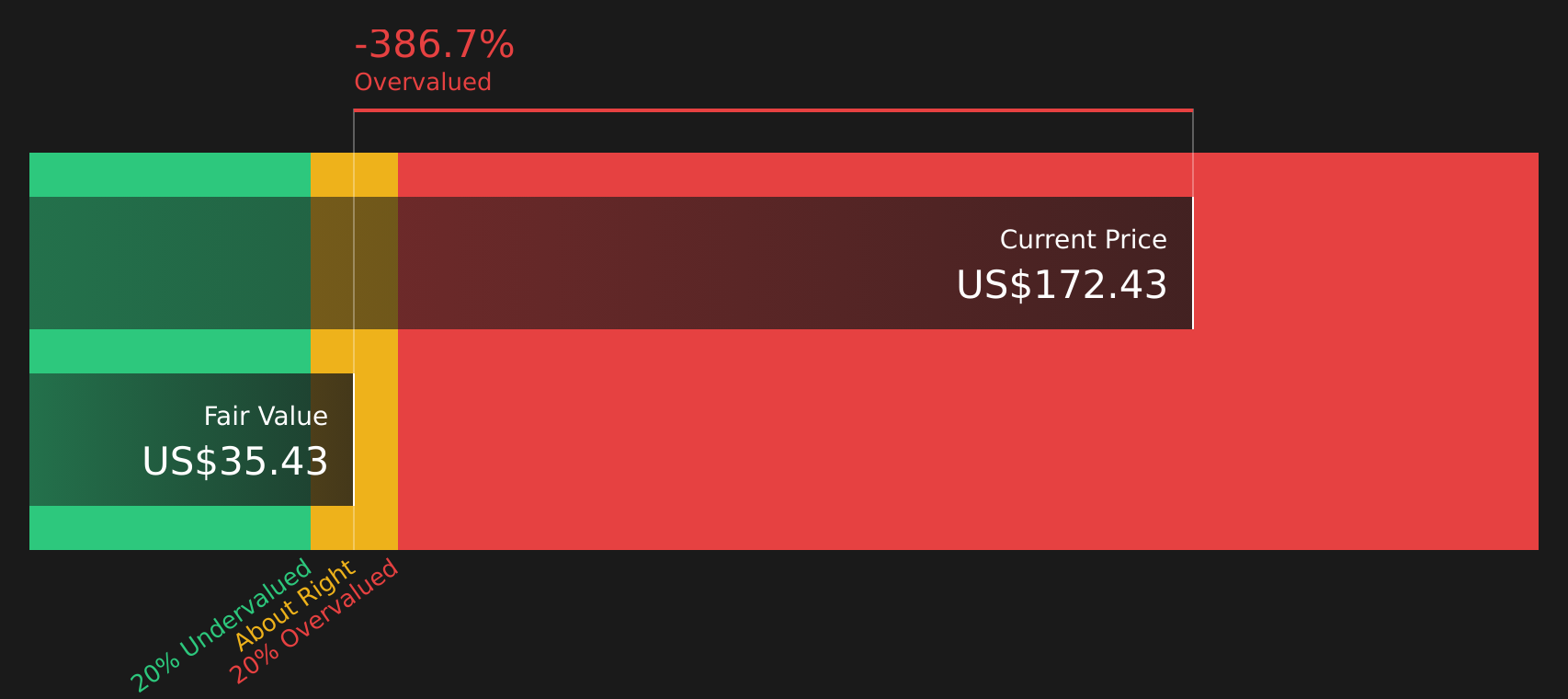

While the leading narrative sees Sanmina as 34.4% undervalued, the SWS DCF model points the other way, with a future cash flow value of $76 per share versus the current $129.64, flagging the stock as overvalued on this view. Which story do you trust more?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

The split views on Sanmina's value make this a moment to move quickly, check the underlying numbers yourself, and decide where you stand using the 2 key rewards and 2 important warning signs

Looking for more investment ideas?

If Sanmina is already on your radar, do not stop there. Broaden your watchlist now so you do not miss other opportunities taking shape.

- Target dependable cash generators by scanning companies with solid finances using the solid balance sheet and fundamentals stocks screener (39 results).

- Spot potential value opportunities early by reviewing the 58 high quality undervalued stocks before prices fully reflect their fundamentals.

- Hunt for lesser known potential opportunities that could be flying under the radar with the screener containing 25 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com