Powell Industries (POWL) has drawn fresh attention after announcing a three-for-one forward stock split, paired with an increase in authorized shares. The move is designed to support liquidity and future corporate flexibility.

See our latest analysis for Powell Industries.

The stock split headlines come on top of a sharp move in the share price, with a 90 day share price return of 73.8% and a year to date share price return of 57.17%, while the 1 year total shareholder return is 206.77%. This points to strong momentum building over both shorter and longer periods.

If this kind of price action has your attention, it may be worth widening your search using our power grid technology and infrastructure stocks screener as a next stop, starting with the 26 power grid technology and infrastructure stocks.

With the stock up sharply and trading above the average analyst price target, the key question now is whether Powell Industries is still mispriced or if the recent run already reflects the growth that analysts are expecting.

Most Popular Narrative: 105.8% Overvalued

Powell Industries last closed at $554.05, while the most followed narrative points to a fair value of $269.26, creating a wide valuation gap that hinges on specific growth and margin assumptions.

The market may be pricing in sustained outsized revenue growth and backlog conversion driven by robust order activity in electric utility, data center, and offshore energy infrastructure sectors benefiting from the accelerating buildout of electrification and grid modernization resulting in potentially over optimistic top line expectations.

Curious what kind of revenue trajectory and margin path could still leave the shares looking expensive at current levels. The narrative leans on measured growth, moderating profitability, and a future earnings multiple that has to work hard to justify today’s price.

Result: Fair Value of $269.26 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still a couple of big what ifs, including stronger than expected demand across utilities and data centers, as well as more lasting margin gains from recent projects.

Find out about the key risks to this Powell Industries narrative.

Another Angle On Valuation

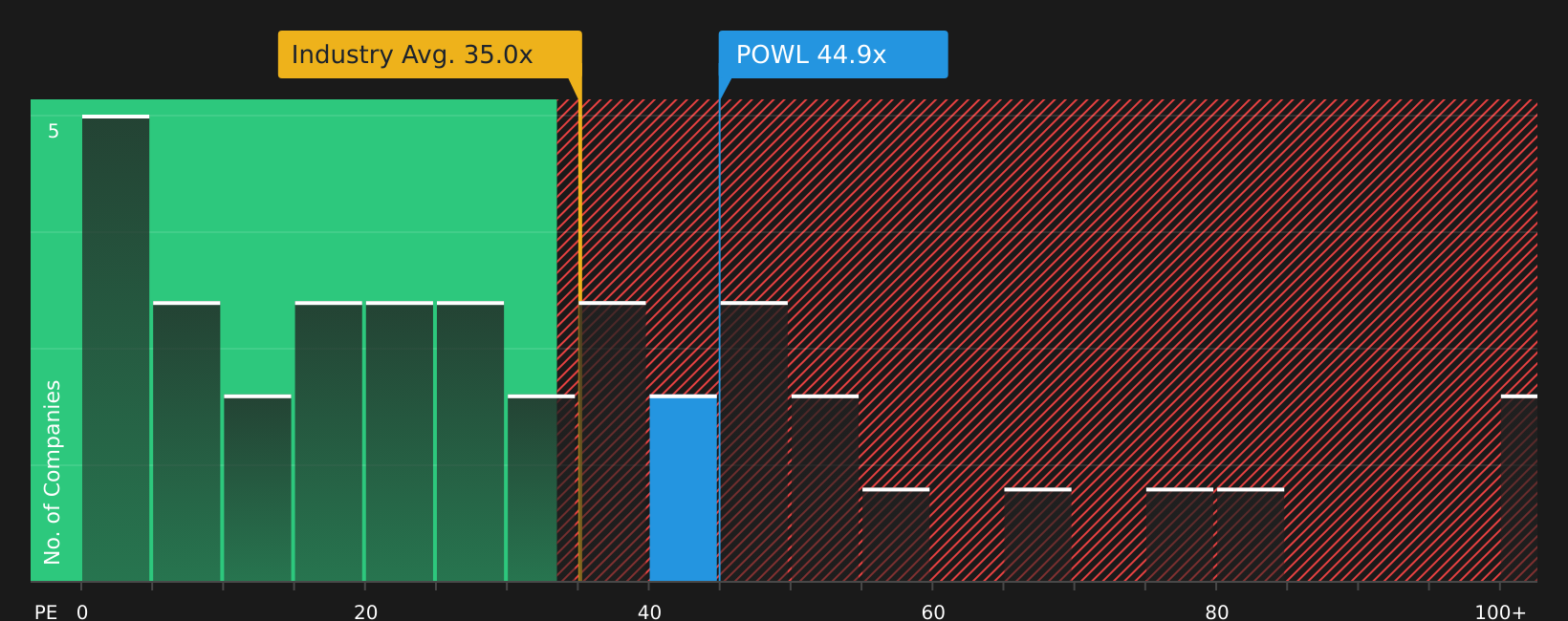

The narrative fair value of $269.26 points to Powell Industries looking expensive, but the P/E picture is more mixed. The shares trade on 35.9x earnings, above the US Electrical industry at 32.4x, yet below peers at 66.4x and above a fair ratio of 29.6x, which suggests meaningful valuation risk if sentiment cools.

For a closer look at how that kind of premium could compress or hold up in different scenarios, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment pulled in two directions by strong price momentum and valuation questions, it makes sense to check the data yourself and move quickly while you form your own view, starting with the 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Powell Industries has sharpened your focus on pricing and quality, it is worth lining up a few more names so you are not relying on a single story.

- Target value focused opportunities by scanning companies that screen as attractively priced on fundamentals with the 63 high quality undervalued stocks.

- Strengthen your income watchlist by finding companies that pair higher yields with balance sheet support using the 12 dividend fortresses.

- Prioritize resilience by filtering for businesses with lower risk scores and steadier profiles through the 65 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com