- Polaris Off Road and its RZR Factory Racing team recently dominated the historic San Felipe 250 in Mexico, securing a Pro UTV Open Class win and sweeping the overall podium while extending a three-year winning streak at the event.

- This racing success not only reinforces the performance credentials of Polaris’ RZR Pro R Factory platform, it also enhances brand visibility that could help counter concerns about stagnating sales and rising investment needs.

- We’ll now examine how this podium sweep and enhanced brand visibility may influence Polaris’ existing investment narrative and future expectations.

Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Polaris Investment Narrative Recap

To own Polaris, you need to believe that its core powersports brands can convert product enthusiasm and racing credibility into sustainable profits, despite recent losses and tariff headwinds. The San Felipe 250 podium sweep strengthens the RZR performance story and brand visibility, but it does little to change the near term earnings catalyst around the upcoming Q1 2026 results or the key risk of pressured margins from tariffs and softer demand.

Among recent announcements, the upcoming Q1 2026 earnings release on April 28 stands out as most relevant. Investors will be watching how racing wins and a steady stream of product launches, such as premium RZR and RANGER models, show up in actual sales, margins, and free cash flow after a year in which Polaris generated US$7,236.3 million of revenue but recorded a net loss of US$465.5 million.

Yet beneath the race wins, investors also need to be aware of rising tariff exposure and how it could...

Read the full narrative on Polaris (it's free!)

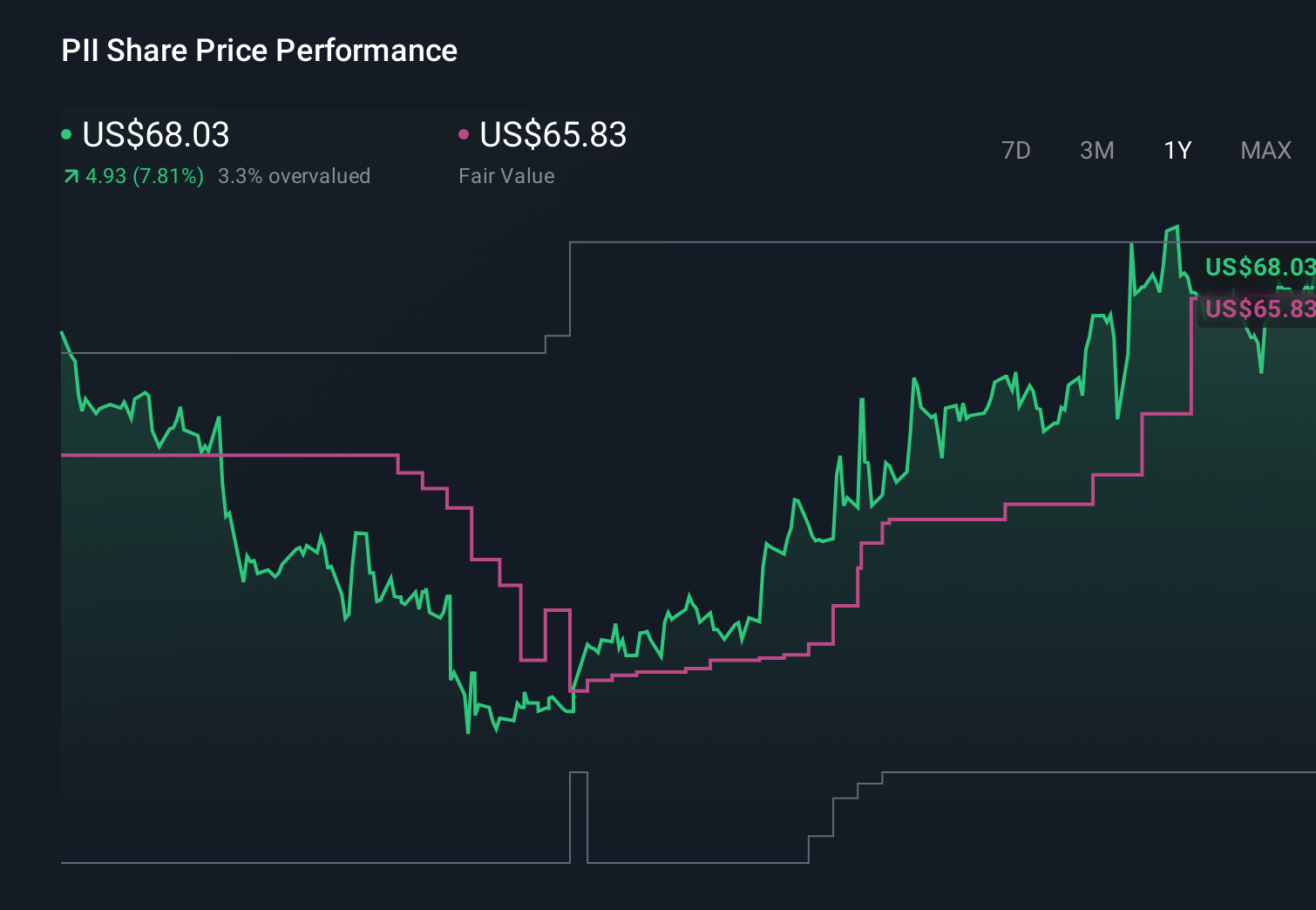

Polaris’ narrative projects $7.8 billion revenue and $243.0 million earnings by 2029.

Uncover how Polaris' forecasts yield a $66.71 fair value, a 22% upside to its current price.

Exploring Other Perspectives

While the consensus view leans on tariff mitigation and product strength, the most pessimistic analysts expect revenue near US$7.1 billion and only US$219.8 million of earnings by 2028, reminding you that opinions on Polaris, even after a big racing win, can differ sharply and may shift as new information comes in.

Explore 4 other fair value estimates on Polaris - why the stock might be worth as much as 48% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Polaris research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Polaris research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Polaris' overall financial health at a glance.

Contemplating Other Strategies?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 22 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Invest in the nuclear renaissance through our list of 94 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com