- Bank OZK recently announced that its Board of Directors raised the quarterly cash dividend on common stock to US$0.47 per share and declared a quarterly dividend of US$0.28906 per share on its 4.625% Series A Non-Cumulative Perpetual Preferred Stock, both payable in mid-April and mid-May 2026 to shareholders of record.

- This latest dividend increase extends Bank OZK’s long record of dividend growth and may be read as a signal of management’s confidence in the bank’s underlying financial strength ahead of its upcoming first-quarter 2026 results.

- We’ll now examine how this incremental common dividend increase shapes Bank OZK’s existing investment narrative built around yield-curve benefits and lending expansion.

Invest in the nuclear renaissance through our list of 94 elite nuclear energy infrastructure plays powering the global AI revolution.

Bank OZK Investment Narrative Recap

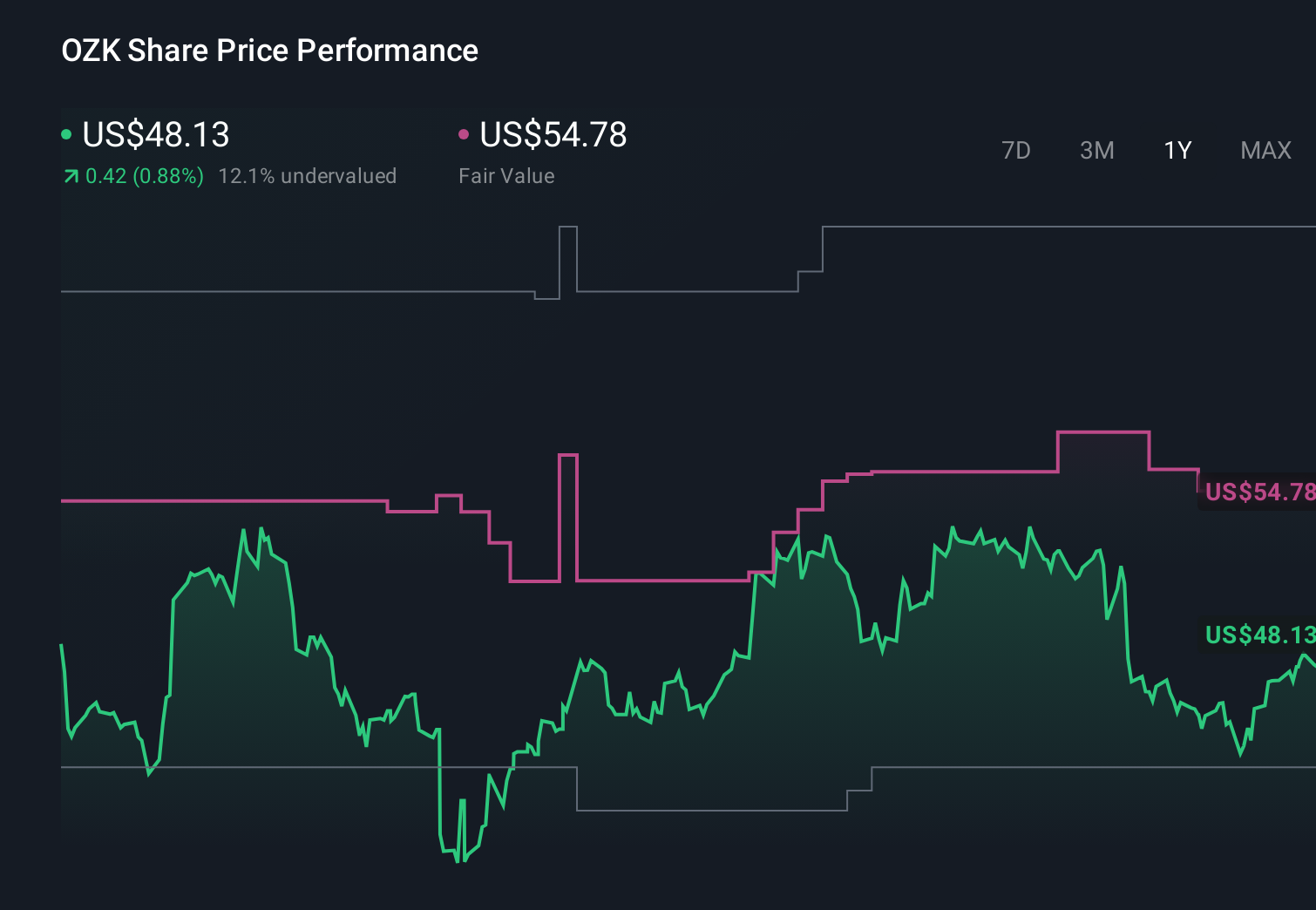

To own Bank OZK, you need to be comfortable with a bank that leans into commercial real estate and Sun Belt growth, while relying on disciplined underwriting and consistent dividends to compensate for that concentration risk. The latest US$0.01 quarterly dividend increase and ongoing preferred dividends do not materially change the near term picture; the key catalyst remains upcoming Q1 2026 results, while the biggest risk is still a potential downturn in commercial real estate and related credit quality pressures.

The most relevant recent announcement is Bank OZK’s plan to report first quarter 2026 earnings on April 21, 2026, alongside management commentary. This dividend hike lands just ahead of that update, so investors will soon see how net interest income, loan growth and credit costs are tracking relative to both the bank’s CRE heavy profile and its expansion efforts in Corporate & Institutional Banking and newer growth markets.

Yet even with a higher dividend today, investors should be aware of how a concentrated commercial real estate book could react if...

Read the full narrative on Bank OZK (it's free!)

Bank OZK's narrative projects $2.1 billion revenue and $815.7 million earnings by 2028.

Uncover how Bank OZK's forecasts yield a $53.00 fair value, a 15% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts take a more cautious view than the consensus, even with this dividend news, expecting revenue of about US$2.0 billion and earnings near US$825 million, so if you are weighing that against concerns about CRE concentration and credit losses, it is worth exploring how those assumptions might evolve from here.

Explore 4 other fair value estimates on Bank OZK - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Bank OZK research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Bank OZK research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bank OZK's overall financial health at a glance.

Curious About Other Options?

Our top stock finds are flying under the radar-for now. Get in early:

- Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com