- In recent days, Iran’s blocking of the Strait of Hormuz, a key route for about one-fifth of global oil and gas shipments, pushed oil prices higher and disrupted energy markets. This disruption highlights how companies such as TechnipFMC, which supplies technology, equipment and services to upstream producers, can see operating conditions change quickly as exploration and production plans adjust.

- We’ll now examine how this oil price shock and potential shift in upstream activity could influence TechnipFMC’s existing investment narrative centered on subsea strength and recurring services.

- We’ll now explore how the Strait of Hormuz disruption and higher oil prices could affect TechnipFMC’s subsea-driven investment narrative and risks.

This technology could replace computers: discover 25 stocks that are working to make quantum computing a reality.

TechnipFMC Investment Narrative Recap

To own TechnipFMC, you need to believe that its subsea technology, project execution and recurring services can stay attractive even as oil price and activity cycles shift. The Strait of Hormuz disruption and higher oil prices could support near term subsea project sanctioning, while the biggest current risk remains volatility in operator capex that could delay awards and make TechnipFMC’s backlog and earnings less predictable. Overall, the immediate impact of this event on the core narrative looks limited.

In February 2026, TechnipFMC raised its 2026 Subsea revenue guidance to US$9.2 billion to US$9.6 billion, reinforcing the importance of subsea strength as a key catalyst. That guidance was issued before the Strait of Hormuz disruption, so investors may now reassess how sustained oil price changes or geopolitical tensions could influence the timing of new offshore awards and the achievability of that outlook.

Yet, higher oil prices also bring a risk investors should be aware of, including the potential for prolonged commodity volatility to...

Read the full narrative on TechnipFMC (it's free!)

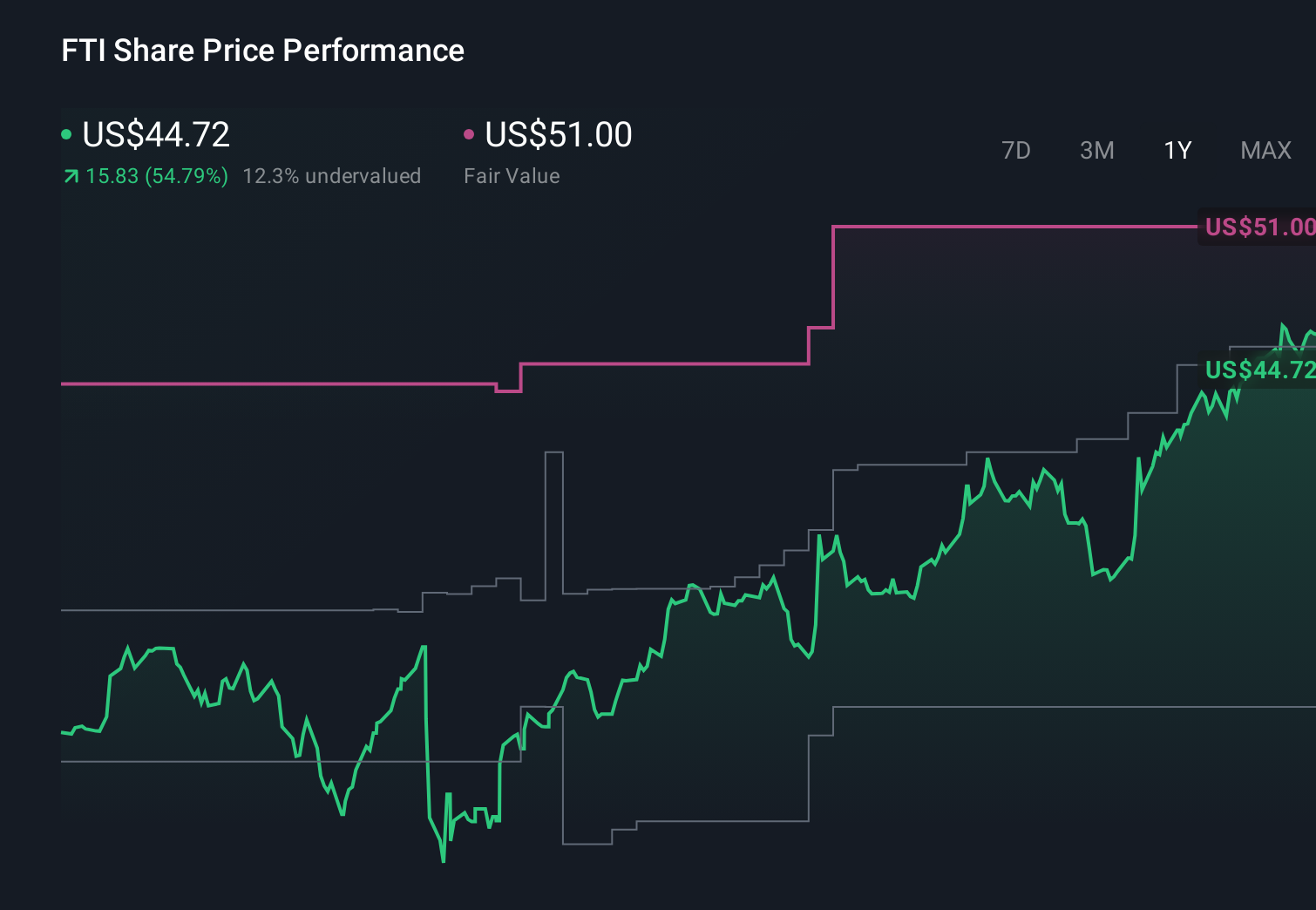

TechnipFMC's narrative projects $11.3 billion revenue and $1.2 billion earnings by 2028.

Uncover how TechnipFMC's forecasts yield a $62.62 fair value, a 10% downside to its current price.

Exploring Other Perspectives

You should know that the most cautious analysts were already assuming only about 4.2% annual revenue growth and modest margin pressure before this shock, so their US$936.4 million 2028 earnings view could shift meaningfully as oil prices and project risks evolve.

Explore 4 other fair value estimates on TechnipFMC - why the stock might be worth as much as 17% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your TechnipFMC research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free TechnipFMC research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate TechnipFMC's overall financial health at a glance.

No Opportunity In TechnipFMC?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Invest in the nuclear renaissance through our list of 94 elite nuclear energy infrastructure plays powering the global AI revolution.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com