- In March 2026, CACI International Inc. was awarded a five-year expertise task order valued at up to US$85,000,000 to continue providing engineering, technical support, data analysis, software development, and cybersecurity services for the U.S. Navy Naval Surface Warfare Center Carderock Division under the SeaPort Next Generation contract vehicle.

- This contract underscores CACI’s role in supporting advanced naval vessel design and control systems, reinforcing its position in high-value defense technology and cybersecurity services.

- Next, we’ll examine how this new Navy task order, emphasizing software and cybersecurity capabilities, may influence CACI’s existing investment narrative.

Find 62 companies with promising cash flow potential yet trading below their fair value.

CACI International Investment Narrative Recap

To be a shareholder in CACI, you generally need to believe in its role as a trusted, tech-focused contractor across defense, intelligence, and federal missions, with contract wins helping offset budget and procurement uncertainty. The new US$85,000,000 Navy Carderock task order reinforces CACI’s software and cybersecurity positioning, but is relatively small in the context of multi‑billion‑dollar annual revenue, so it is unlikely to change the near term catalyst around federal funding visibility or the key risk of contract timing and budget volatility in a major way.

Among recent announcements, the five year, up to US$416,000,000 NAVSEA NMMES modernization task order is especially relevant. Like the Carderock award, it leans heavily on CACI’s software, IT modernization, and data capabilities for the Navy, but at a larger scale. Together, these contracts highlight how CACI’s pipeline of Navy and Defense work ties directly into the core catalyst of increased demand for higher value, software and cyber centric federal programs.

Yet, against these positives, investors should be aware that concentrated exposure to shifting U.S. defense priorities could still...

Read the full narrative on CACI International (it's free!)

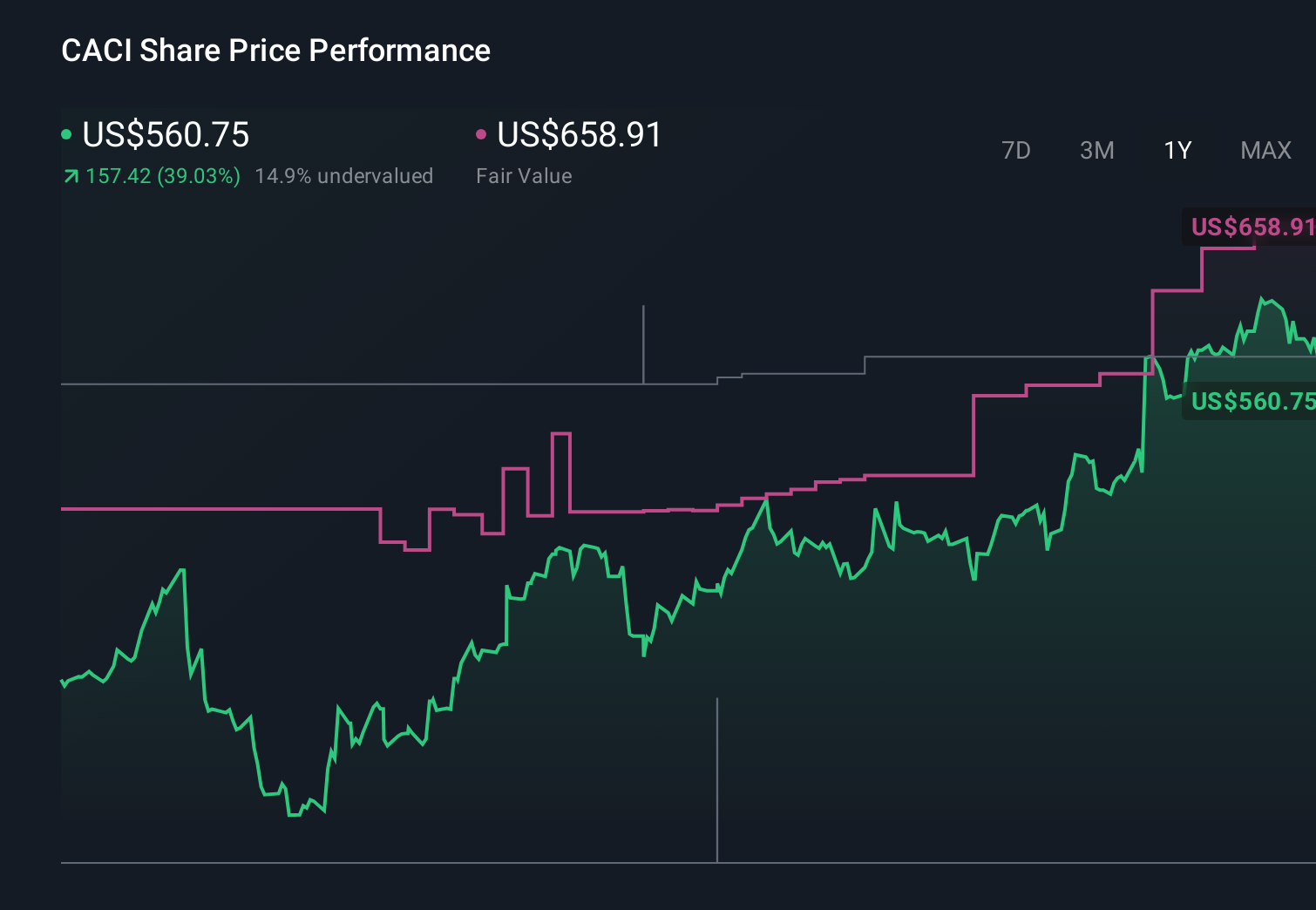

CACI International's narrative projects $10.4 billion revenue and $634.1 million earnings by 2028. This requires 6.5% yearly revenue growth and about a $134 million earnings increase from $499.8 million today.

Uncover how CACI International's forecasts yield a $718.08 fair value, a 25% upside to its current price.

Exploring Other Perspectives

Compared with the baseline view, the lowest analysts draw a much more pessimistic picture, even while assuming revenue of about US$11.8 billion and earnings near US$728 million by 2029, arguing that federal budget scrutiny and automation could restrain CACI more than the new Navy software and cyber wins suggest, so you may want to weigh how this fresh contract news could shift those expectations.

Explore 4 other fair value estimates on CACI International - why the stock might be worth as much as 63% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your CACI International research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free CACI International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CACI International's overall financial health at a glance.

Looking For Alternative Opportunities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Explore 25 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com