- In March 2026, Philip Morris International disclosed that shareholder advocacy group As You Sow filed a proposal urging the company to publish a report on the reputational, financial, and operational risks of not assuming responsibility for cigarette filter cleanup costs, while the board advised investors to vote against it at the May 6, 2026 annual meeting.

- This push for transparency on environmental liabilities contrasts with PMI’s broader messaging around its smoke-free transformation and sustainability agenda, raising questions about how comprehensively the company is addressing tobacco-related waste in its long-term plans.

- We’ll now examine how this shareholder push on filter cleanup responsibility may influence Philip Morris International’s investment narrative.

We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Philip Morris International Investment Narrative Recap

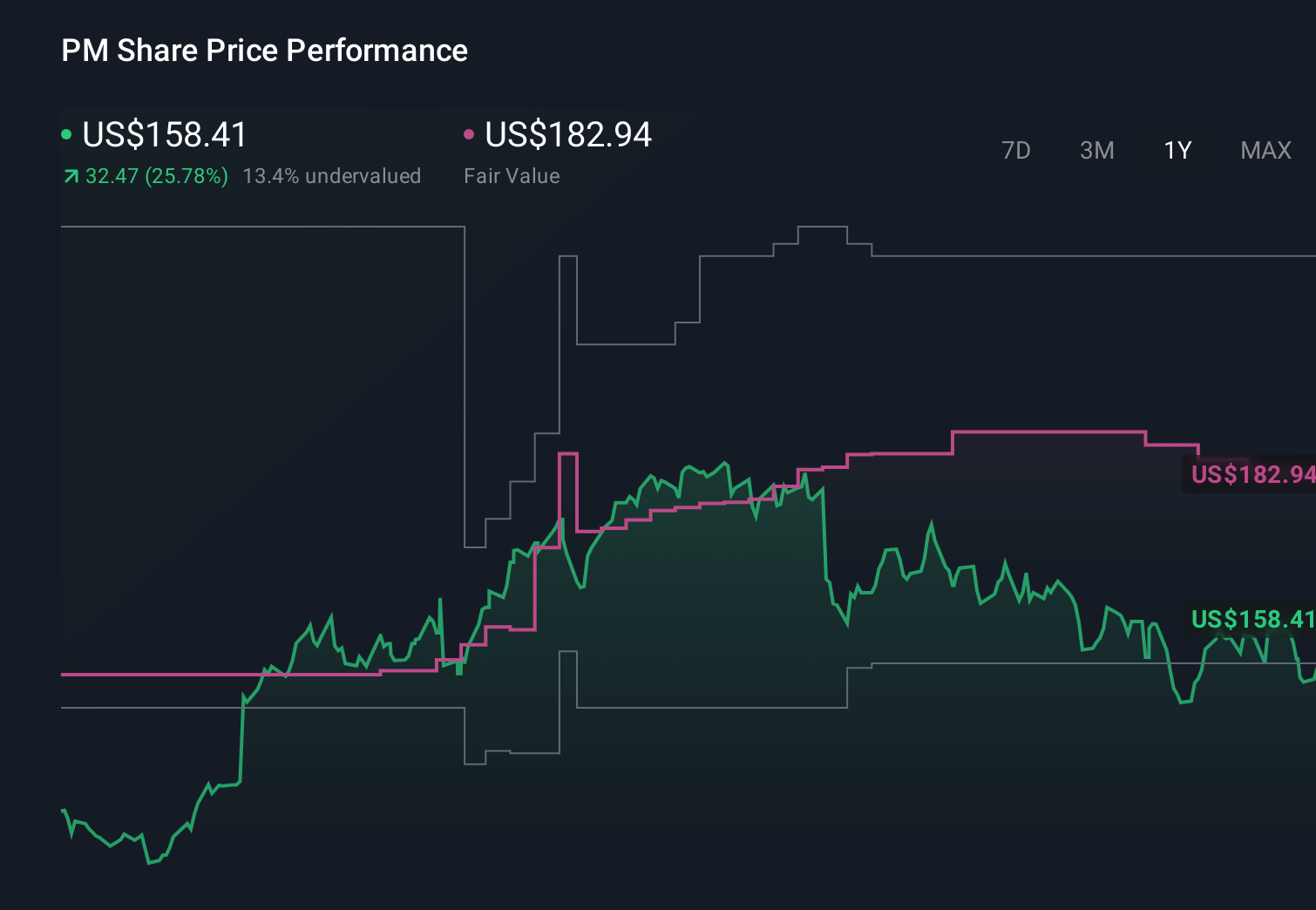

To own Philip Morris International, you need to believe its shift toward smoke free products can offset pressure on traditional cigarettes and support its dividend focused profile. Right now, the key near term catalyst is regulatory clarity on products like IQOS and ZYN, while the biggest risk is tightening global rules on both nicotine and waste. The new shareholder proposal on filter cleanup looks directionally important for ESG perception but is unlikely to be a primary near term driver.

The As You Sow proposal lands just after PMI released its Value Report 2025 and unveiled the Value Plan 2030+, which lists “circularity” and “nature and biodiversity” among six long term priorities. That corporate roadmap already puts environmental topics on the agenda, and investors may now watch how consistently PMI’s responses to tobacco waste, including filters, line up with those stated goals as regulators and ESG focused shareholders scrutinize its smoke free narrative.

Yet behind PMI’s smoke free push, investors should also be aware of growing regulatory scrutiny of nicotine pouches and IQOS that could...

Read the full narrative on Philip Morris International (it's free!)

Philip Morris International's narrative projects $49.4 billion revenue and $14.5 billion earnings by 2028. This requires 8.2% yearly revenue growth and a $6.3 billion earnings increase from $8.2 billion today.

Uncover how Philip Morris International's forecasts yield a $180.38 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already cautious, assuming revenue of about US$47.1 billion and earnings of roughly US$14.4 billion by 2028, and they see filter related ESG pressure as reinforcing the risk that heavier regulation and public health skepticism could still cap the upside, so if you are weighing PMI today it is worth knowing how far opinions diverge and how this new proposal might shift those expectations.

Explore 9 other fair value estimates on Philip Morris International - why the stock might be worth just $170.00!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Philip Morris International research is our analysis highlighting 5 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Philip Morris International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Philip Morris International's overall financial health at a glance.

Ready For A Different Approach?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Explore 25 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Find 62 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com