- In recent sessions, Sunrun reported ongoing losses alongside expectations for a small per‑share loss and higher revenue, while also completing a US$431 million securitization of residential solar assets and drawing fresh analyst support.

- This combination of stronger sector sentiment, expanded financing capacity, and upgraded analyst views has sharpened attention on how effectively Sunrun can convert its growing asset base into sustainable cash generation.

- Next, we’ll examine how the latest securitization deal and analyst upgrades may reshape Sunrun’s investment narrative and risk‑reward profile.

Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

Sunrun Investment Narrative Recap

To own Sunrun, you need to believe residential solar and storage can keep gaining traction despite incentive cliffs, financing demands, and earnings volatility. The recent earnings expectations for a small per share loss and stronger revenue, alongside sector strength and fresh analyst support, highlight the near term catalyst of improved cash generation, while the biggest current risk remains Sunrun’s dependence on affordable financing and securitizations to fund its growth. This latest news does not materially change that core tradeoff.

The new US$431 million securitization stands out because it directly relates to that financing risk. By turning existing residential solar assets into long term funding, Sunrun reinforces its ability to keep installing systems and expanding its subscriber base, which underpins the longer term opportunity in storage, grid services, and recurring revenue. At the same time, it underlines how much the business model still leans on steady access to capital markets.

But while sentiment has improved, investors should also be aware that Sunrun’s reliance on debt markets and securitizations could become a real pressure point if...

Read the full narrative on Sunrun (it's free!)

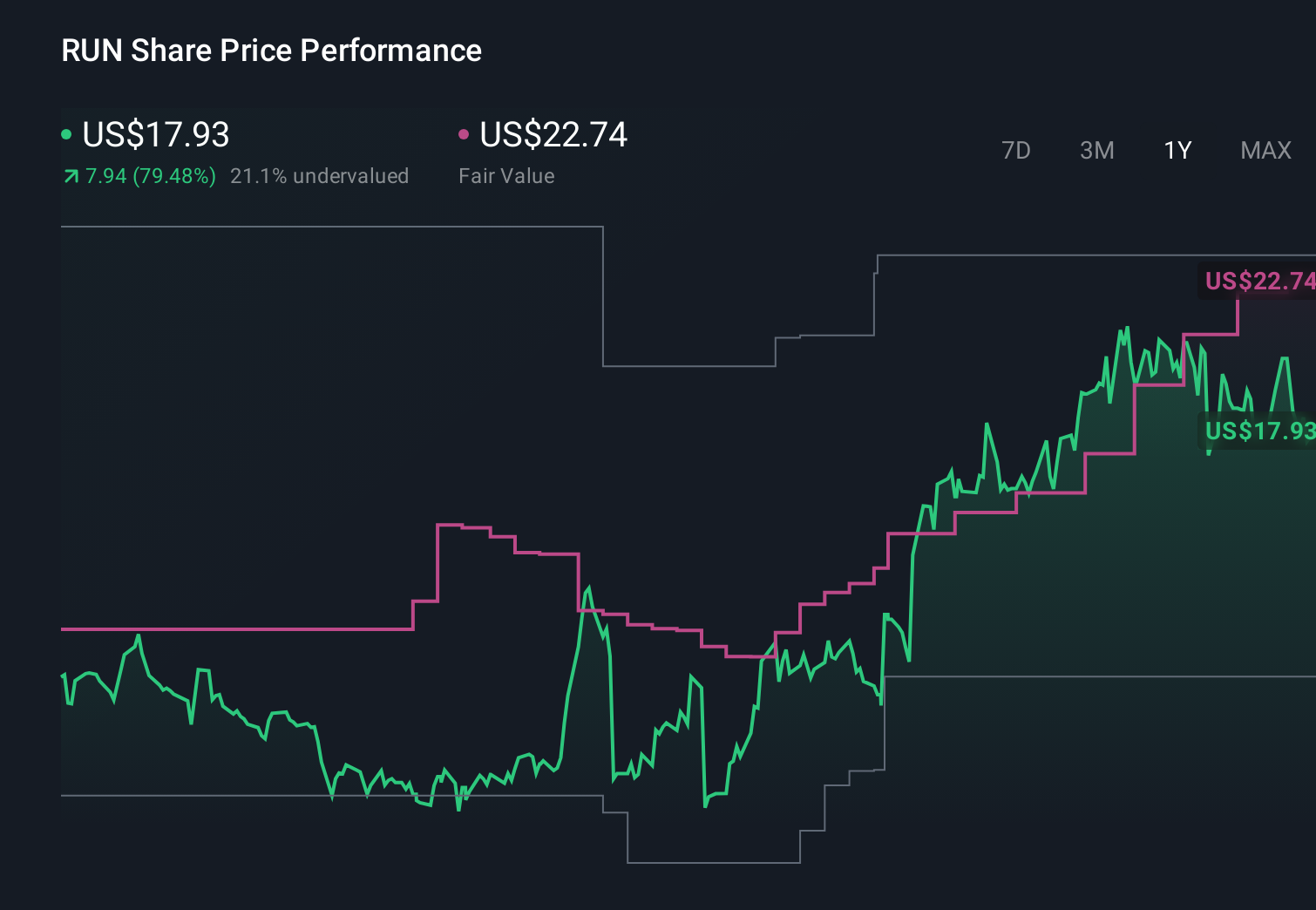

Sunrun's narrative projects $2.9 billion revenue and $465.4 million earnings by 2028. This requires 10.4% yearly revenue growth and about a $3.1 billion earnings increase from -$2.6 billion today.

Uncover how Sunrun's forecasts yield a $22.20 fair value, a 64% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts expect Sunrun to reach about US$3.8 billion in revenue and US$1.6 billion in earnings by 2028, which is a far more upbeat story than the cautious focus on financing risk and tax credit sunsets you have just read, and this upbeat view could be reassessed in light of the recent loss expectations and securitization news.

Explore 3 other fair value estimates on Sunrun - why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Sunrun research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Sunrun research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Sunrun's overall financial health at a glance.

Looking For Alternative Opportunities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 26 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

- Explore 25 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com