- In recent weeks, Southern California Gas Company reported that its four underground natural gas storage fields helped SoCalGas and San Diego Gas & Electric customers avoid over US$120 million in potential energy costs during January’s Winter Storm Fern by drawing on lower-cost gas purchased earlier.

- A separate upgrade from Wells Fargo highlighted Sempra’s ongoing business simplification and capital reallocation efforts, emphasizing how pending transactions could sharpen its focus on regulated utility operations and capital efficiency.

- We’ll now examine how Wells Fargo’s upgrade, emphasizing business simplification and capital allocation shifts, could influence Sempra’s existing investment narrative.

Rare earth metals are the new gold rush. Find out which 26 stocks are leading the charge.

Sempra Investment Narrative Recap

To own Sempra, you generally need to believe in the resilience of regulated utilities in California and Texas, plus disciplined capital recycling from non-core assets. The SoCalGas storage performance during Winter Storm Fern reinforces the reliability pillar of that thesis, but it does not materially change the near term focus on executing planned asset sales and managing regulatory risk around decarbonization and affordability in key jurisdictions.

The Wells Fargo upgrade, centered on business simplification and capital reallocation, feels most relevant here because it directly touches Sempra’s ongoing shift toward regulated utility operations. That lens helps frame SoCalGas’s storage success as part of a broader effort to highlight stability and capital efficiency while the company progresses with the KKR partnership and Ecogas sale and works to keep earnings quality and credit metrics aligned with higher regulated investment needs.

Yet despite this emphasis on reliability, investors still need to understand how more aggressive California decarbonization or affordability reforms could...

Read the full narrative on Sempra (it's free!)

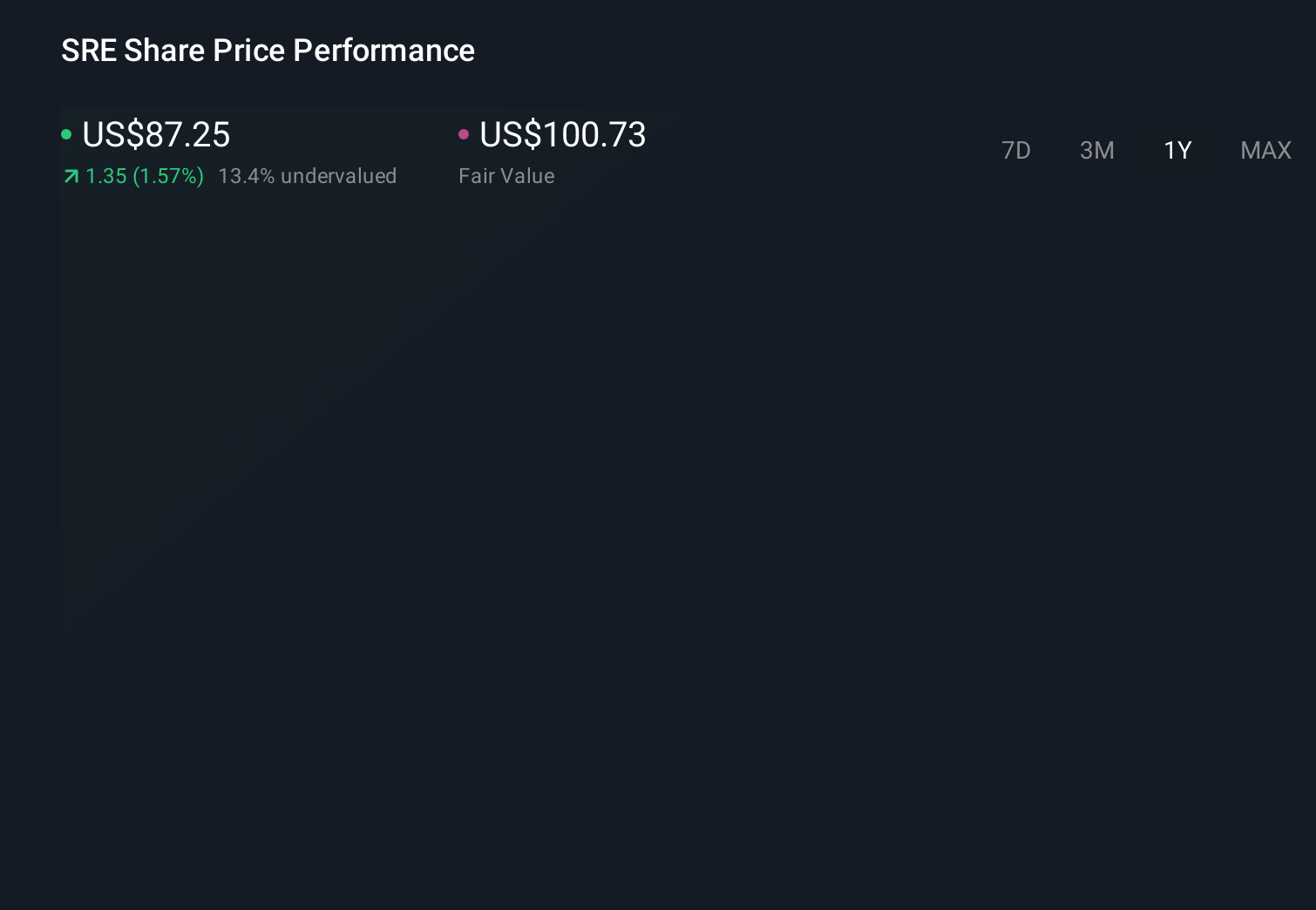

Sempra's narrative projects $14.3 billion revenue and $4.0 billion earnings by 2029. This requires 1.5% yearly revenue growth and a $2.2 billion earnings increase from $1.8 billion today.

Uncover how Sempra's forecasts yield a $102.56 fair value, a 3% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members see fair values for Sempra ranging from about US$22 to US$103 across 2 independent views, underlining how far opinions can spread. Set against that, the current focus on capital recycling into regulated utilities and the associated regulatory risks could materially influence how future returns are shared between customers and shareholders, so you may want to weigh several of these perspectives before deciding what feels reasonable.

Explore 2 other fair value estimates on Sempra - why the stock might be worth less than half the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Sempra research is our analysis highlighting 1 key reward and 4 important warning signs that could impact your investment decision.

- Our free Sempra research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Sempra's overall financial health at a glance.

Searching For A Fresh Perspective?

Our top stock finds are flying under the radar-for now. Get in early:

- Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 22 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com