- InterDigital, Inc. recently secured a preliminary injunction in Brazil against Transsion over alleged 5G patent infringement and announced new patent license agreements with Buffalo Americas, Inc. for Wi‑Fi 5 and Wi‑Fi 6, along with fresh deals with a global TV manufacturer.

- Together, these legal and licensing developments underscore InterDigital’s ability to both enforce and commercialize its wireless intellectual property across smartphones, networking gear, and consumer electronics.

- We’ll now examine how the Brazilian court injunction, in particular, could reshape InterDigital’s investment narrative and future licensing outlook.

We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

InterDigital Investment Narrative Recap

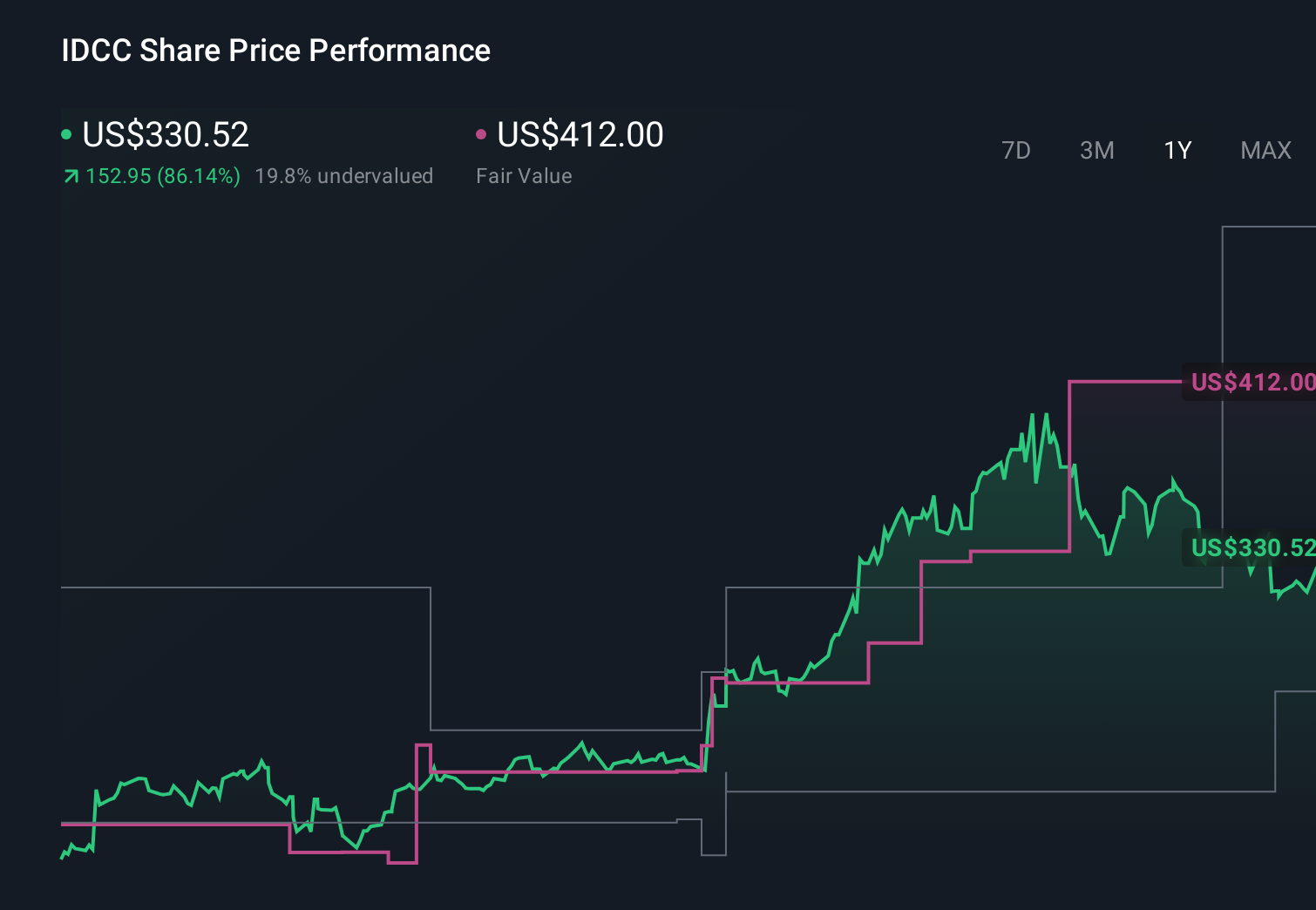

To own InterDigital, I think you need to believe in the durability and breadth of its patent licensing engine across 5G, Wi Fi, video, and consumer electronics, and that it can keep converting this IP into high margin, recurring cash flows. The Brazilian 5G injunction and new Wi Fi and TV licenses both speak directly to that, reinforcing enforcement strength and diversification, while also highlighting that legal outcomes and patent disputes remain a central near term risk.

Among the latest announcements, the new Buffalo Americas Wi Fi 5 and Wi Fi 6 license, alongside agreements with a global TV manufacturer, feels most connected to this story. Together with the Brazilian ruling, it pairs legal validation of InterDigital’s 5G patents with fresh proof that the company can sign deals across networking gear and consumer electronics, which matters for the current catalyst of expanding recurring revenue beyond smartphones.

But even with these wins, the biggest risk investors should be aware of is how dependent InterDigital’s long term earnings power is on evolving patent rules and enforcement...

Read the full narrative on InterDigital (it's free!)

InterDigital's narrative projects $633.9 million revenue and $173.4 million earnings by 2028. This requires a 10.8% yearly revenue decline and a $290.1 million earnings decrease from $463.5 million.

Uncover how InterDigital's forecasts yield a $462.67 fair value, a 48% upside to its current price.

Exploring Other Perspectives

Before this injunction, the most optimistic analysts were assuming revenue could reach about US$1.0 billion with earnings near US$487.6 million, yet the Brazilian ruling and rising worries about regulatory pushback on patent enforcement show how differently you and those analysts might weigh upside versus the risk that tougher IP rules or royalty free standards reshape that story.

Explore 6 other fair value estimates on InterDigital - why the stock might be worth 47% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your InterDigital research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free InterDigital research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate InterDigital's overall financial health at a glance.

Want Some Alternatives?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Rare earth metals are the new gold rush. Find out which 26 stocks are leading the charge.

- Outshine the giants: these 22 early-stage AI stocks could fund your retirement.

- Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com