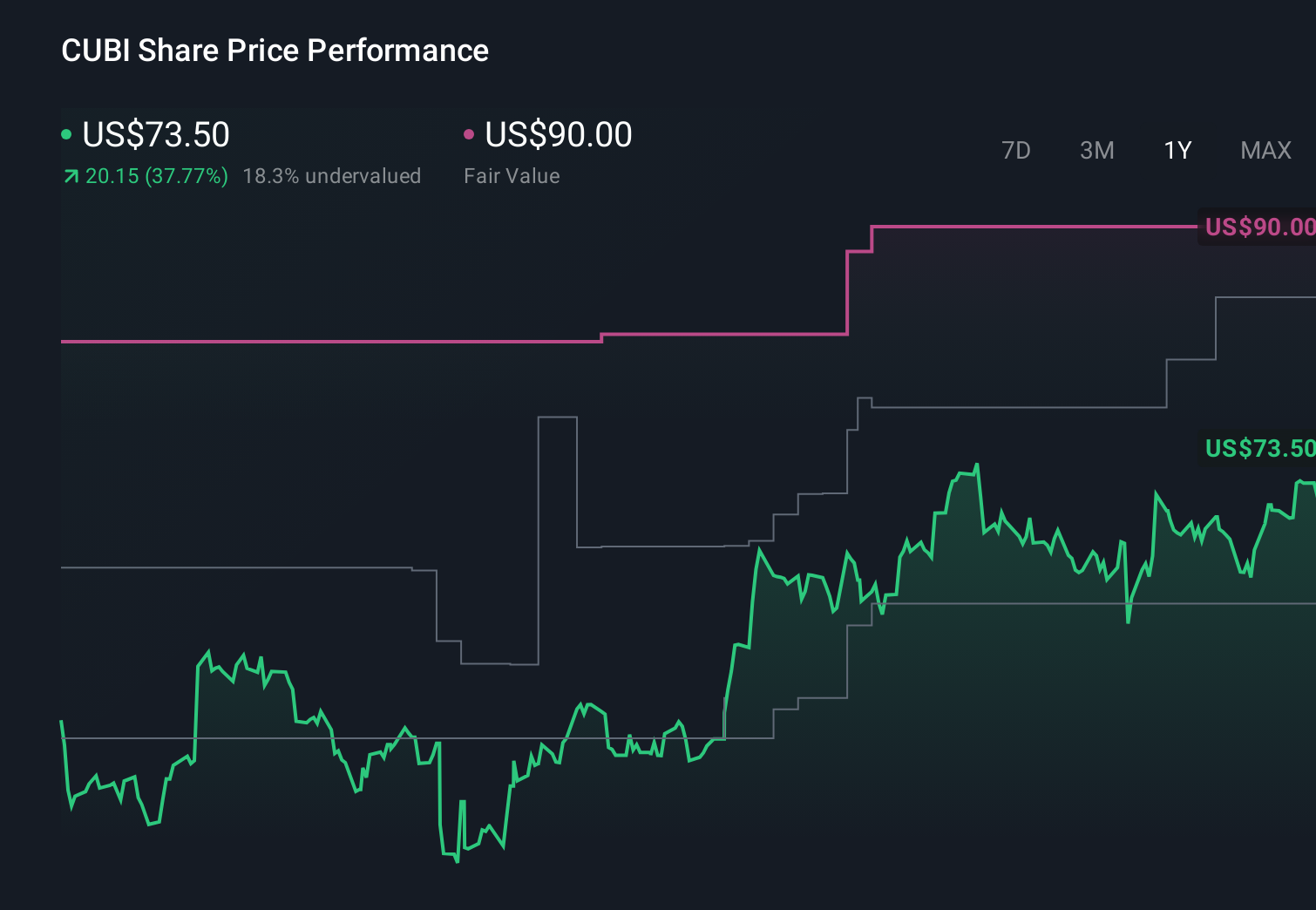

- In March 2026, Customers Bancorp reported quarterly results with year-on-year revenue growth above analyst forecasts and a small earnings per share beat.

- Ahead of these results, board member Robert N. Mackay disclosed plans to retire after the 2026 Annual Meeting to focus on his external CEO role, with no disagreements cited over the bank’s operations or policies.

- We’ll now examine how this earnings outperformance shapes Customers Bancorp’s investment narrative, particularly in relation to its technology-driven banking model.

Find 62 companies with promising cash flow potential yet trading below their fair value.

Customers Bancorp Investment Narrative Recap

To own Customers Bancorp, you need to believe its technology-led cubiX platform can keep attracting sticky commercial deposits and fee income while managing the concentration and regulatory risks around digital assets. The latest quarter’s revenue and EPS beat supports that tech-forward narrative, but the share price drop since results highlights how sensitive sentiment remains to perceived risk in cubiX deposits and regulatory scrutiny. Mackay’s planned board retirement, as disclosed, does not appear to materially change the near term catalysts or key risks.

The most relevant recent announcement here is the new US$100 million share repurchase program authorized in February 2026. In the context of an earnings beat but a falling share price, this buyback can matter for near term upside if management keeps shrinking the share count while the market debates the sustainability of cubiX driven growth and the cost of staying ahead on technology and compliance.

Yet against this, investors should be aware that concentration in cubiX related deposits could quickly become a problem if...

Read the full narrative on Customers Bancorp (it's free!)

Customers Bancorp's narrative projects $977.5 million revenue and $424.9 million earnings by 2028. This requires 17.9% yearly revenue growth and a $293.3 million earnings increase from $131.6 million today.

Uncover how Customers Bancorp's forecasts yield a $87.00 fair value, a 24% upside to its current price.

Exploring Other Perspectives

Before this latest update, the most pessimistic analysts were still assuming earnings could reach about US$361.9 million by 2028, yet they worry that rising fintech competition and digital disruption could blunt the payoff from CUBI’s tech investments, reminding you that reasonable people can look at the same numbers and reach very different conclusions.

Explore 3 other fair value estimates on Customers Bancorp - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Customers Bancorp research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Customers Bancorp research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Customers Bancorp's overall financial health at a glance.

No Opportunity In Customers Bancorp?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

- Rare earth metals are the new gold rush. Find out which 26 stocks are leading the charge.

- Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com