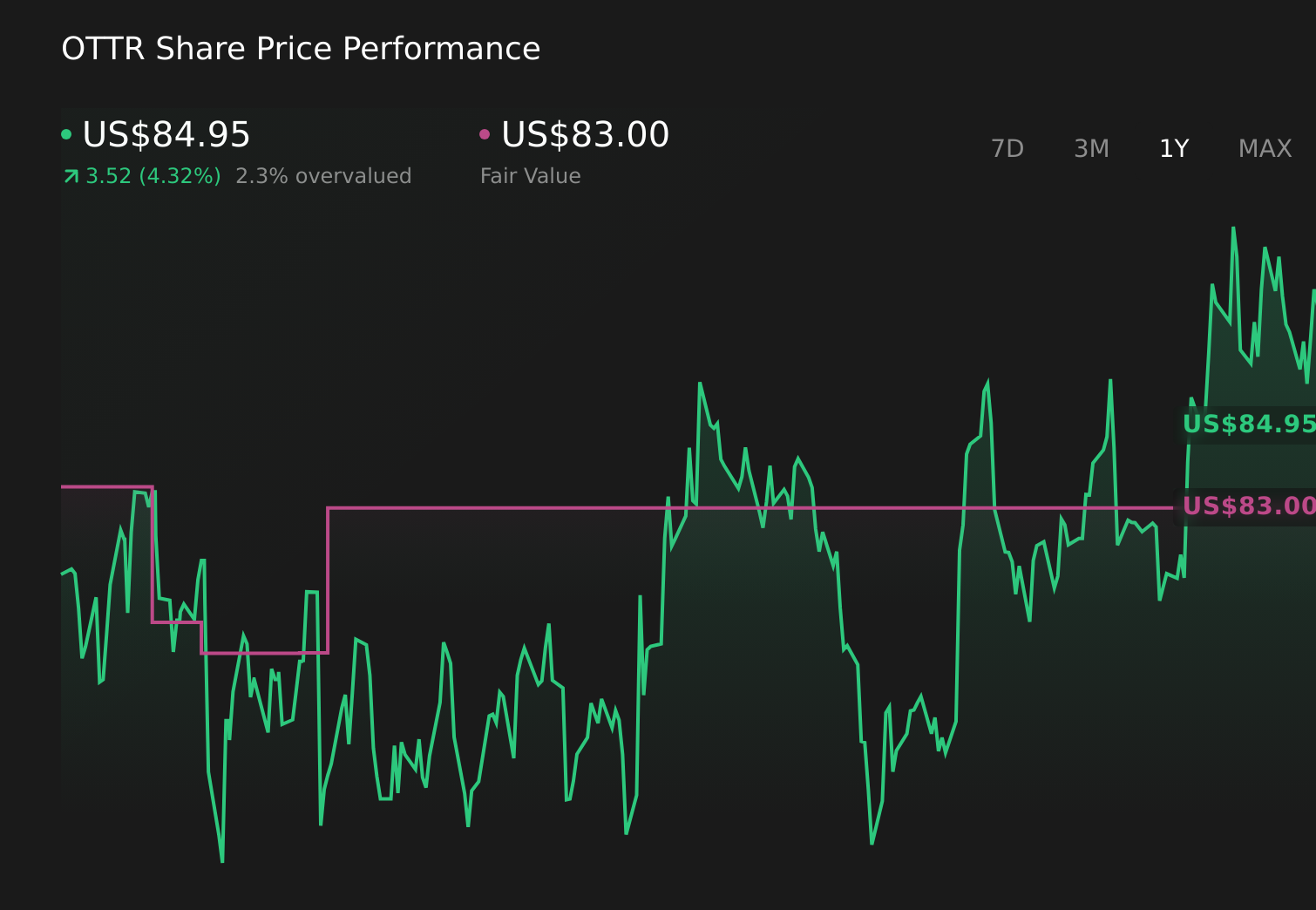

- Recently, Zacks upgraded Otter Tail to a Rank #2 (Buy) after analysts revised their earnings forecasts higher, signaling a more favorable outlook for the company’s future profits.

- This shift in analyst expectations highlights how changes in projected earnings alone, without new operational announcements, can meaningfully influence market perceptions of Otter Tail.

- We’ll now examine how this earnings-driven analyst upgrade interacts with concerns about regulation, capital costs, and long-term profit pressure in Otter Tail’s investment narrative.

AI is about to change healthcare. These 37 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Otter Tail Investment Narrative Recap

To own Otter Tail, you need to believe its regulated utility, manufacturing, and plastics businesses can collectively sustain solid cash flows despite earnings forecasts that currently point to pressure rather than growth. The Zacks Rank upgrade reflects higher earnings estimates in the near term, but it does not materially change the key short term catalyst, which remains execution on its capital plan, or the biggest risk, which is rising capital costs eating into returns.

The most relevant recent development alongside the Zacks upgrade is Otter Tail’s full year 2026 diluted EPS guidance of US$5.22 to US$5.62, issued in February 2026. This guidance frames the upgraded earnings expectations against a backdrop of elevated interest rates and a US$1.4 billion capital plan that could strain free cash flow and increase funding costs if borrowing remains expensive or credit conditions tighten.

Yet behind the improved earnings outlook, investors should be aware that higher interest rates could still...

Read the full narrative on Otter Tail (it's free!)

Otter Tail's narrative projects $1.4 billion revenue and $186.1 million earnings by 2029. This requires 3.1% yearly revenue growth and a $89.8 million earnings decrease from $275.9 million today.

Uncover how Otter Tail's forecasts yield a $86.50 fair value, in line with its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community currently see Otter Tail’s fair value between US$65.27 and US$86.50, underscoring how far opinions can spread. Set this against the risk that elevated interest rates and a sizeable US$1.4 billion capital program could pressure future earnings, and it becomes important to weigh several different views before deciding how Otter Tail might fit in your portfolio.

Explore 3 other fair value estimates on Otter Tail - why the stock might be worth 26% less than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Otter Tail research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Otter Tail research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Otter Tail's overall financial health at a glance.

Want Some Alternatives?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

- Find 62 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com