Arbor Realty Trust (ABR) recently closed a US$762.6m commercial real estate mortgage loan securitization, a financing move that reshapes its funding mix and supports ongoing lending and investment activity.

See our latest analysis for Arbor Realty Trust.

Despite the fresh securitization and recent preferred dividend declaration, Arbor Realty Trust’s 30 day share price return decline of 12.69% and 1 year total shareholder return decline of 24.33% suggest momentum has softened rather than built over time.

If this financing story has you looking beyond a single lender, it could be a good moment to see what else is moving and uncover 20 top founder-led companies

With Arbor trading at US$7.50, sitting at a 15% discount to the US$8.63 analyst target and an estimated 33% intrinsic discount, investors need to consider whether this represents genuine value or whether the market already reflects its outlook.

Most Popular Narrative: 38% Undervalued

With Arbor Realty Trust last closing at $7.50 against a most-followed fair value estimate of $12.00, the prevailing narrative sees a meaningful valuation gap and focuses on how the earning power of the loan book evolves from here.

The analysts have a consensus price target of $12.312 for Arbor Realty Trust based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $15.0, and the most bearish reporting a price target of just $10.5.

Want to see what sits behind that valuation gap? The narrative focuses on shifting revenue, expanding margins and a higher future earnings multiple. The tension between slower top line and firmer profitability is central. If you care which assumptions really carry the fair value, the full narrative lays them out clearly.

Result: Fair Value of $12 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the story can change if agency production weakens further or if dividend payouts reset closer to earnings guidance. This would challenge the current undervalued narrative.

Find out about the key risks to this Arbor Realty Trust narrative.

Another Take: Multiples Paint a Tighter Picture

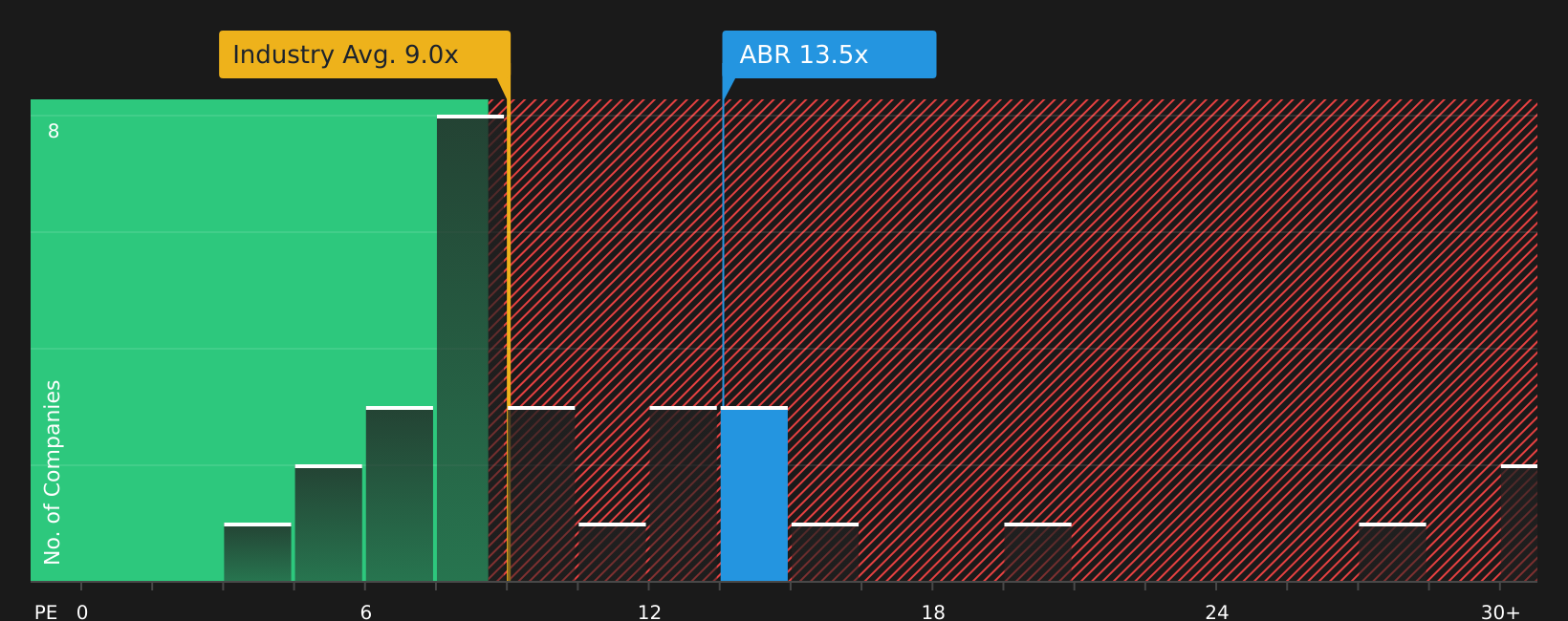

Analyst and DCF style work sees Arbor trading at roughly a 33% discount to an estimated fair value of $11.21, yet the current P/E of 13.5x is slightly above the fair ratio of 13.4x and materially above the US Mortgage REITs average of 8.7x. Is this a margin of safety or a sign that expectations are already loaded into the price?

To see how that small gap between the current P/E, the fair ratio and the wider industry could matter for your risk and return trade off, take a closer look at the valuation breakdown: See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Mixed signals or a clear message for you as an investor? With both risks and rewards identified, move quickly to check the full picture through 2 key rewards and 3 important warning signs

Looking for more investment ideas?

If Arbor has sharpened your thinking, do not stop here. Use focused stock lists to spot opportunities that fit your goals before the crowd catches on.

- Target potential bargains by scanning companies that combine quality metrics with low valuations using the 59 high quality undervalued stocks.

- Strengthen your income stream by focusing on companies with higher yields and resilient payouts through the 13 dividend fortresses.

- Keep risk in check by filtering for businesses with sturdier finances using the solid balance sheet and fundamentals stocks screener (40 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com