Goldman Sachs recently added Citizens Financial Group (CFG) to its US Conviction List. This move has sharpened investor focus on the bank’s private banking growth, efficiency program, liquidity, and capital returns.

See our latest analysis for Citizens Financial Group.

CFG’s recent addition to the US Conviction List comes after a period of steady share price momentum, with a 7 day share price return of 5.56% and a 1 year total shareholder return of 84.48% signaling strong recent interest.

If this kind of performance has you thinking about what else might be setting up for strong returns, it could be worth scanning 20 top founder-led companies

With CFG trading at $60.99, alongside an intrinsic value estimate that implies a 43% discount and analyst targets sitting higher, the key question is simple: is this still an undervalued bank, or has the market already priced in future growth?

Most Popular Narrative: 29.7% Undervalued

At a last close of $60.99 versus a fair value of $86.72, the most followed narrative argues that Citizens Financial Group still trades at a meaningful discount.

Citizens Financial is currently $43.60. They will be releasing their quarterly report tomorrow morning during Pre-Market. Currently up 30.96% for the year, and 13.61% out of the last three months. Known for major spikes during the releases of their reports. Here at The Daily Investors, we are expecting a Beat tomorrow. The current estimate is +.79 cents. We are estimating a gain of around +.83 cents. Their last earnings release proved that their company is making a turn around. Several technical signals are showing a positive up trend turning around from their previous two beats. With the economy growing better on a monthly basis, expect to see another leap ahead to join with their fellow banking peers.

According to DailyInvestors, this fair value hinges on a mix of accelerating earnings, firmer margins, and a richer profit multiple than the market currently credits. It is worth examining which specific growth rates and profitability targets sit behind that $86.72 figure and the projected valuation rerating.

Result: Fair Value of $86.72 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this depends on earnings, margins, and valuation multiples remaining stable. Any earnings disappointment or weaker profitability could quickly challenge the 29.7% undervalued narrative.

Find out about the key risks to this Citizens Financial Group narrative.

Another View: What The Market Multiple Is Saying

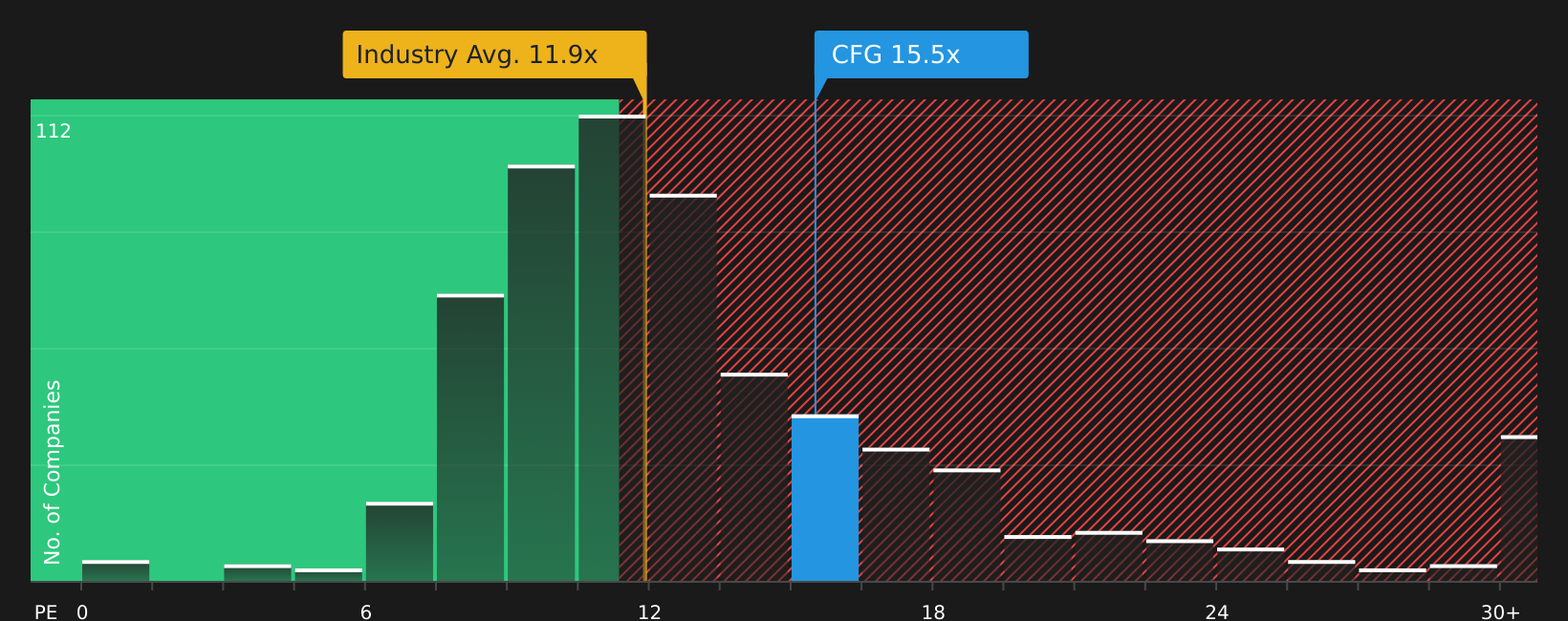

The user narrative leans heavily on fair value estimates, but the current P/E of 15.4x tells a more cautious story. That is higher than both peers at 12.3x and the US banks average at 11.4x, even though the fair ratio of 19.6x suggests the market could still move closer to that level. Is this a reasonable premium, or a sign that expectations are already running hot?

For a closer look at how this pricing gap lines up against earnings power, check the valuation breakdown in our detailed multiples view, including banking peers and the fair ratio context, via the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment divided between undervaluation potential and a full P/E, it makes sense to review the numbers yourself and decide where you stand. Investors are already highlighting some positives in the story, so check how these align with your own expectations in the 4 key rewards

Ready to hunt for your next idea?

If CFG has caught your attention, do not stop here. Broaden your watchlist now, or risk missing other setups that could fit your approach.

- Target strong cash generation and pricing power by scanning companies flagged as 59 high quality undervalued stocks that pair quality fundamentals with appealing valuations.

- Prioritise resilience and capital strength by reviewing stocks picked out in the solid balance sheet and fundamentals stocks screener (40 results) for robust financial footing.

- Get ahead of the crowd by checking the screener containing 25 high quality undiscovered gems highlighting lesser known names with solid underlying metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com