Emerson Electric (EMR) is back in focus after Jefferies shifted its stance to a more positive rating, citing solid order momentum, improving earnings prospects, and progress toward building a more focused automation business.

See our latest analysis for Emerson Electric.

The recent Jefferies upgrade and Emerson's selection to automate the Louisiana Green Fuels facility come after a mixed stretch, with a 7.4% 30 day share price decline but a 41.6% 1 year total shareholder return signaling longer term momentum.

If Emerson's automation exposure has caught your attention, this is a good moment to see what else is moving in industrial technology and energy infrastructure via 28 power grid technology and infrastructure stocks

With Emerson shares at $131.70, a 1-year total return of 41.6%, mixed recent price action, and an average analyst target well above the current level, should you see value still on the table or assume markets are already pricing in future growth?

Most Popular Narrative: 19.9% Undervalued

Emerson Electric's most followed narrative points to a fair value of about $164.51 per share, compared with the last close of $131.70, setting up a valuation story driven by automation and software.

The company's transformation toward a pure-play automation leader, emphasizing innovation, commercialization of new products, and operational excellence, continues to yield improved profitability (e.g., margin expansion, higher free cash flow) and positions Emerson to capitalize on long-term modernization and infrastructure trends.

Curious what kind of revenue trajectory, margin lift, and earnings profile sit behind that valuation gap? The narrative leans heavily on automation demand, software mix, and a richer profit structure. The full set of embedded assumptions might surprise you.

Result: Fair Value of $164.51 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on AspenTech execution and industrial software integration going smoothly, as well as on capital spending cycles not softening in key process and power markets.

Find out about the key risks to this Emerson Electric narrative.

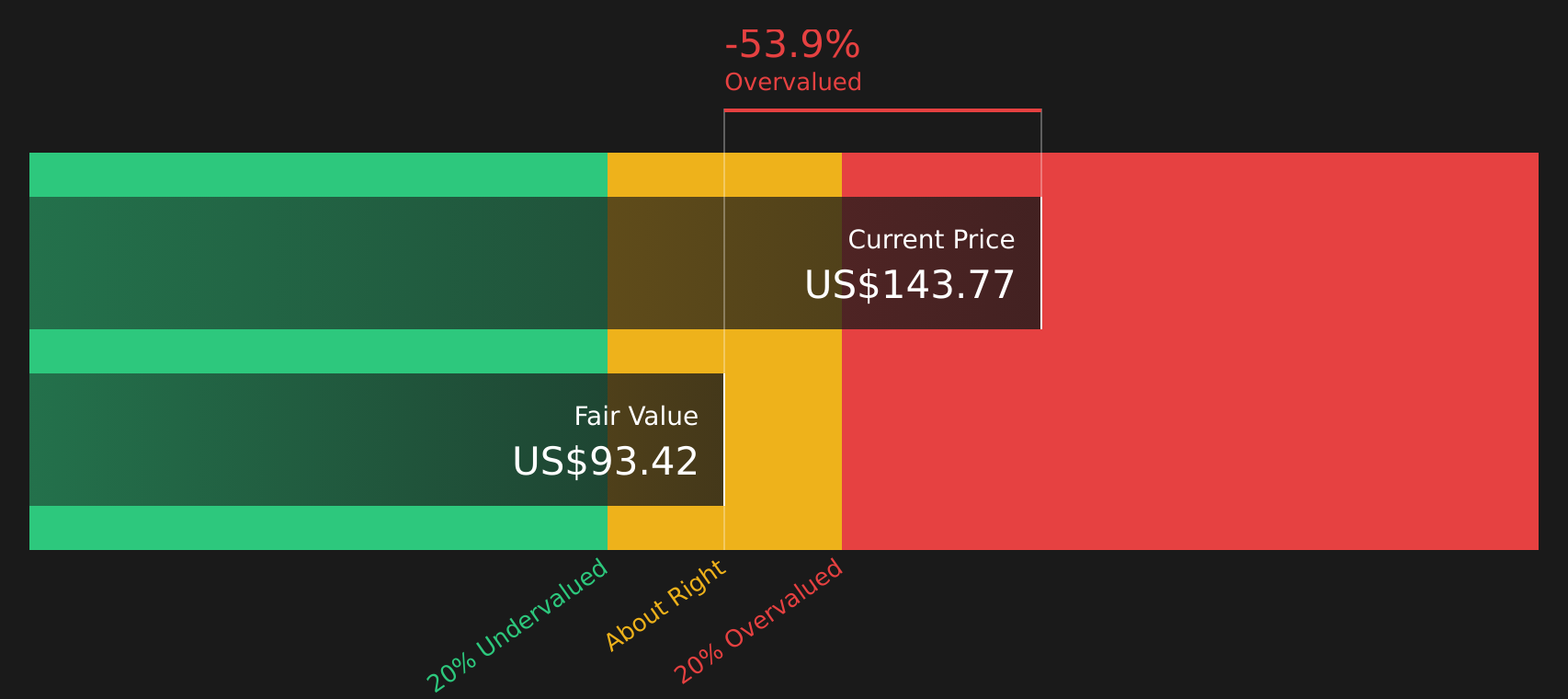

Another Angle: DCF Sends a Very Different Signal

The 19.9% undervaluation story built on analyst targets is not the only take. Simply Wall St's DCF model, which focuses on future cash flows, comes out closer to $93.06 per share, with Emerson shares at $131.70. That points to an overvalued picture instead. Which set of assumptions appears more realistic to you?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Emerson Electric for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 59 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment pulled in two directions by optimism on automation and tension around valuation, this is a good time to look through the underlying data yourself and decide how comfortable you are with the current setup, then weigh that against the company's mix of 6 key rewards and 2 important warning signs

Looking for more investment ideas?

If Emerson has you thinking more seriously about where to put your money next, do not stop here. The right watchlist additions often start with just one smart search.

- Target quality at a discount by scanning for companies that combine strong fundamentals with room for rerating via 59 high quality undervalued stocks

- Prioritise resilience and sleep a bit easier at night by focusing on businesses highlighted in the 68 resilient stocks with low risk scores

- Hunt for tomorrow's standouts before the crowd catches on by checking the screener containing 25 high quality undiscovered gems

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com