- On March 31, 2026, Ternium S.A. filed its 2025 Form 20-F with the SEC, outlining its operational, financial and sustainability progress, including investments in low-carbon steelmaking technologies and advanced products for the energy transition.

- The filing gives investors a more detailed view of how Ternium is positioning itself as a supplier of lower-emission steel solutions across the Americas, with an emphasis on sustainable mobility and transparency in reporting.

- Now, we’ll explore how Ternium’s emphasis on low-carbon steel investments in its latest 20-F could influence its broader investment narrative.

The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Ternium Investment Narrative Recap

Ternium’s investment case today rests on its push into higher value, lower emission steel across the Americas while managing a heavy capex cycle and exposure to Latin American demand and currencies. The new 2025 Form 20 F adds useful detail on decarbonization projects, but it does not materially change the near term balance between the main catalyst of successful project execution and the key risks of overcapacity, import pressure and elevated spending.

The most relevant recent update alongside the filing is the UBS analyst move on April 2, 2026, keeping a Neutral rating but lifting the price target to US$41, in line with the roughly US$40.50 consensus. That reinforces how the market was already framing Ternium’s low carbon investments and expansion plans ahead of the new disclosure, and it gives you a reference point for how quickly views could shift as fresh data on margins and cash flows comes through.

Yet behind this progress, investors should also be aware of the risk that rising decarbonization and energy costs could...

Read the full narrative on Ternium (it's free!)

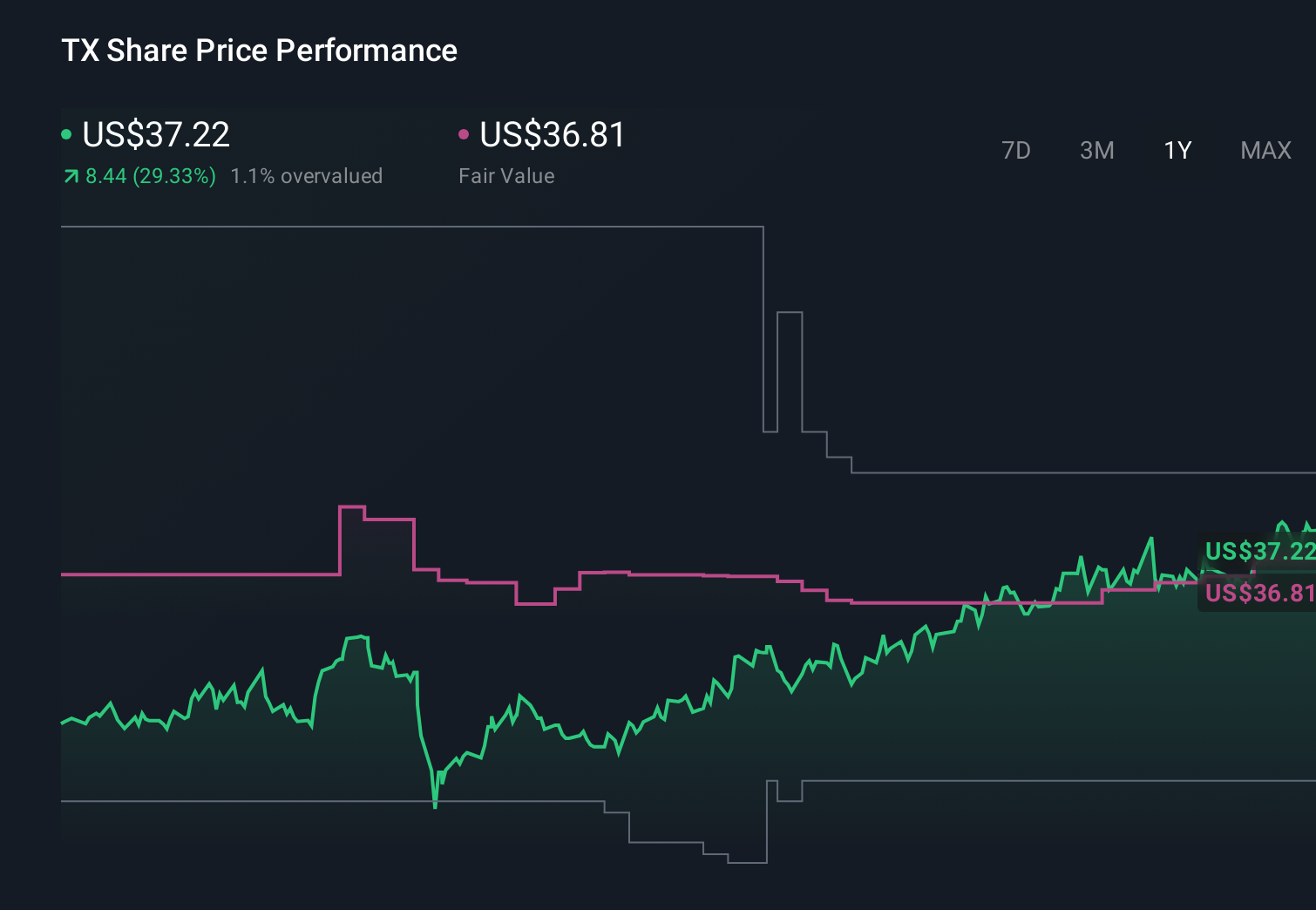

Ternium's narrative projects $18.5 billion revenue and $865.0 million earnings by 2029.

Uncover how Ternium's forecasts yield a $40.19 fair value, in line with its current price.

Exploring Other Perspectives

Compared with the baseline view, the most optimistic analysts were assuming Ternium could reach about US$19.8 billion in revenue and US$1.1 billion in earnings, so this new focus on low emission steel could either reinforce that greener growth story or prompt a rethink of how much risk you are willing to accept on execution and regional exposure.

Explore 4 other fair value estimates on Ternium - why the stock might be worth just $40.19!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Ternium research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Ternium research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ternium's overall financial health at a glance.

Want Some Alternatives?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

- AI is about to change healthcare. These 36 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com