Why UCT 3.0 and AI Demand Are Driving Fresh Interest in Ultra Clean

Ultra Clean Holdings (UCTT) is back on investor radars after its UCT 3.0 plan to expand manufacturing capacity for AI related demand, combined with inclusion in a recent “strongest buys” analyst list.

See our latest analysis for Ultra Clean Holdings.

At a share price of US$63.16, Ultra Clean has seen a 13.21% 1 month share price return and a 131.19% 3 month share price return. Its 1 year total shareholder return of 245.51% suggests strong momentum building around the UCT 3.0 story and AI related demand.

If UCT 3.0 and AI supply chains are on your radar, it can be useful to compare Ultra Clean with other potential beneficiaries using 36 AI infrastructure stocks

With the shares already up sharply and analysts setting an average price target of US$81.25, implying a discount of about 29% to that level, you have to ask: is there still an opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 22.3% Undervalued

Compared to the last close of $63.16, the most widely followed narrative anchors on a fair value of $81.25, built around UCT 3.0 and AI linked demand.

New product qualifications and business wins, especially at the Czech facility, are expected to contribute incremental revenue starting in Q4, positioning Ultra Clean to benefit from continued accelerated investment in advanced fabs and the robust outlook for semiconductor capital equipment spending (impacts revenue growth).

Curious what sits behind that revenue ramp story, the margin reset, and the earnings path that underpins this fair value? The narrative leans on specific growth, profitability, and valuation assumptions that paint a very different picture to the current share price.

Result: Fair Value of $81.25 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still clear pressure points, including high dependence on a small group of large customers and ongoing tariff related costs that weigh on margins and cash flow resilience.

Find out about the key risks to this Ultra Clean Holdings narrative.

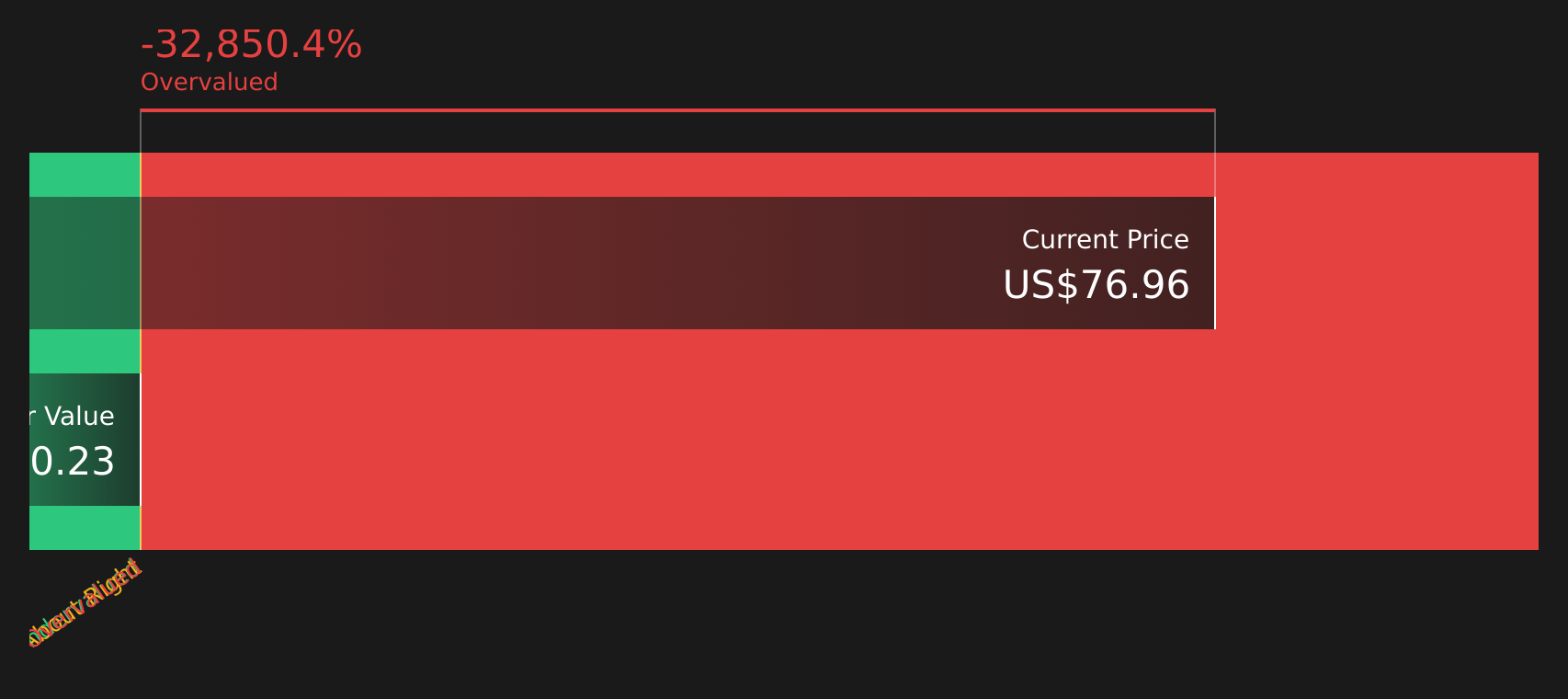

Another Take: DCF Sends a Very Different Signal

While the analyst narrative sees fair value at $81.25 and calls that undervalued, the Simply Wall St DCF model points the other way. In this view, Ultra Clean at $63.16 is trading well above an estimated future cash flow value of about $0.23. This raises a sharp question about how much of UCT 3.0 and AI demand is already priced in.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Ultra Clean Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 59 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With such mixed signals across valuation models, it makes sense to check the underlying data yourself and decide how comfortable you are with the current risk reward trade off. To see both sides of the story in one place, take a closer look at the 2 key rewards and 1 important warning sign

Ready for more investment ideas?

If Ultra Clean has caught your eye, do not stop here. Broaden your watchlist now so you are not relying on a single story.

- Target quality at a sensible price by scanning companies that look mispriced using the 59 high quality undervalued stocks.

- Prioritise resilience by filtering for businesses with stronger finances through the solid balance sheet and fundamentals stocks screener (40 results).

- Hunt for future standouts before the crowd pays attention with the screener containing 25 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com