- In recent weeks, Crescent Energy’s position as a top 10 independent U.S. oil and gas producer has been reinforced by its multi–billion‑dollar Vital Energy acquisition and stronger investor attention amid heightened Middle East tensions that have lifted crude prices and earnings expectations across the sector.

- The combination of a larger Permian-focused asset base, rising free cash flow, and an expanding royalties business is now reshaping how Crescent Energy is grouped and compared within the U.S. energy universe.

- Next, we’ll examine how heightened Middle East tensions and Crescent’s expanded Permian footprint could influence its existing investment narrative.

Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

Crescent Energy Investment Narrative Recap

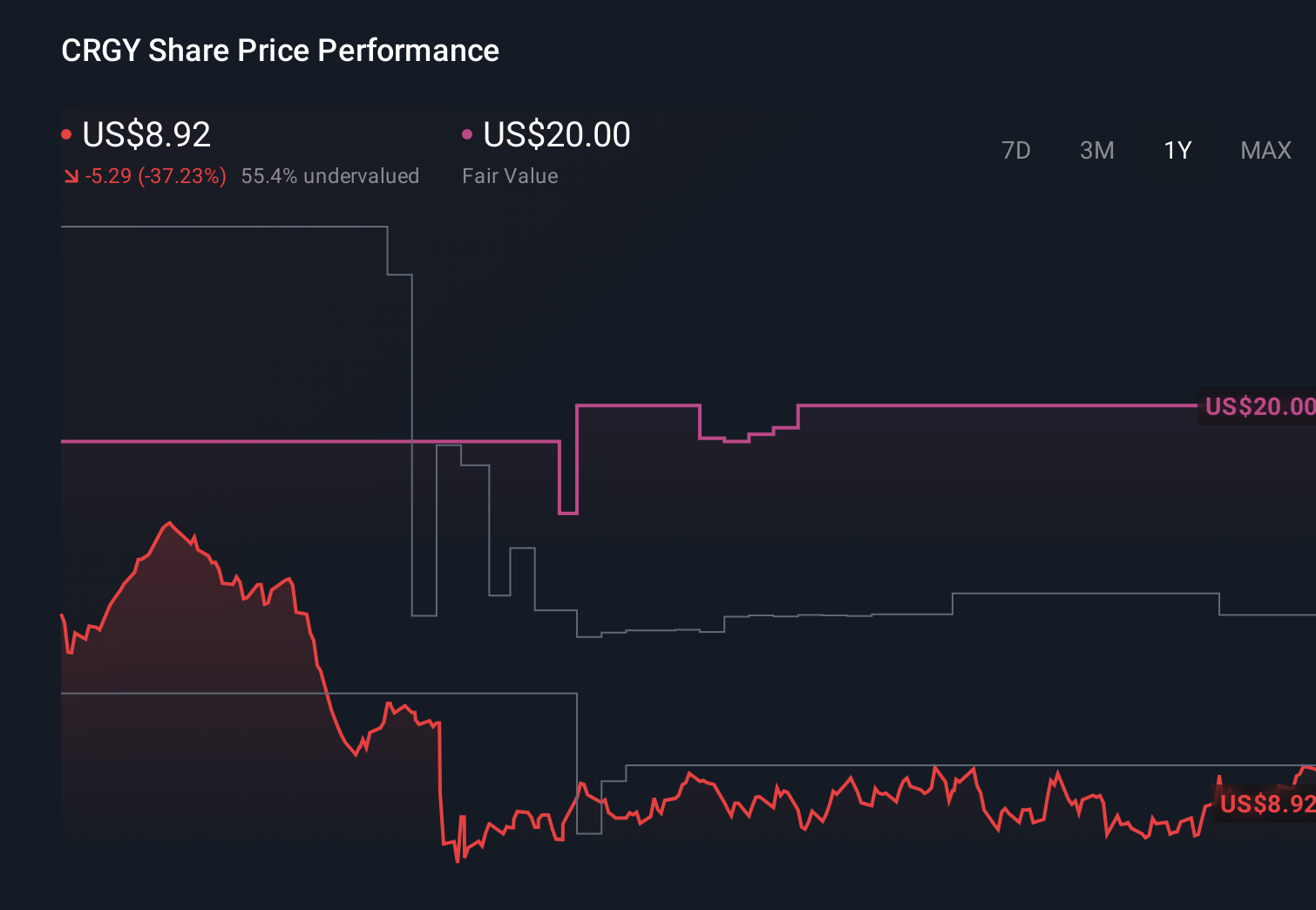

To own Crescent Energy, you have to believe its bigger Permian footprint and cash generation can outweigh the integration, leverage and commodity risks that come with rapid expansion. The latest spike in crude tied to Middle East tensions may reinforce near term earnings sensitivity to prices, but it does not fundamentally change the key near term catalyst, which is how effectively Crescent integrates Vital Energy and manages its higher debt load.

Against that backdrop, KeyBanc’s recent price target increase to US$19, following the US$3.10 billion Vital Energy acquisition and three straight EPS beats, is particularly relevant. It highlights how some analysts view Crescent’s enlarged scale and production guidance of 320,000 to 335,000 BOE per day in 2026 as central to the story, while the share buybacks and 4 percent dividend yield frame how management is choosing to return capital alongside that growth.

Yet, despite this stronger positioning, investors should still watch how Crescent’s acquisition driven model could amplify the impact of any prolonged downturn in oil prices and...

Read the full narrative on Crescent Energy (it's free!)

Crescent Energy's narrative projects $5.2 billion revenue and $672.6 million earnings by 2028.

Uncover how Crescent Energy's forecasts yield a $13.07 fair value, a 3% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts paint a far more cautious picture, assuming revenue of about US$4.5 billion and earnings near US$318 million by 2029, which sits in sharp contrast to more optimistic views on Crescent’s acquisition driven growth and could shift again as markets reassess today’s geopolitically charged oil backdrop.

Explore 4 other fair value estimates on Crescent Energy - why the stock might be worth just $13.07!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Crescent Energy research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Crescent Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Crescent Energy's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

- Find 59 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com