- Conagra Brands, Inc. recently reported mixed third‑quarter fiscal 2026 results, with net sales of US$2,787.8 million down from US$2,841.0 million a year earlier, but net income rising to US$199.8 million from US$145.1 million, while narrowing its fiscal 2026 guidance to organic net sales change near the midpoint of its 1% decline to 1% range versus 2025.

- Alongside these results, the company maintained its quarterly dividend at US$0.35 per share and highlighted renewed organic growth in its frozen and snacks businesses, even as higher input costs, a lower contribution from the Ardent Mills joint venture, and an anticipated 7% inflation rate on cost of goods sold weigh on margins and full‑year earnings expectations.

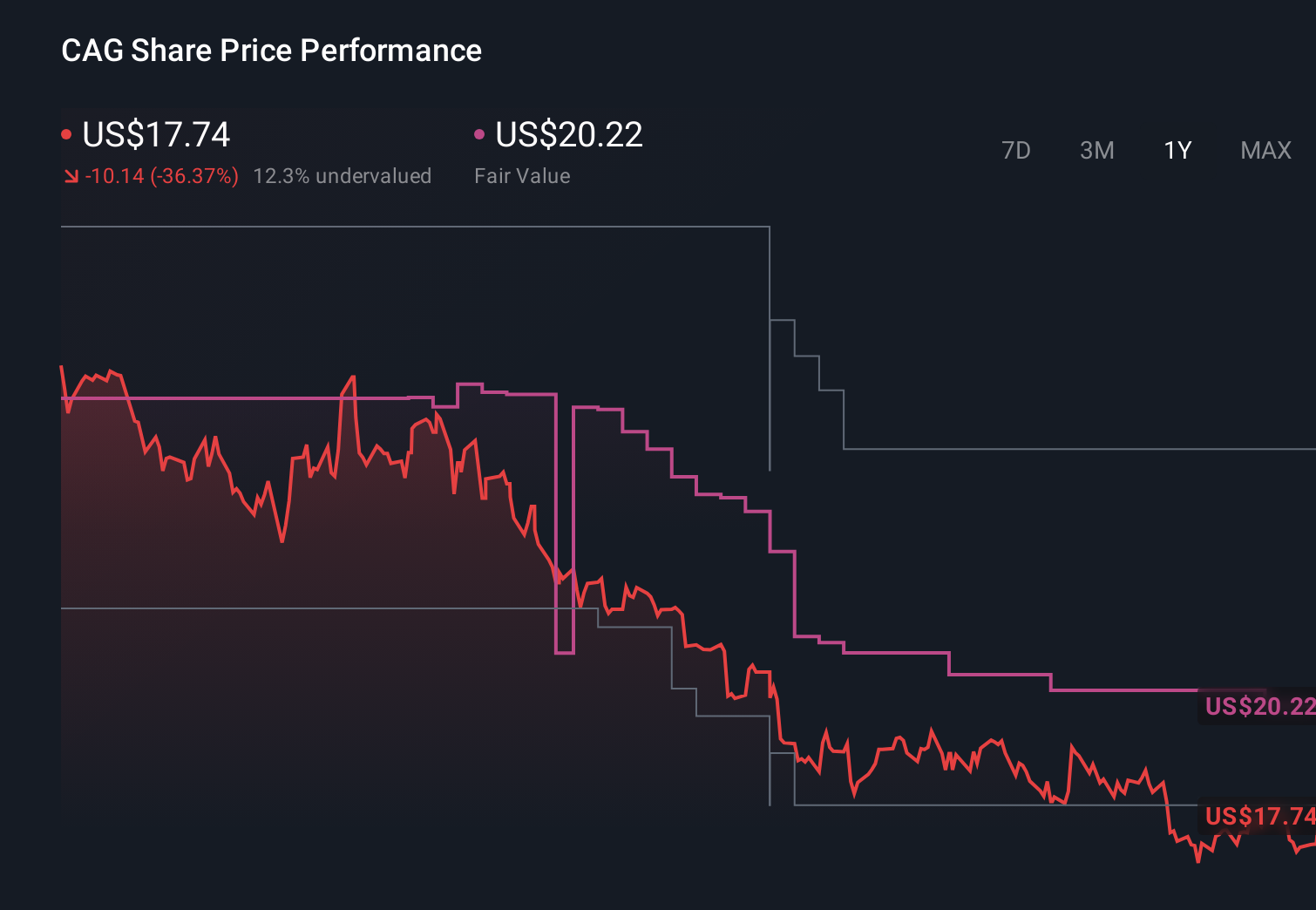

- With Conagra now expecting roughly flat organic sales and lower adjusted earnings for 2026, we’ll assess how this guidance reset and margin pressure affect its pre‑existing investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 21 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Conagra Brands Investment Narrative Recap

To own Conagra Brands today, you need to believe its frozen and snacks momentum and cash generation can offset pressure from inflation, soft volumes, and a still‑unprofitable year to date. The key short term catalyst is whether that renewed organic growth in core categories can flow through to margins despite an anticipated 7% cost of goods inflation. The biggest current risk is that this margin squeeze, alongside a weaker Ardent Mills contribution, keeps earnings under strain even as sales stabilize.

The most relevant recent move is Conagra’s decision to narrow fiscal 2026 guidance to roughly flat organic net sales and lower adjusted earnings of about US$1.70 per share. This reset effectively lowers the earnings bar, but it also sharpens the focus on execution in frozen and snacks, free cash flow conversion near 105%, and debt reduction as potential offsets to cost inflation and soft demand. How well the company performs against this tighter guide will shape sentiment around the next leg for the stock.

Yet behind the renewed frozen and snacks growth, investors should be aware of the company’s low Altman Z‑Score and what it could signal about...

Read the full narrative on Conagra Brands (it's free!)

Conagra Brands' narrative projects $11.4 billion revenue and $905.9 million earnings by 2028. This implies a 0.5% yearly revenue decline and an earnings decrease of about $294 million from $1.2 billion today.

Uncover how Conagra Brands' forecasts yield a $18.75 fair value, a 19% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming flat revenue at about US$11.2 billion and earnings of roughly US$1.1 billion by 2029, so you should recognize that this new guidance and margin pressure may push their already more pessimistic risk view even further, especially around whether portfolio shifts and supply chain improvements can really restore profitability as quickly as they projected.

Explore 10 other fair value estimates on Conagra Brands - why the stock might be worth 11% less than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Conagra Brands research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Conagra Brands research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Conagra Brands' overall financial health at a glance.

Curious About Other Options?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Find 59 companies with promising cash flow potential yet trading below their fair value.

- This technology could replace computers: discover 24 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com