Delek Logistics Partners (NYSE:DKL) recently put a new US$1.3b revolving credit facility in place, refinancing its prior agreement and extending potential maturity to 2031. This marks a shift that refocuses attention on the partnership's balance sheet.

See our latest analysis for Delek Logistics Partners.

The share price has eased in the short term, with a 7 day share price return of 5.35% and 30 day share price return of 6.05%, yet the 1 year total shareholder return of 39.85% and 5 year total shareholder return of 111.66% point to momentum that has been building over time as investors have reacted to both income and price gains. The new US$1.3b revolving credit facility, which refinances earlier borrowings and extends potential access to capital, adds a fresh datapoint for investors reassessing risk and balance sheet flexibility at the current US$50.28 share price.

If this refinancing has you thinking more broadly about income focused and infrastructure linked plays, it could be worth scanning the 28 power grid technology and infrastructure stocks

So with DKL trading around US$50.28, a value score of 4, and recent returns already strong, is the new US$1.3b facility a signal that the units are still mispriced, or is the market already pricing in future growth?

Most Popular Narrative: 2.6% Overvalued

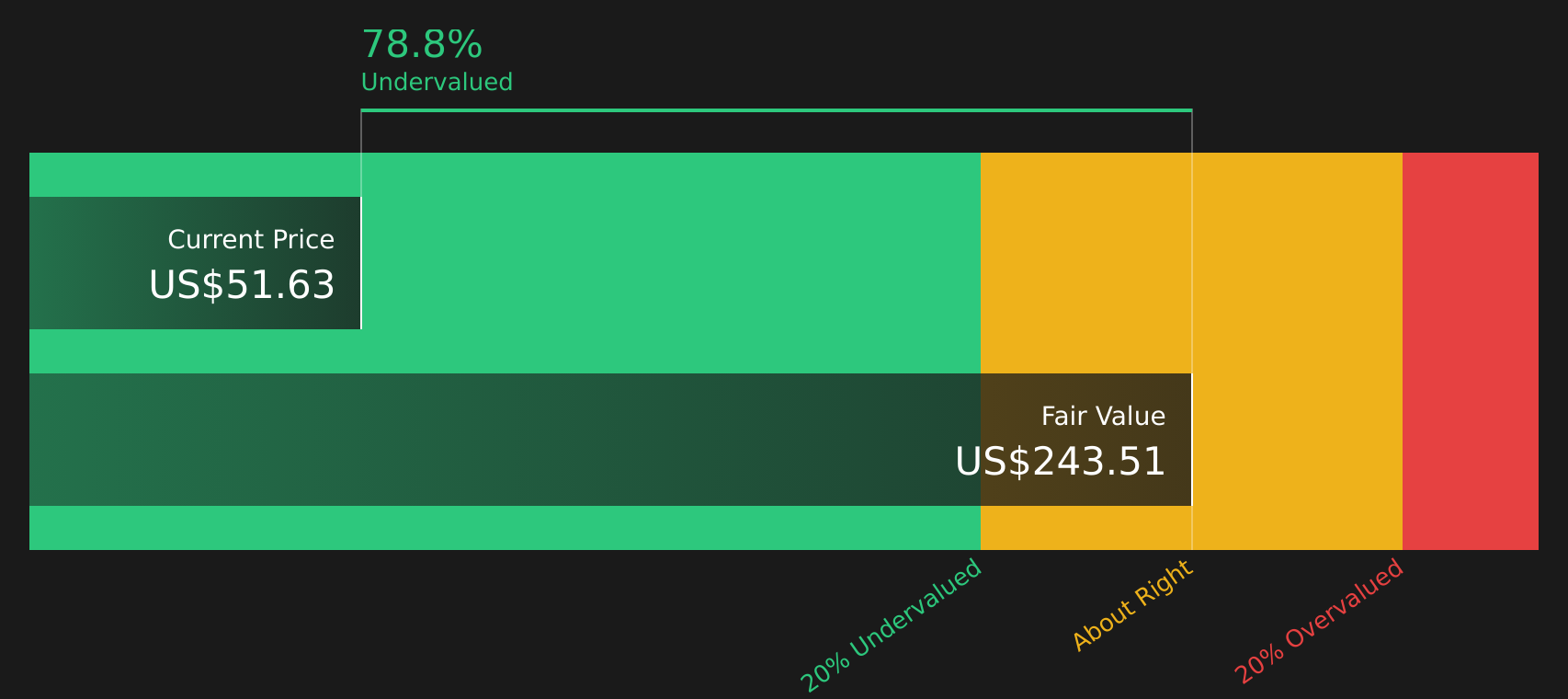

With the units at $50.28 against a narrative fair value of $49.00, analysts see only a small valuation gap, putting the refinancing into a tight pricing context.

The full commissioning and expected ramp to capacity of the new Libby 2 gas plant in the Delaware Basin, along with associated investments (amine unit and AGI wells), positions Delek Logistics to capitalize on rising energy demand and stable domestic energy infrastructure needs, likely boosting gathering and processing volumes, EBITDA, and revenue growth.

Curious what kind of revenue lift, margin profile, and future earnings multiple are baked into that fair value, and how far out the heavy lifting really sits?

Result: Fair Value of $49 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that story depends heavily on Libby 2 ramping as planned and on customer volumes holding up in the Permian, both areas where delays or contract changes could create risks.

Find out about the key risks to this Delek Logistics Partners narrative.

Another Angle on Value

The narrative fair value of $49 suggests a small 2.6% premium at $50.28. However, the SWS DCF model presents a very different picture, with DKL trading at a steep discount to its estimated future cash flow value of $380.76. Which story do you think better fits a leveraged midstream partnership?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

The mix of optimism and concern in this story is hard to ignore, so it makes sense to review the underlying numbers yourself and decide quickly where you stand based on the 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If DKL has sharpened your focus, do not stop here. Use the Simply Wall Street Screener to uncover fresh, data driven ideas that fit your style.

- Target resilient balance sheets and solid fundamentals by running the solid balance sheet and fundamentals stocks screener (40 results) that filters for companies with financial strength at the core.

- Pursue quality at a price that suits you with the 59 high quality undervalued stocks highlighting companies where fundamentals and current pricing look out of sync.

- Prioritise income potential with the 13 dividend fortresses focused on businesses offering higher yielding dividends with an emphasis on stability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com