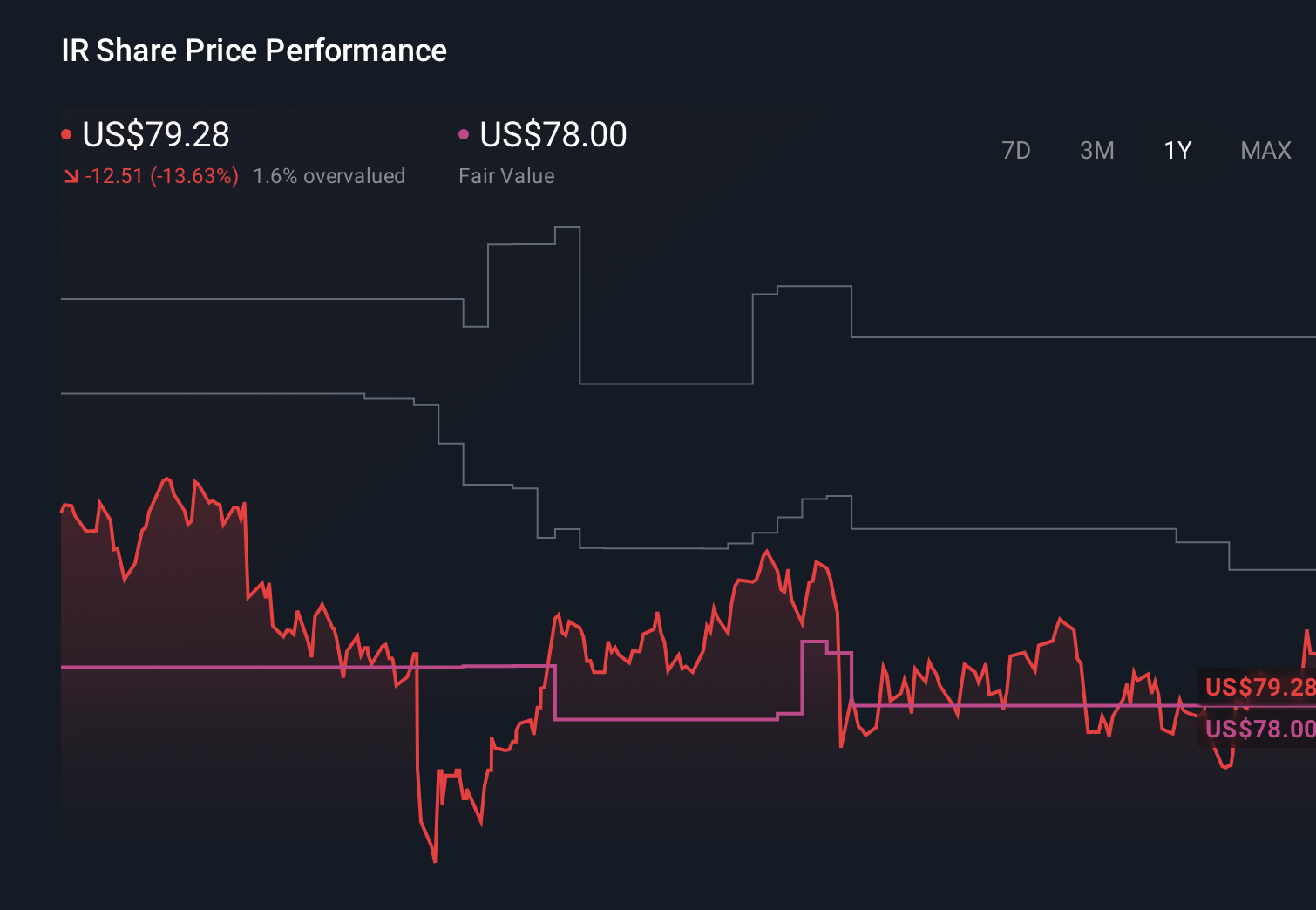

- In the past quarter, Ingersoll Rand reported revenues of US$2.09 billion, a 10.1% year-on-year increase that exceeded analyst expectations by 2.6%, alongside stronger earnings and free cash flow in what management called a complex global backdrop.

- At the same time, insider sentiment turned more cautious with increased insider selling, even as Barclays reaffirmed its positive view on the company’s operational performance.

- We’ll now examine how this stronger-than-expected revenue performance may influence Ingersoll Rand’s investment narrative and longer-term earnings assumptions.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 21 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Ingersoll Rand Investment Narrative Recap

To own Ingersoll Rand, you need to believe in its ability to turn energy efficiency, aftermarket services, and disciplined M&A into durable earnings, despite cyclical industrial spending and geopolitical noise. The latest quarter’s better than expected US$2.09 billion revenue supports that thesis, but the 17.3% share price drop and heavier insider selling refocus attention on valuation risk and the possibility that weaker organic orders or macro shocks could pressure short term expectations. Overall, the news does not materially change the core long term story.

Against this backdrop, the ongoing share buyback program stands out as especially relevant. In Q4 2025, Ingersoll Rand repurchased about US$314.7 million of stock, bringing total spend under the current authorization to roughly US$1.76 billion. For investors watching a high earnings multiple and recent underperformance versus the Machinery sector, this capital return policy interacts directly with the catalysts around recurring revenue growth and M&A, and with the risk that acquisition missteps or softer orders undermine future returns.

Yet beneath the strong quarter and buybacks, the growing tension between premium valuation and uneven earnings trends is something investors should be aware of...

Read the full narrative on Ingersoll Rand (it's free!)

Ingersoll Rand's narrative projects $8.8 billion revenue and $1.4 billion earnings by 2029. This requires 4.7% yearly revenue growth and about an $818.6 million earnings increase from $581.4 million today.

Uncover how Ingersoll Rand's forecasts yield a $101.93 fair value, a 31% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts took a more cautious line, assuming revenue would grow only about 2.5% a year and still reach roughly US$7.8 billion by 2028. If you are weighing that against the recent revenue beat and ongoing M&A driven expansion, it highlights how differently people can read the same story and why it is worth comparing several viewpoints before you decide what feels reasonable for you.

Explore 3 other fair value estimates on Ingersoll Rand - why the stock might be worth as much as 31% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Ingersoll Rand research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Ingersoll Rand research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ingersoll Rand's overall financial health at a glance.

Contemplating Other Strategies?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

- Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- AI is about to change healthcare. These 36 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com