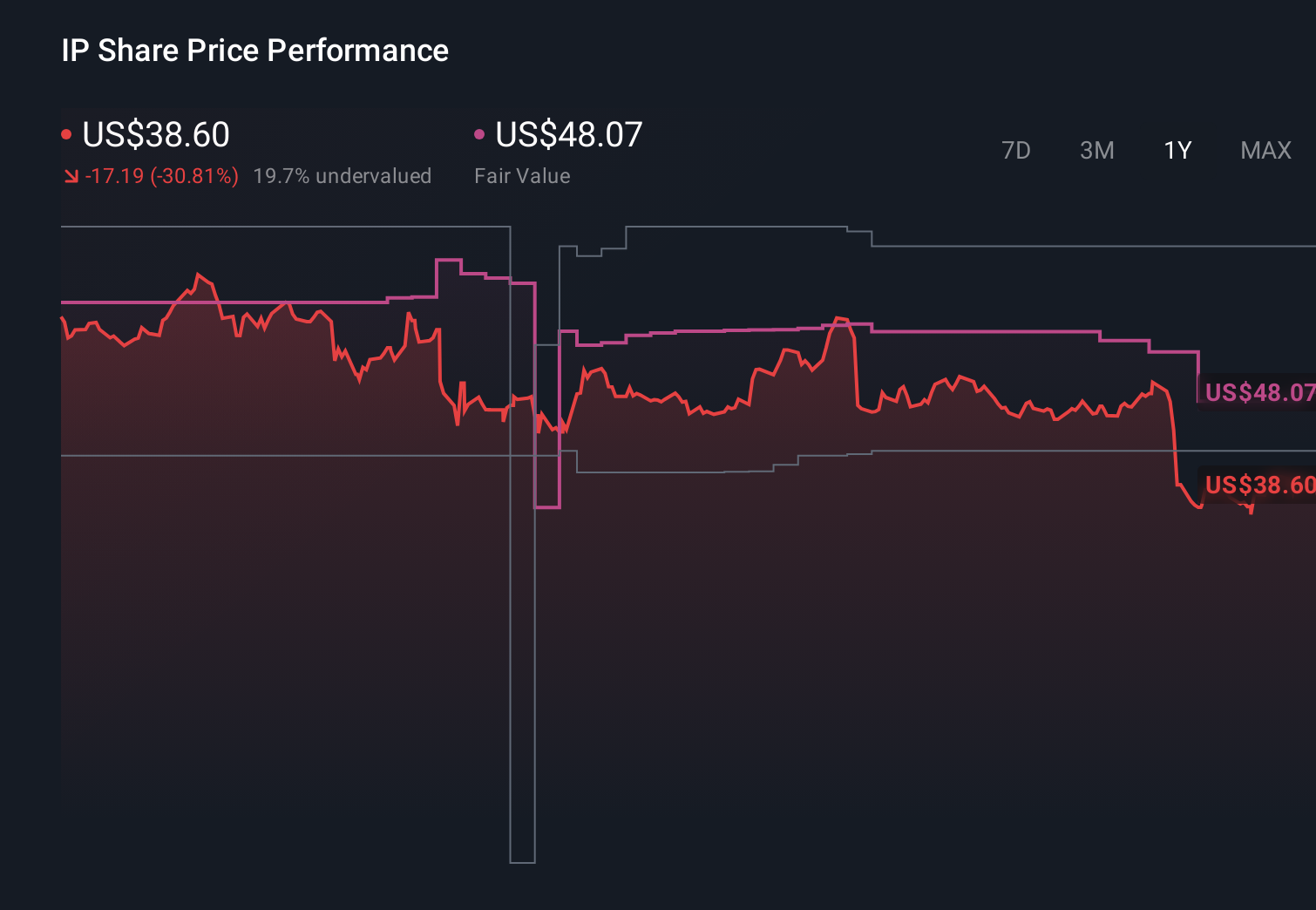

- In recent months, International Paper has faced weaker demand, higher costs, and heavy restructuring charges, alongside analyst concerns over its softer results and execution risks.

- Together with falling free cash flow margins and declining returns on invested capital, these pressures are prompting investors to question the company’s longer-term profit potential and growth options.

- We’ll now examine how this combination of cost headwinds and muted packaging demand could reshape International Paper’s investment narrative.

Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

International Paper Investment Narrative Recap

To own International Paper today, you need to believe its push into fiber-based packaging and operational improvements can offset cyclical softness, higher costs, and recent restructuring losses. The key near term catalyst is whether management can stabilize earnings despite analyst estimate cuts and cost headwinds flagged by J.P. Morgan’s Negative Catalyst Watch. The biggest current risk is that persistent mill and restructuring issues keep margins and free cash flow under pressure. The latest news reinforces, rather than changes, that risk profile.

The most relevant recent development here is J.P. Morgan’s decision to put the stock on Negative Catalyst Watch, citing steeper cost headwinds than peers and trimming EBITDA estimates. This sits uncomfortably alongside International Paper’s already weaker free cash flow margins and falling ROIC, and raises fresh questions about how quickly its cost out and packaging growth projects, such as the new US$225,000,000 Mississippi facility, can translate into better profitability.

Yet beneath the long term packaging story, investors should be aware that persistent mill reliability and cost pressures could still...

Read the full narrative on International Paper (it's free!)

International Paper's narrative projects $26.3 billion revenue and $1.7 billion earnings by 2029. This requires 3.6% yearly revenue growth and a $4.5 billion earnings increase from -$2.8 billion today.

Uncover how International Paper's forecasts yield a $46.47 fair value, a 34% upside to its current price.

Exploring Other Perspectives

Before this setback, the most optimistic analysts were assuming revenue could reach about US$30.8 billion and earnings US$2.9 billion by 2028, a far rosier view than the current cost headwinds and mill risks imply, reminding you that reasonable investors can see the same stock very differently and that these upbeat narratives may need to be revisited as new data arrives.

Explore 3 other fair value estimates on International Paper - why the stock might be worth just $46.47!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your International Paper research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free International Paper research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate International Paper's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- AI is about to change healthcare. These 36 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 21 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Find 58 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com