- VinFast recently launched the VF 9, a fully electric three-row SUV offering up to 518 kilometres of range, a spacious family-oriented interior, and an all-in starting price of C$77,308, backed by 10-year warranties for both the vehicle and battery.

- By combining luxury features such as ventilated, massaging captain’s chairs with extensive cargo flexibility and app-enabled charging access, the VF 9 positions VinFast to appeal simultaneously to family buyers and premium EV customers.

- We’ll now explore how the VF 9’s long-range, three-row format and extensive warranty coverage could influence VinFast’s broader investment narrative.

AI is about to change healthcare. These 36 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

VinFast Auto Investment Narrative Recap

To own VinFast, you have to believe it can turn rapid EV expansion into sustainable, higher quality revenue despite heavy losses and liquidity pressure. The VF 9 launch in Canada modestly supports the near term delivery and brand recognition catalyst, but it does not meaningfully change the immediate risks tied to high cash burn, negative equity, and reliance on Vingroup funding.

Among recent developments, the shift to a dealer based distribution model in North America and Europe is especially relevant here, because the VF 9’s appeal to family and premium buyers depends on consistent sales, service, and charging support. If dealers can convert VF 9 interest into actual deliveries while keeping VinFast’s own fixed costs lower, that could incrementally support the volume and margin improvement story around new products like this SUV.

Yet behind the VF 9’s appeal, investors should really be paying attention to the company’s ongoing cash burn and reliance on external funding...

Read the full narrative on VinFast Auto (it's free!)

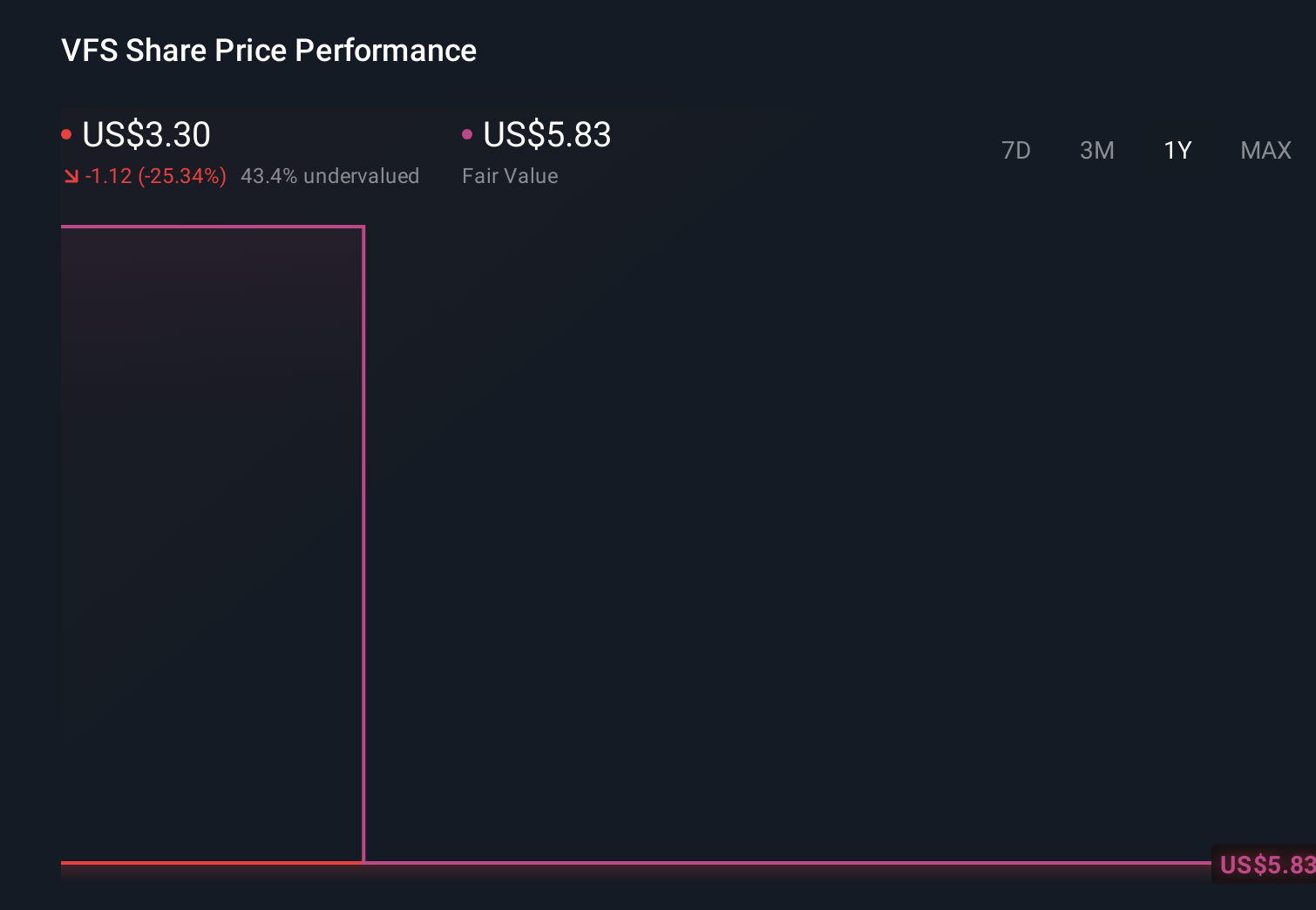

VinFast Auto’s narrative projects ₫239,006.9 billion in revenue and ₫6,414.4 billion in earnings by 2029. This requires 38.3% yearly revenue growth and an earnings increase of about ₫103,456.3 billion from -₫97,041.9 billion today.

Uncover how VinFast Auto's forecasts yield a $6.38 fair value, a 40% upside to its current price.

Exploring Other Perspectives

While consensus sees fast revenue growth, the most bearish analysts expected about 47 percent annual revenue growth and still no profits by 2029, underscoring how sharply opinions differ and how launches like the VF 9 could eventually shift these more pessimistic views.

Explore 5 other fair value estimates on VinFast Auto - why the stock might be worth less than half the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your VinFast Auto research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free VinFast Auto research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate VinFast Auto's overall financial health at a glance.

Ready For A Different Approach?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

- Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com