The United States market has shown strong performance recently, climbing 3.5% in the last week and 31% over the past year, with earnings projected to grow by 16% annually in the coming years. In such a dynamic environment, identifying stocks that are potentially undervalued can be crucial for investors looking to capitalize on growth opportunities across various regions.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Enovis | NA | 0.6x | 47.21% | ★★★★★★ |

| Financial Institutions | 8.6x | 2.7x | 44.58% | ★★★★★☆ |

| AVITA Medical | NA | 1.6x | 36.77% | ★★★★★☆ |

| Tennant | 28.7x | 1.0x | 47.49% | ★★★★☆☆ |

| 1st Source | 11.0x | 4.1x | 48.03% | ★★★★☆☆ |

| Franklin Financial Services | 10.9x | 2.7x | 0.60% | ★★★☆☆☆ |

| New Peoples Bankshares | 9.4x | 2.2x | 41.83% | ★★★☆☆☆ |

| Bank of the James Financial Group | 10.6x | 2.0x | 46.94% | ★★★☆☆☆ |

| CEVA | NA | 5.0x | -17.07% | ★★★☆☆☆ |

| Douglas Emmett | 105.2x | 1.6x | 44.35% | ★★★☆☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

CEVA (CEVA)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: CEVA is a technology company specializing in licensing intellectual property, with a focus on signal processing platforms and artificial intelligence processors, and has a market cap of approximately $0.82 billion.

Operations: The company's primary revenue stream is derived from licensing intellectual property, with recent quarterly revenue reaching $109.60 million. The gross profit margin has shown fluctuations, recently recorded at 87.08%. Operating expenses are significant, with research and development being a major component, accompanied by sales and marketing costs. The net income margin has experienced variability over time, reflecting the impact of both operating and non-operating expenses on profitability.

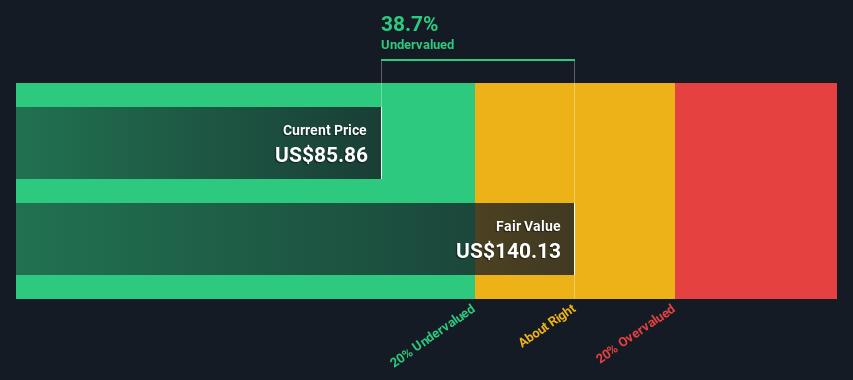

PE: -51.2x

CEVA's recent product innovations, including the Ceva-Waves UWB IP and PentaG-NTN modem, position it well in the growing wireless and satellite markets. Despite reporting a net loss of US$1.1 million for Q4 2025, revenue increased to US$31.29 million from the previous year. Insider confidence is evident with Amir Panush purchasing 5,100 shares for US$100,470 recently. The company's strategic focus on next-gen connectivity solutions and insider activity suggest potential for future growth in these expanding sectors.

- Click here and access our complete valuation analysis report to understand the dynamics of CEVA.

Gain insights into CEVA's past trends and performance with our Past report.

ICF International (ICFI)

Simply Wall St Value Rating: ★★★★★☆

Overview: ICF International provides professional services to a broad array of clients, with operations focused on delivering strategic consulting and technology solutions, and has a market capitalization of approximately $2.16 billion.

Operations: ICF International's primary revenue stream is derived from professional services, generating $1.87 billion. The company's cost of goods sold (COGS) for the same period was $1.18 billion, resulting in a gross profit margin of 37.16%. Operating expenses include significant general and administrative costs amounting to $492.40 million, impacting its net income margin which stands at 4.89%.

PE: 13.4x

ICF International is navigating its small cap space with strategic acquisitions and a focus on organic growth, as highlighted by their CFO. Despite a dip in recent earnings, with Q4 2025 sales at US$443.67 million compared to last year's US$496.32 million, the company remains proactive through share repurchases totaling 1.19% of shares from October to December 2025 for US$17.78 million. Their involvement in significant contracts like Florida's management services and Pennsylvania's system modernization underscores potential for future growth amidst current financial challenges.

- Navigate through the intricacies of ICF International with our comprehensive valuation report here.

Examine ICF International's past performance report to understand how it has performed in the past.

AH REALTY TRUST (AHRT)

Simply Wall St Value Rating: ★★★★★☆

Overview: AH Realty Trust operates in the real estate sector, focusing on office, retail, and multifamily real estate properties as well as real estate financing, with a market capitalization of $1.83 billion.

Operations: AH Realty Trust generates revenue primarily from office and retail real estate, with additional contributions from multifamily real estate and real estate financing. The company's gross profit margin has shown variability, peaking at 48.25% in Q4 2021 before declining to 26.13% in Q2 2024. Operating expenses are significant, including general and administrative costs, which have increased over time reaching $23.23 million in Q2 2025.

PE: -41.3x

AH Realty Trust, a small cap stock in the U.S., recently filed a $300 million shelf registration, indicating potential capital raising. Despite being dropped from multiple S&P indices in March 2026, the company continues to expand its retail footprint with new leases at key mixed-use destinations like Southern Post and Town Center of Virginia Beach. However, financial challenges persist as earnings are projected to decline by 1.7% annually over the next three years.

- Delve into the full analysis valuation report here for a deeper understanding of AH REALTY TRUST.

Review our historical performance report to gain insights into AH REALTY TRUST's's past performance.

Where To Now?

- Access the full spectrum of 57 Undervalued US Small Caps With Insider Buying by clicking on this link.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com