Virtu Financial (VIRT) is back on investor radars after a string of earnings beats, higher analyst estimates, and a favorable Zacks Rank, all coinciding with renewed interest in its valuation versus sector peers.

See our latest analysis for Virtu Financial.

Those strong earnings surprises and improving sentiment have come alongside a sharp share price move. The stock is now at $46.22 after a 39.34% 3 month share price return and a 179.25% 3 year total shareholder return. This suggests momentum has been building as investors reassess the risk reward trade off.

If Virtu’s recent run has you thinking about other opportunities in the market, this can be a good moment to scan for potential winners through the 20 top founder-led companies

With shares near $46, a value score of 5, and an estimated intrinsic value implying a roughly 49% discount, the key question now is whether Virtu still trades below its fundamentals or if the market is already pricing in future growth.

Most Popular Narrative: 332% Overvalued

According to a widely followed narrative by DailyInvestors, Virtu Financial’s fair value of $10.71 sits far below the recent $46.22 share price, creating a sharp gap between market price and that view of worth.

VIRT "stock ticker name" or better known as Vertiv Holdings. Is one of them companies, that is continually making Global Headlines. Any company let alone with a Positive Cash Flow of 302%+, is one that should be talked about. VIRT is a AI Financial Service Company. This little firm has integrated AI and algorithm trading into their system. VIRT is currently rated a Strong Buy, and honestly is at a Perfect Price for Long Term Investments. Why is this? Today after reporting a successful Earnings Report. Their shares plummeted after Bulls sold for the short Profit. This means now, it is at its new lowest bottom. This is because their report, posted a positive outcome and results showing that now it is definitely a way undervalued company. In just this year, they have climbed over 100%. Then add in them constantly making headlines, that add the votality for major runs. We are not getting paid for any of these articles. We are freelance, but when we see a good company that is honest and growing. Well make our report. You heard this from The Daily Investors.

The fair value hinges on a specific view of cash flow strength, profit margins and a future earnings multiple that sits well below today’s market pricing. Curious which assumptions do the heavy lifting in that $10.71 estimate, and how they try to reconcile rapid recent returns with a much lower valuation anchor.

Result: Fair Value of $10.71 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this view could be challenged if Virtu’s revenue contraction of 10.19% continues, or if margins tied to its market making and execution services compress.

Find out about the key risks to this Virtu Financial narrative.

Another View: Earnings Multiple Sends a Different Signal

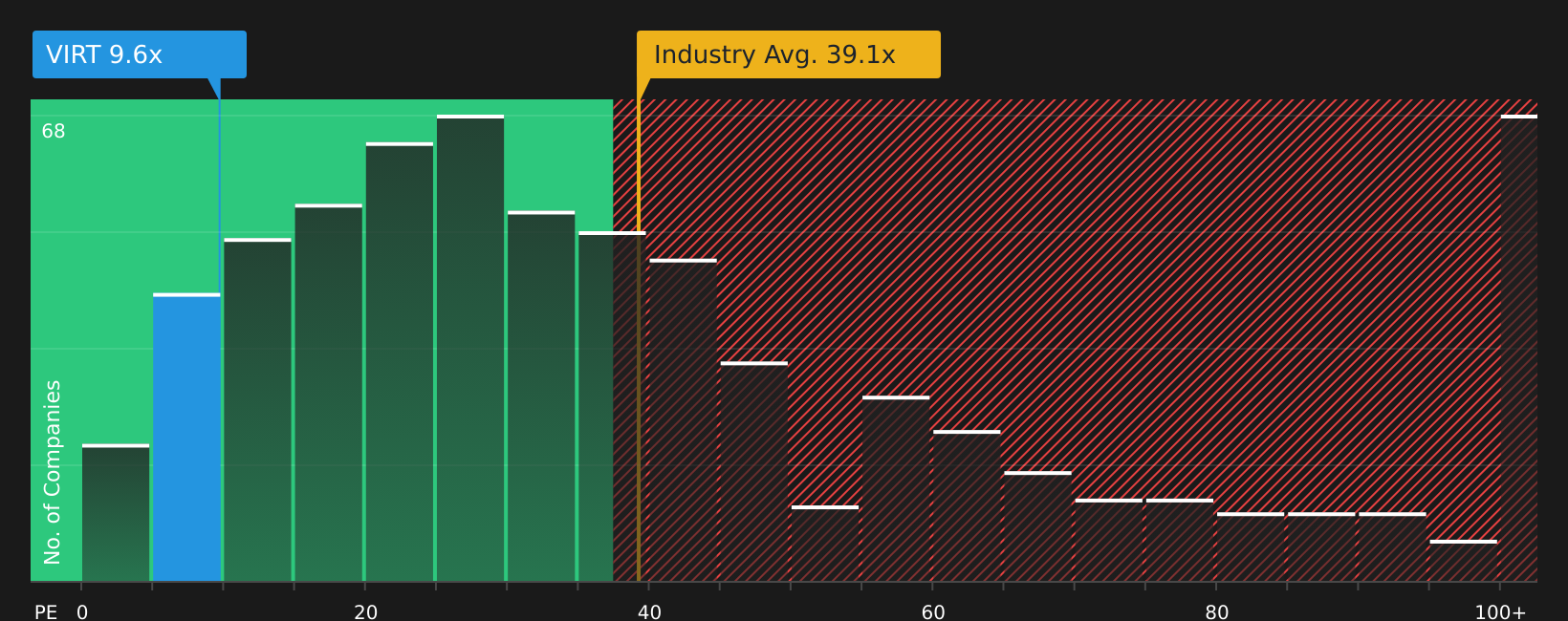

DailyInvestors’ $10.71 fair value suggests Virtu is 332% overvalued, but our preferred P/E check points the other way. At 9.1x earnings versus a fair ratio of 14.4x, and well below the 18.4x peer average and 36.1x industry average, the market could be underpricing those earnings. The question is which story you trust when you look at your own risk tolerance.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this mix of optimism and concern feels conflicting, treat it as your cue to check the numbers yourself and weigh both sides of the story with the 5 key rewards and 1 important warning sign

Looking for more investment ideas?

If Virtu has sharpened your focus, do not stop here. Broaden your watchlist now so you are not late to the next opportunity Simply Wall St surfaces.

- Target income potential by reviewing companies screened as higher yield opportunities through the 13 dividend fortresses.

- Zero in on quality at a discount by scanning companies highlighted in the 58 high quality undervalued stocks.

- Prioritise capital preservation first by checking companies flagged as having sturdier profiles in the 67 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com