The market in the United States has shown a notable uptick, rising 3.5% over the last week and achieving a 31% increase over the past year, with earnings projected to grow by 16% annually. In such an environment, dividend stocks that offer consistent payouts and potential for growth can be appealing options for investors seeking to benefit from both income and capital appreciation.

Top 10 Dividend Stocks In The United States

| Name | Dividend Yield | Dividend Rating |

| Provident Financial Services (PFS) | 4.51% | ★★★★★★ |

| Peoples Bancorp (PEBO) | 4.90% | ★★★★★★ |

| OTC Markets Group (OTCM) | 5.46% | ★★★★★★ |

| Omega Healthcare Investors (OHI) | 5.96% | ★★★★★★ |

| First Interstate BancSystem (FIBK) | 5.62% | ★★★★★★ |

| First Community Bankshares (FCBC) | 5.34% | ★★★★★★ |

| Farmers National Banc (FMNB) | 5.07% | ★★★★★★ |

| Ennis (EBF) | 4.61% | ★★★★★★ |

| Dillard's (DDS) | 5.45% | ★★★★★★ |

| Columbia Banking System (COLB) | 5.34% | ★★★★★★ |

Click here to see the full list of 114 stocks from our Top US Dividend Stocks screener.

Here we highlight a subset of our preferred stocks from the screener.

OneSpan (OSPN)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: OneSpan Inc. offers digital security, authentication, identity, electronic signature, and digital workflow solutions across various regions including the Americas, Europe, the Middle East, Africa, and the Asia Pacific with a market cap of approximately $400.52 million.

Operations: OneSpan Inc.'s revenue is primarily derived from its Cybersecurity segment, which generated $177.69 million, and its Digital Agreements segment, contributing $65.49 million.

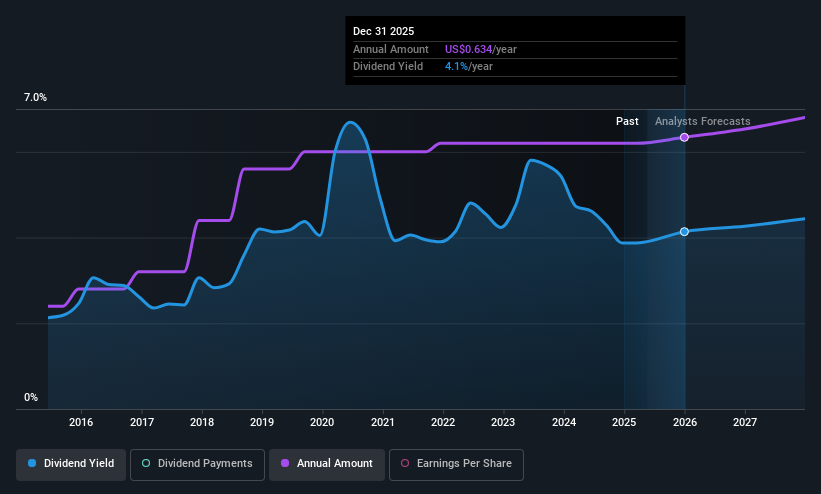

Dividend Yield: 4.9%

OneSpan Inc. recently increased its quarterly dividend to US$0.13 per share, reflecting an 8% annualized rise, while maintaining a low payout ratio of 25.7%, indicating dividends are well-covered by earnings and cash flows. Despite being new to dividends, OneSpan's yield of 4.86% places it in the top quartile among US dividend payers. The company's strategic focus on M&A and digital integration solutions like the Workato partnership could support future growth but may impact near-term profitability.

- Delve into the full analysis dividend report here for a deeper understanding of OneSpan.

- The valuation report we've compiled suggests that OneSpan's current price could be quite moderate.

Huntington Bancshares (HBAN)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Huntington Bancshares Incorporated, with a market cap of $32.17 billion, operates as the bank holding company for The Huntington National Bank, offering commercial, consumer, and mortgage banking services.

Operations: Huntington Bancshares generates revenue through its Commercial Banking segment at $2.76 billion and Consumer & Regional Banking segment at $5.24 billion.

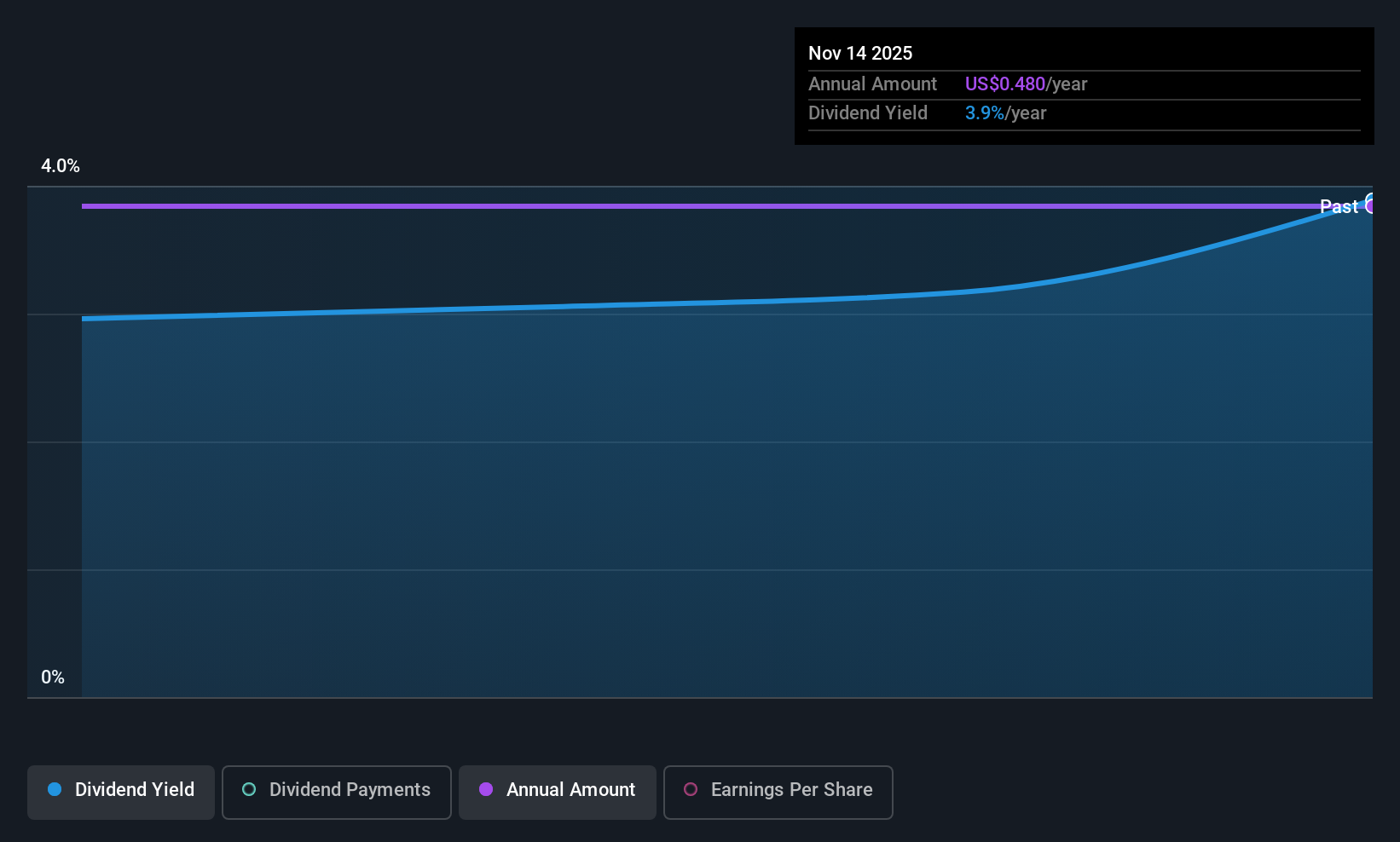

Dividend Yield: 3.9%

Huntington Bancshares offers a consistent dividend, recently reaffirming a quarterly cash dividend of US$0.155 per share. Its dividends are well-covered by earnings with a payout ratio of 43.9%, and future coverage is forecasted to improve to 37.1%. Despite trading below estimated fair value, the stock's yield of 3.93% is slightly lower than top-tier US dividend payers. Recent executive changes and strategic moves like fixed-income offerings may influence its financial stability and growth trajectory.

- Dive into the specifics of Huntington Bancshares here with our thorough dividend report.

- Our comprehensive valuation report raises the possibility that Huntington Bancshares is priced lower than what may be justified by its financials.

Copa Holdings (CPA)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Copa Holdings, S.A. operates as an airline providing passenger, cargo, and mail transportation services across North America, South America, Central America, and the Caribbean with a market cap of approximately $4.73 billion.

Operations: Copa Holdings generates its revenue primarily from air transportation, amounting to $3.62 billion.

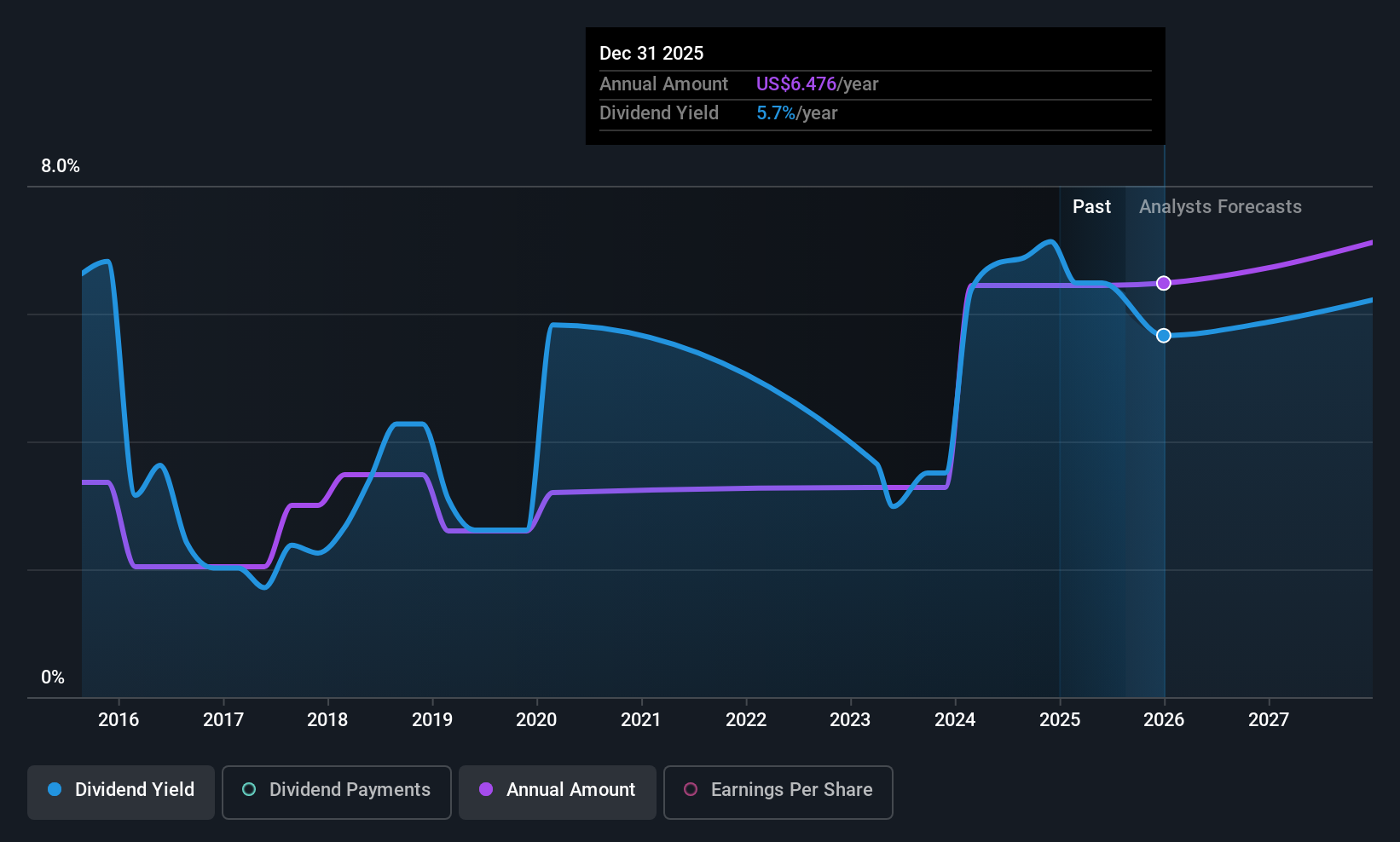

Dividend Yield: 6%

Copa Holdings' quarterly dividend of US$1.71 per share is among the top 25% in the US market, yet its sustainability is questionable due to a high cash payout ratio of 538.9%. Although dividends are well-covered by earnings with a 39.6% payout ratio, past volatility raises concerns about reliability. Recent earnings growth and trading at a good value compared to peers may appeal to investors despite dividend coverage issues from free cash flows.

- Click to explore a detailed breakdown of our findings in Copa Holdings' dividend report.

- The analysis detailed in our Copa Holdings valuation report hints at an deflated share price compared to its estimated value.

Turning Ideas Into Actions

- Take a closer look at our Top US Dividend Stocks list of 114 companies by clicking here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com