- In recent months, Ormat Technologies has outlined plans to add 149 MW of new capacity by the end of 2027, including 101 MW from geothermal projects, while committing US$180 million to build additional energy storage assets in the United States through 2028.

- This combination of geothermal expansion and sizable storage investment highlights Ormat’s effort to deepen its role in supplying grid-stable renewable power as adoption of clean energy accelerates.

- Next, we’ll explore how Ormat’s planned 149 MW capacity addition could reshape its investment narrative and future growth expectations.

The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Ormat Technologies Investment Narrative Recap

To own Ormat Technologies, you need to believe in its ability to turn long term geothermal and storage assets into steady, inflation resilient cash flows while managing heavy capital needs. The new 149 MW pipeline and US$180 million storage build are directionally consistent with this thesis, but do not materially change the near term picture where project execution and capital discipline remain the key catalyst, and balance sheet strain from ongoing capex is still the central risk.

The recent commissioning of the 80 MW / 320 MWh Shirk storage facility in California, under a 15 year resource adequacy agreement and supported by tax equity, feels closely linked to the latest growth plans. It shows how Ormat is already turning policy support and storage investment into contracted assets, which ties directly into the catalyst of credit enhanced returns from ITC monetization and longer dated offtake agreements, even as investors weigh the rising capex burden.

Yet, investors also need to be aware of how Ormat’s elevated capital spending and leverage could magnify the impact of any slowdown in project ramp up or funding access...

Read the full narrative on Ormat Technologies (it's free!)

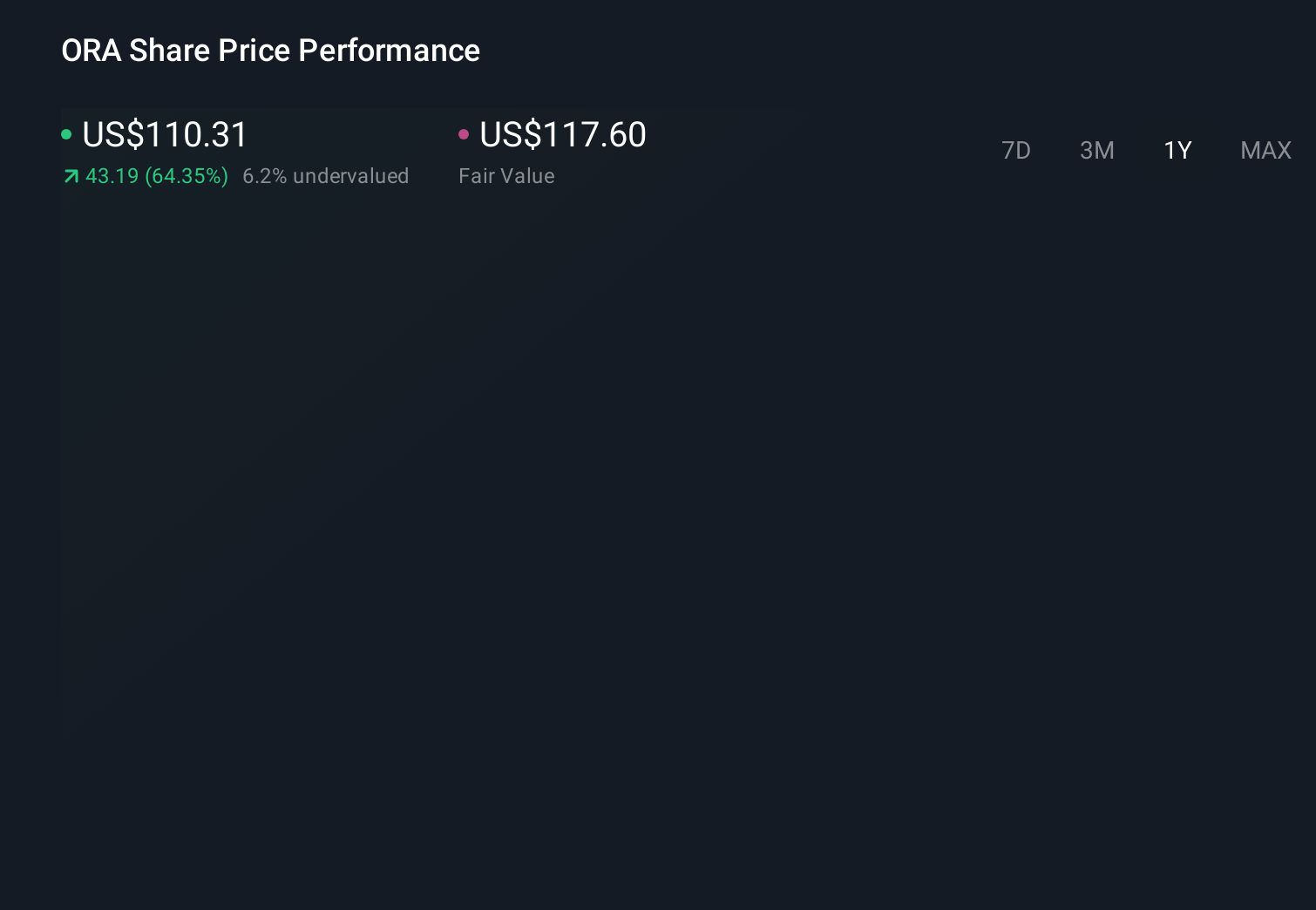

Ormat Technologies' narrative projects $1.3 billion revenue and $203.7 million earnings by 2029. This requires 8.6% yearly revenue growth and about an $80 million earnings increase from $123.9 million today.

Uncover how Ormat Technologies' forecasts yield a $127.27 fair value, a 15% upside to its current price.

Exploring Other Perspectives

Three Simply Wall St Community fair value estimates for Ormat span a very wide range, from about US$9 to roughly US$127 per share, showing how far apart views can be. Against this backdrop, the company’s sizeable upcoming capex and leverage profile could be seen very differently depending on how you weigh long term geothermal and storage growth against near term balance sheet risk, so it is worth comparing several viewpoints.

Explore 3 other fair value estimates on Ormat Technologies - why the stock might be worth as much as 15% more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Ormat Technologies research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Ormat Technologies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ormat Technologies' overall financial health at a glance.

Searching For A Fresh Perspective?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- AI is about to change healthcare. These 37 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Outshine the giants: these 21 early-stage AI stocks could fund your retirement.

- This technology could replace computers: discover 23 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com