Context for LSB Industries stock

LSB Industries (LXU) has drawn fresh attention after a strong year of share price performance, with total return over the past 12 months at 185% and market value around US$1.1b.

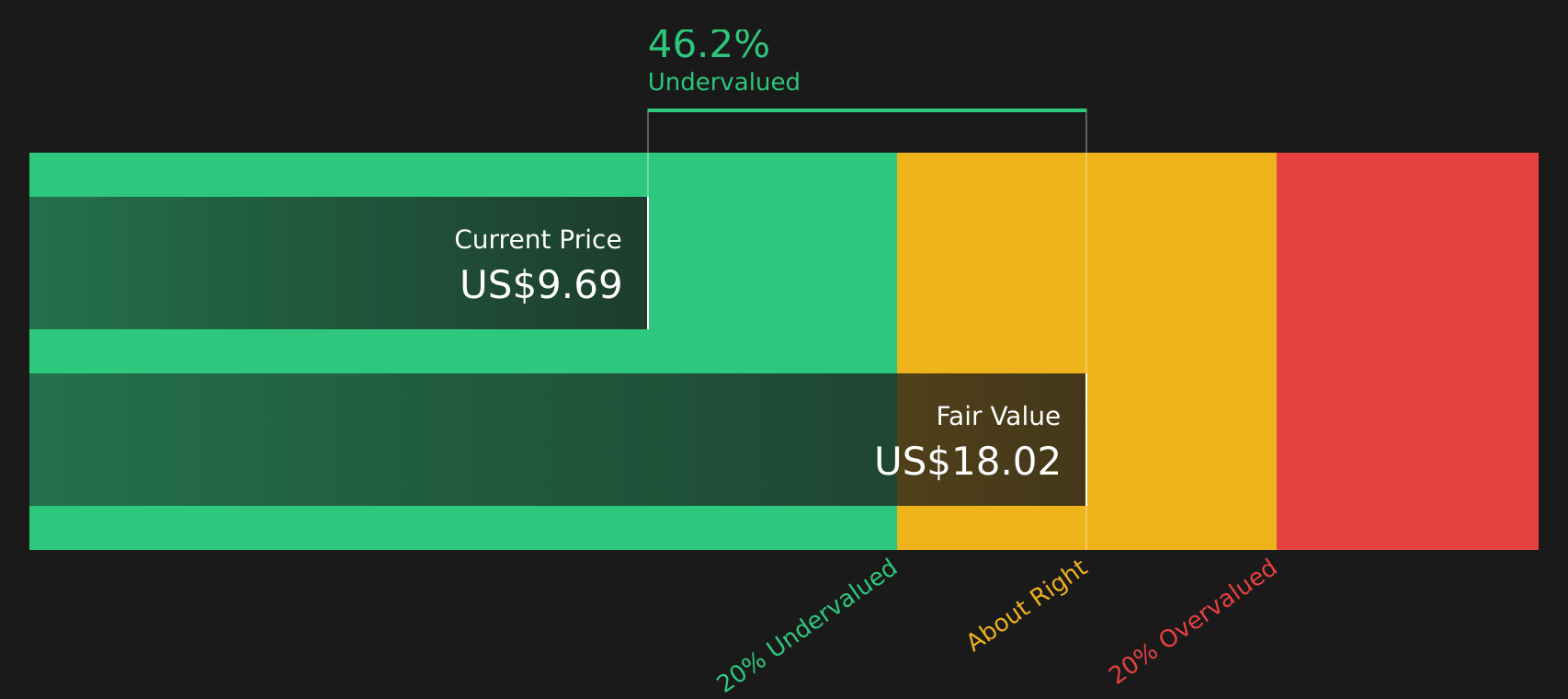

See our latest analysis for LSB Industries.

At a share price of US$15.00, LSB Industries has seen strong positive momentum over the past year, with a 68.35% 3 month share price return contributing to a 184.63% 1 year total shareholder return, even after a softer 7 day share price move.

If this kind of move has your attention, it could be a good moment to widen your search with the Simply Wall St screener for 20 top founder-led companies

With the share price up sharply and trading close to analyst targets, the key question now is whether LSB Industries is still trading at a discount to its estimated value or if the market is already pricing in future growth.

Most Popular Narrative: 35% Overvalued

The most popular narrative pegs LSB Industries' fair value at $11.15, which sits below the recent $15.00 share price and frames a debate about what is already priced in.

The company's transition towards higher-margin industrial and upgraded products, along with strategic investments in plant reliability and efficiency, is improving capacity utilization and lowering fixed costs. This is positioning margins and net income for meaningful expansion.

LSB is advancing a low-carbon ammonia/CO2 capture project at El Dorado and is poised to supply decarbonized solutions, aligning with increasing customer and policy preference for clean energy and low-carbon chemicals. This could unlock new revenue streams and enhance long-term earnings visibility.

Want to see what is driving that valuation gap? The narrative leans on measured revenue growth, firmer margins, and a richer future earnings multiple to bridge today’s price to fair value.

Result: Fair Value of $11.15 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you still need to weigh exposure to natural gas price swings and ongoing heavy capital spending, either of which could pressure margins and cash generation.

Find out about the key risks to this LSB Industries narrative.

Another View: Cash Flows Point in a Different Direction

While the popular narrative sees LSB Industries as 35% overvalued on an earnings multiple approach, the SWS DCF model paints a different picture, with fair value at $17.43 versus the current $15.00. This suggests the market may be pricing future cash flows more cautiously than that model implies.

For investors, the question is which lens feels more realistic: the earnings based fair value of $11.15 or a cash flow based estimate above the current price.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out LSB Industries for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 62 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With both upside potential and clear risks on the table, sentiment around LSB Industries is understandably split, so move quickly, review the numbers for yourself, and weigh the 2 key rewards and 2 important warning signs

Looking for more investment ideas?

If LSB Industries has you thinking about what else might be out there, do not stop here. Widen your watchlist and give yourself more options.

- Explore stocks with reliable payouts and cash flows using the 13 dividend fortresses

- Review companies that may be mispriced on fundamentals with the 62 high quality undervalued stocks

- Find under the radar opportunities before they attract wider attention using the screener containing 25 high quality undiscovered gems

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com