- If you are wondering whether NextEra Energy's share price still offers value, you are not alone. This is especially true with the stock firmly on many investors' watchlists.

- The shares last closed at US$92.73, with returns of 0.7% over 7 days, 1.9% over 30 days, 14.6% year to date and 46.8% over the past year. This naturally raises questions about what is already priced in.

- Recent coverage of the utilities sector has continued to highlight large, established names like NextEra Energy, keeping the company in focus for investors comparing options within the space. At the same time, broader discussions about interest rates and income-oriented assets provide extra context for how investors may be weighing regulated utilities against other yield and growth choices.

- Simply Wall St currently gives NextEra Energy a valuation score of 1 out of 6. The rest of this article will break down what different valuation methods say about the stock and suggest a more complete way to think about value that ties those methods together at the end.

NextEra Energy scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

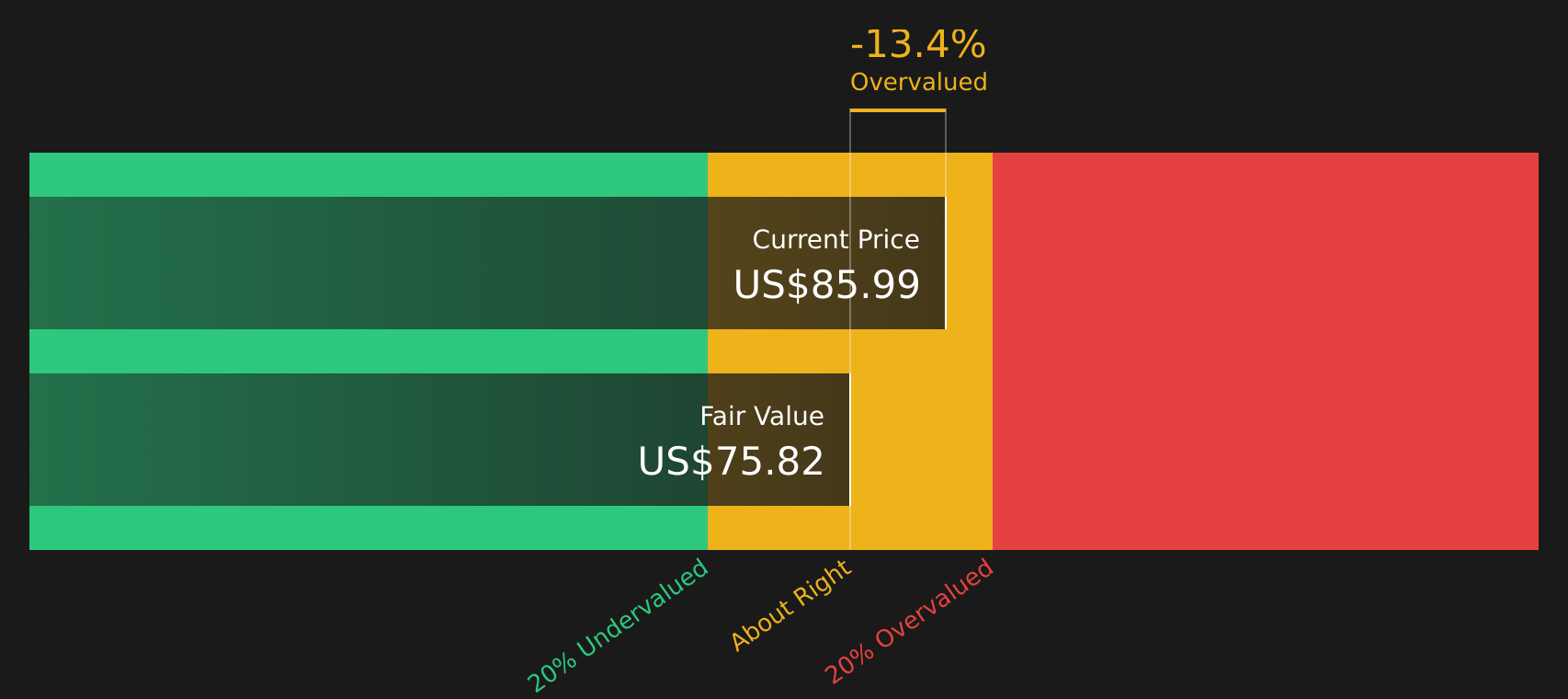

Approach 1: NextEra Energy Dividend Discount Model (DDM) Analysis

The Dividend Discount Model estimates what a stock could be worth by projecting future dividends and discounting them back to today, then comparing that figure with the current share price.

For NextEra Energy, the DDM uses a dividend per share of US$2.73, a return on equity of 9.51% and a payout ratio of about 61%. Simply Wall St caps the dividend growth rate at 3.41%, slightly below the model’s expected growth of about 3.71%. This keeps the focus on a level of growth that appears aligned with current profitability and payout levels, rather than assuming more aggressive expansion.

Based on these inputs, the model arrives at an estimated intrinsic value of about US$76.53 per share. Compared with the recent share price of US$92.73, this implies the stock is around 21.2% overvalued according to this single dividend based lens. For income focused investors, that suggests the current price already reflects a relatively optimistic view of future payouts.

Result: OVERVALUED

Our Dividend Discount Model (DDM) analysis suggests NextEra Energy may be overvalued by 21.2%. Discover 62 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: NextEra Energy Price vs Earnings

For profitable companies, the P/E ratio is a useful way to think about value because it links what you pay for each share directly to the earnings that business is currently generating.

What counts as a “normal” P/E often reflects how the market views a company’s growth potential and risk profile. Higher expected growth or lower perceived risk can justify a higher multiple, while slower growth or higher risk typically lines up with a lower P/E.

NextEra Energy currently trades on a P/E of 28.29x. That is above the Electric Utilities industry average P/E of 21.92x and also above the peer group average of 27.22x, so the stock is priced at a premium when you compare it with broad sector and peer benchmarks.

Simply Wall St’s Fair Ratio for NextEra Energy is 30.40x. This is a proprietary estimate of what the P/E might be given the company’s earnings growth profile, profit margin, industry, market cap and specific risks. Because it blends these company level drivers with sector context, the Fair Ratio can be more tailored than a simple comparison with industry or peer averages.

With the actual P/E of 28.29x sitting below the Fair Ratio of 30.40x, the stock screens as UNDERVALUED on this multiple based view.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your NextEra Energy Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives bring your view of NextEra Energy together in one simple story that links what you think about its future revenue, earnings and margins to a forecast and then to a Fair Value that you can compare with today’s price.

On Simply Wall St’s Community page, Narratives are an accessible tool used by millions of investors where you set assumptions, add your reasoning in plain language, and instantly see how your story translates into numbers.

This helps you decide whether NextEra Energy looks attractive or stretched for you personally, because you are comparing your Fair Value output with the live share price rather than relying only on headline multiples.

Narratives also update automatically when new information such as earnings or news is added to the platform, so your Fair Value view keeps moving with the company instead of staying frozen at the moment you first ran the numbers.

For example, one optimistic NextEra Energy Narrative links a Fair Value of US$111.0 per share to assumptions about stronger revenue growth and a 27.0x future P/E. A more cautious Narrative points to a Fair Value of about US$70.22 based on slower revenue growth and an 18.7x future P/E. Comparing both ranges with the current market price shows how different perspectives can coexist and helps you decide which story feels more realistic for you.

For NextEra Energy, however, we will make it really easy for you with previews of two leading NextEra Energy Narratives:

Fair value used in this bullish narrative: US$93.65 per share.

At the last close of US$92.73, that implies the shares are about 1.0% below this Fair Value estimate.

Revenue growth assumption in this narrative: 10.09% a year.

- Analysts in this narrative expect strong power demand, including from data centers, to support higher revenue and margins over time.

- The story emphasizes renewables scale, storage, and grid investment as potential supports for long term earnings and cash flows while managing policy and execution risks.

- The Fair Value of US$93.65 sits close to the current price, so the appeal depends on how much confidence you have in these growth and profitability assumptions.

Fair value used in this cautious narrative: US$70.22 per share.

At the last close of US$92.73, that implies the shares are about 32.0% above this Fair Value estimate.

Revenue growth assumption in this narrative: 4.87% a year.

- This narrative places more emphasis on expiring tax credits, higher financing costs, and tighter regulation as constraints on future project returns.

- It also highlights high debt levels and the rise of distributed energy resources as possible headwinds for traditional utility earnings and dividend growth expectations.

- With a Fair Value of US$70.22 sitting well below the current price, the focus is on the risk that market expectations for growth and valuation may be too optimistic.

Do you think there's more to the story for NextEra Energy? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com