- In March 2026, Tapcheck Inc. announced an agreement with Paychex, Inc. to embed real-time earned wage access into the Paychex HR PEO platform, allowing eligible employees to move a portion of earned pay instantly via the Tapcheck app or a free Tapcheck Mastercard.

- By tightly integrating on-demand pay with existing payroll data and controls, Paychex is strengthening its financial wellness offering while giving PEO clients a low-friction tool to compete for and retain staff in complex, high-turnover industries.

- Next, we’ll examine how this embedded on-demand pay capability could influence Paychex’s investment narrative around technology-led HR services.

AI is about to change healthcare. These 37 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

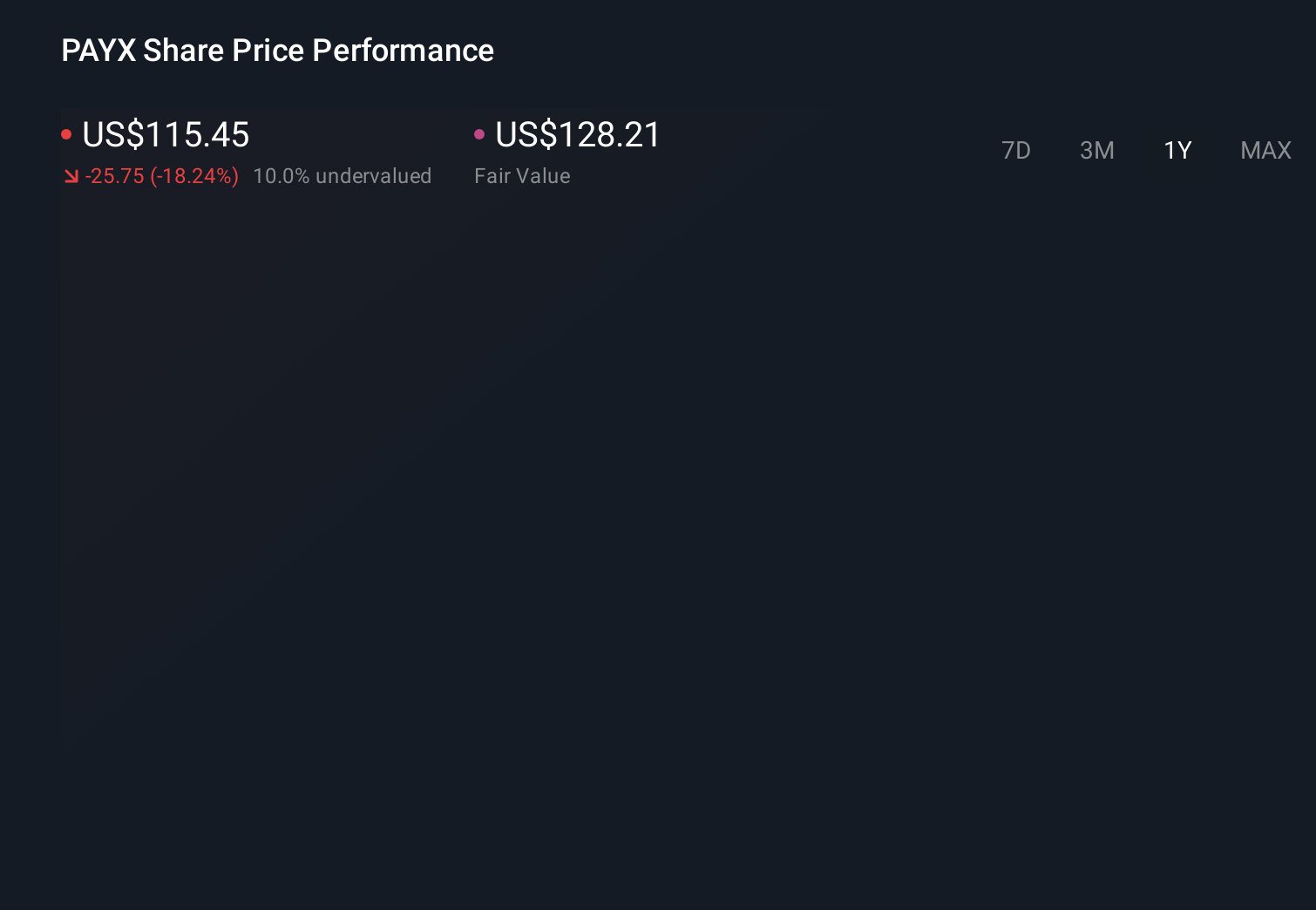

Paychex Investment Narrative Recap

To own Paychex, you need to believe in its ability to deepen client relationships through technology-led HR and payroll services while managing integration and margin pressures. The Tapcheck earned wage access deal underlines that thesis by layering financial wellness tools into the PEO offering, but it does not materially change the near term focus on Paycor integration benefits as a key catalyst, or the risk that softer client behavior and shifting health plan choices could keep pressure on revenue per client and margins.

The most relevant recent announcement alongside the Tapcheck news is Paychex’s March 2026 earnings release, which showed Q3 revenue of US$1,808.9 million and net income of US$560.3 million. These results give you a concrete snapshot of how the business is performing today while Paychex invests in AI, PEO enhancements and Paycor integration, helping you judge whether technology upgrades like embedded on-demand pay are translating into resilient profitability and supporting the current buyback activity.

Yet despite these product wins, investors should be aware that softer deal sizes and more price sensitive clients could still...

Read the full narrative on Paychex (it's free!)

Paychex's narrative projects $7.5 billion revenue and $2.3 billion earnings by 2029.

Uncover how Paychex's forecasts yield a $102.80 fair value, a 12% upside to its current price.

Exploring Other Perspectives

More optimistic analysts saw Tapcheck style innovations fitting into a bigger story, with revenue projected at about US$7.8 billion and earnings near US$2.5 billion by 2029, even as they flagged that heavy AI spending might fail to translate into the differentiated products and margin lift you would need to justify those higher expectations.

Explore 7 other fair value estimates on Paychex - why the stock might be worth just $90.00!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Paychex research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Paychex research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Paychex's overall financial health at a glance.

Looking For Alternative Opportunities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com