Why Golar LNG Is On Investors’ Radar Today

Golar LNG (GLNG) has attracted fresh attention after a strong recent run in its share price, with gains over the past month and past 3 months prompting investors to reassess the LNG-focused business.

See our latest analysis for Golar LNG.

That recent momentum, including a 30 day share price return of 18.42% and a 90 day share price return of 48.27%, sits alongside a very strong 1 year total shareholder return of 76.06% and a multi year track record that some investors may see as evidence of building confidence in Golar LNG’s LNG infrastructure model.

If this kind of move has you thinking about what else is out there in energy related names, it might be a good time to widen your search using the 27 power grid technology and infrastructure stocks

With the shares at US$55.75 and trading at a discount to one intrinsic value estimate of around 46%, yet sitting above the average analyst price target, is there still a clear opportunity here or is the market already pricing in the growth story?

Most Popular Narrative: 6.1% Overvalued

At $55.75, Golar LNG is trading modestly above the most followed fair value estimate of $52.56, which is built on detailed long term FLNG contract assumptions and cash flow projections using a 6.98% discount rate.

The company has secured long-term (20-year) charters for its existing FLNG units, providing $17 billion in contracted EBITDA backlog and 20 years of cash flow visibility, which is expected to drive a significant (4x) increase in EBITDA and contracted free cash flow by 2028, indicating the market may be undervaluing its forward earnings stability and revenue growth.

Want to see what kind of revenue ramp, margin expansion, and earnings multiple are baked into that story? The narrative spells out a bold earnings path and a richer valuation profile than many traditional oil and gas names. The real question is how those assumptions stack up against your own expectations.

Result: Fair Value of $52.56 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on LNG demand and contract stability, and setbacks around new FLNG projects or major counterparties could quickly challenge that earnings and valuation story.

Find out about the key risks to this Golar LNG narrative.

Another View: Cash Flow Paints A Different Picture

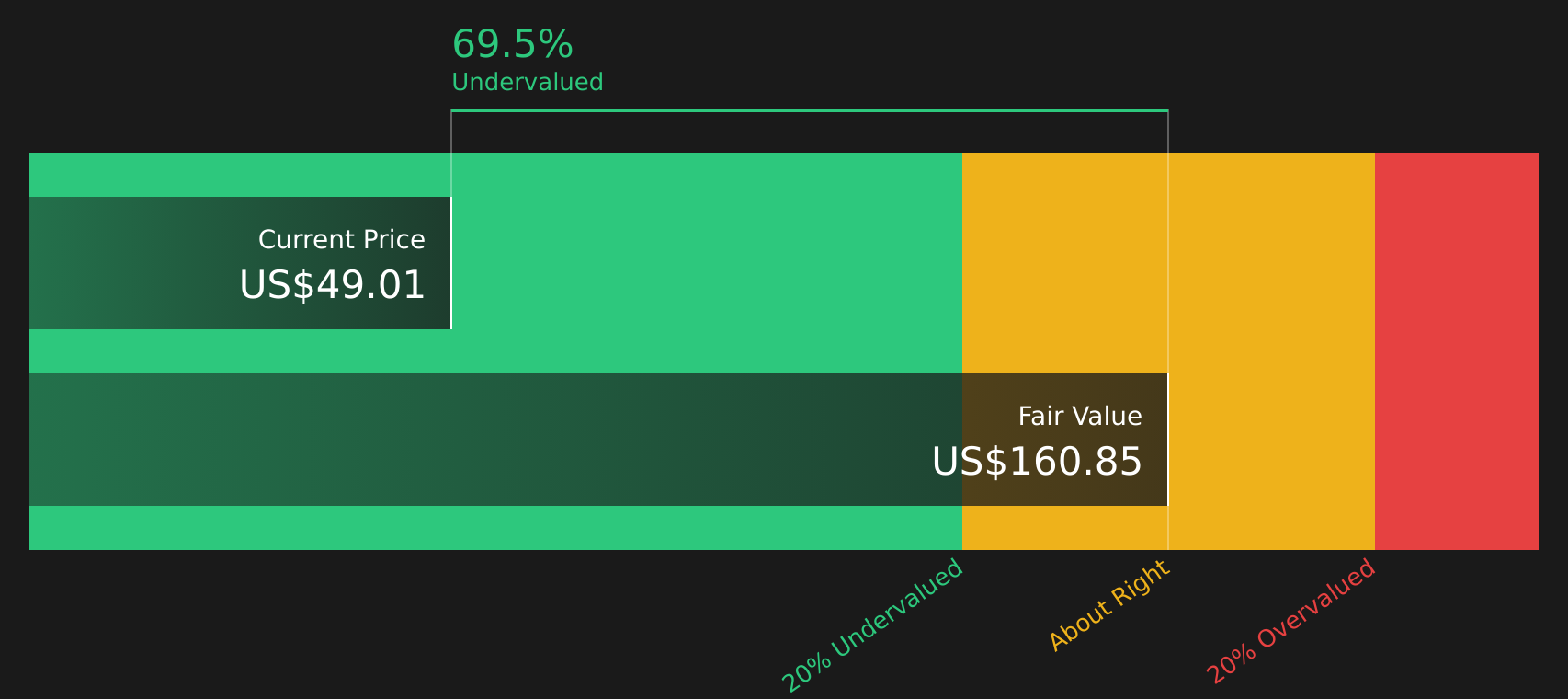

The analyst consensus points to Golar LNG being 6.1% overvalued at US$55.75 versus a fair value of US$52.56, but our DCF model tells a very different story. On that view, the shares sit around 45.8% below an estimated cash flow value of US$102.93, which is a wide gap for you to weigh.

This kind of split between a P/E based target and a cash flow driven model raises a simple question for you as an investor: which lens do you trust more when the story hinges on long term FLNG contracts and project execution?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Golar LNG for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 62 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of enthusiasm and caution has you thinking more critically about Golar LNG, it makes sense to move quickly, test the story against your own expectations, and then weigh both sides by checking the 3 key rewards and 3 important warning signs

Looking for more investment ideas?

If Golar LNG has caught your attention, do not stop here. Some of the most compelling opportunities often sit just outside the headlines you already know.

- Target proven cash generators by running a focused search across 62 high quality undervalued stocks that pair solid fundamentals with prices that may not fully reflect their strengths.

- Strengthen the income side of your portfolio by reviewing 13 dividend fortresses built around higher yielding companies that still prioritize resilience.

- Prioritize peace of mind by filtering for 68 resilient stocks with low risk scores where balance sheets and risk profiles are built to handle tougher conditions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com