The United States market has shown robust performance, climbing 1.2% in the last 7 days and up 33% over the past year, with earnings forecasted to grow by 16% annually. In this thriving environment, identifying stocks that are potentially undervalued can offer opportunities for investors seeking to capitalize on growth prospects while maintaining a focus on value.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Roku (ROKU) | $98.53 | $193.42 | 49.1% |

| National Bank Holdings (NBHC) | $40.12 | $79.88 | 49.8% |

| Kimberly-Clark (KMB) | $93.05 | $184.93 | 49.7% |

| Intuitive Machines (LUNR) | $22.73 | $44.62 | 49.1% |

| Intapp (INTA) | $24.75 | $49.32 | 49.8% |

| Fluence Energy (FLNC) | $13.25 | $26.14 | 49.3% |

| First Busey (BUSE) | $25.93 | $51.67 | 49.8% |

| Ellington Financial (EFC) | $12.05 | $23.89 | 49.6% |

| DNOW (DNOW) | $12.28 | $24.12 | 49.1% |

| Caris Life Sciences (CAI) | $18.75 | $37.23 | 49.6% |

We'll examine a selection from our screener results.

Crocs (CROX)

Overview: Crocs, Inc. designs, manufactures, and sells casual lifestyle footwear and accessories under the Crocs and HEYDUDE brands globally, with a market cap of approximately $4.47 billion.

Operations: The company generates revenue through its Crocs Brand, contributing $3.33 billion, and the Heydude Brand, accounting for $714.84 million.

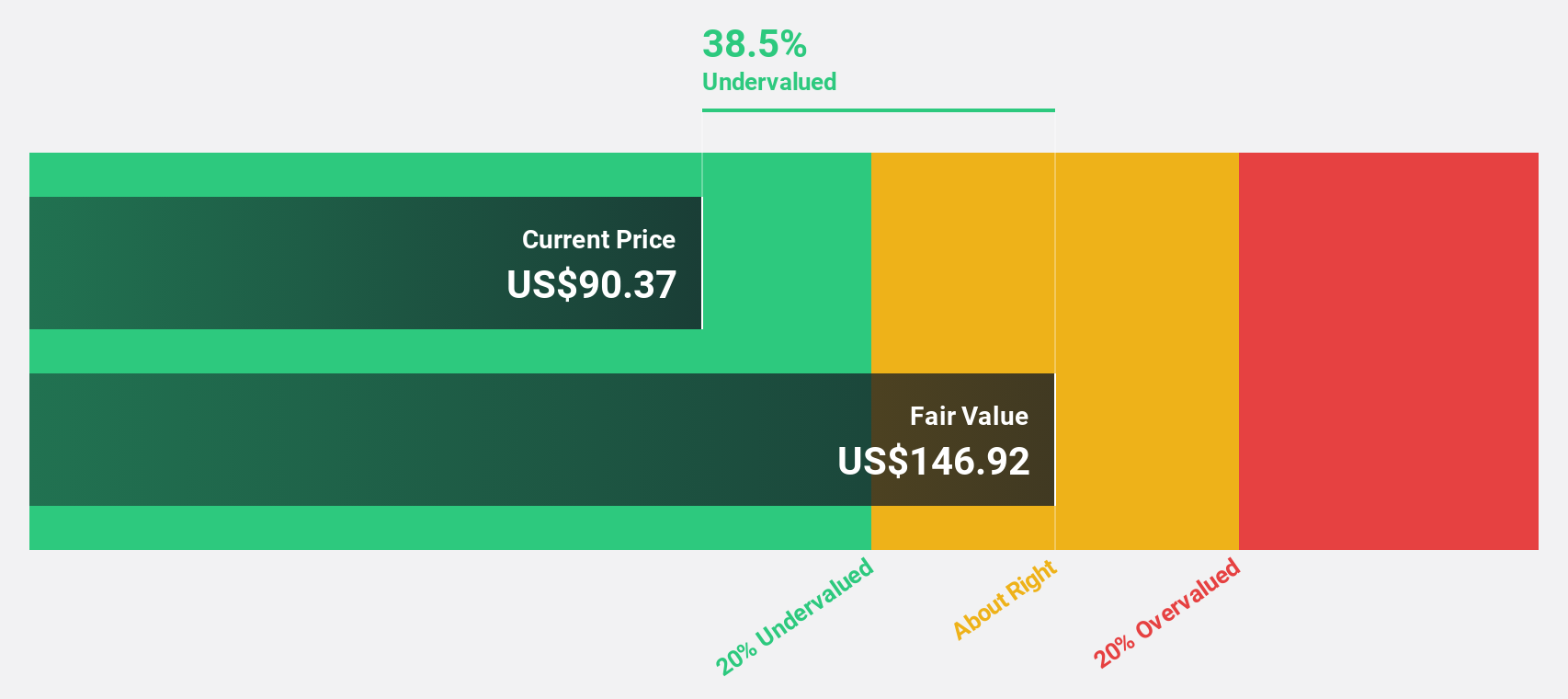

Estimated Discount To Fair Value: 43.1%

Crocs is trading significantly below its estimated future cash flow value, with a current price of US$90.47 against an estimated value of US$158.95, presenting it as undervalued based on discounted cash flows. Despite recent financial challenges, including a net loss for 2025 and slower revenue growth forecasts than the market average, the company has completed a substantial share buyback program worth nearly US$3 billion, potentially enhancing shareholder value in the long term.

- The growth report we've compiled suggests that Crocs' future prospects could be on the up.

- Delve into the full analysis health report here for a deeper understanding of Crocs.

Zscaler (ZS)

Overview: Zscaler, Inc. is a global cloud security company with a market capitalization of approximately $22.43 billion.

Operations: The company generates revenue primarily through the sale of subscription services to its cloud platform and related support services, amounting to $3.00 billion.

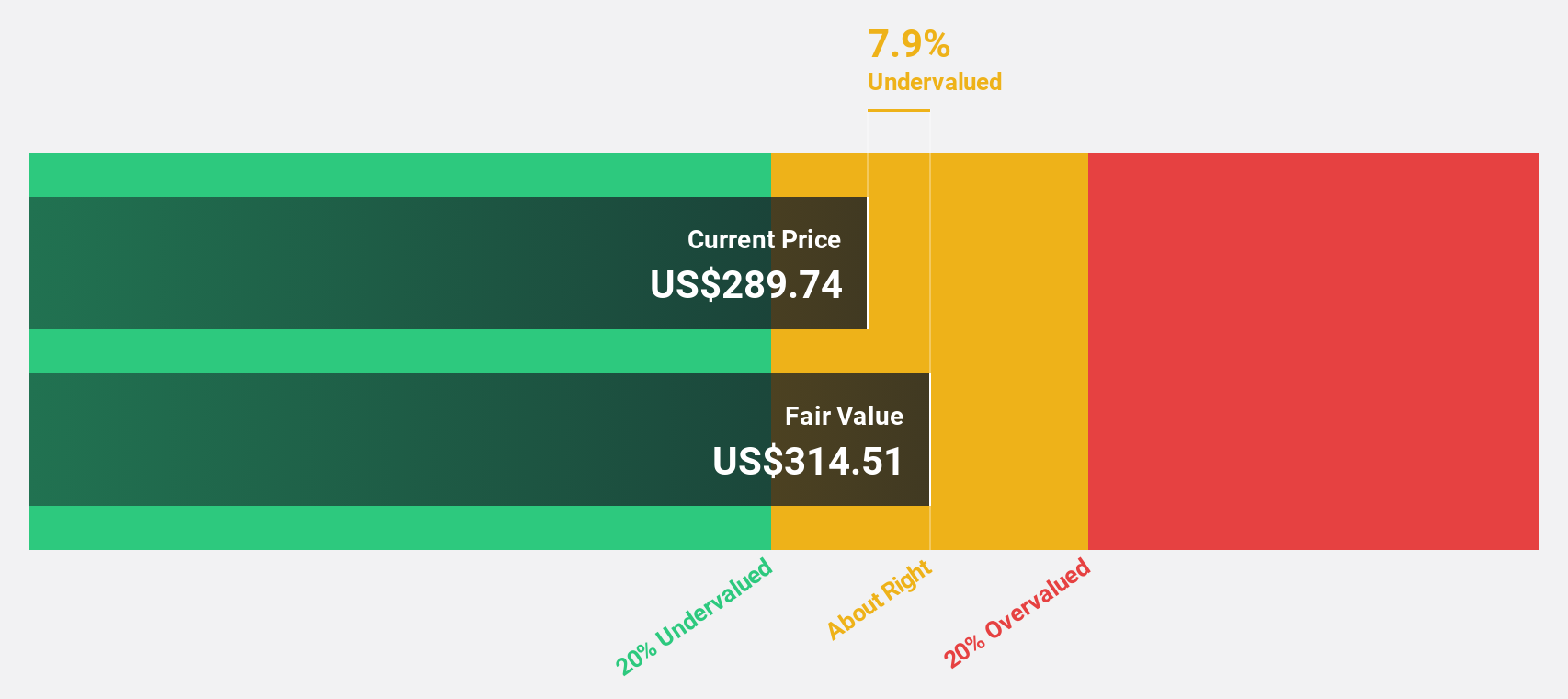

Estimated Discount To Fair Value: 39.4%

Zscaler is trading well below its estimated future cash flow value, with a current price of US$142.09 compared to an estimated value of US$234.55, highlighting its undervaluation based on discounted cash flows. Despite recent net losses and insider selling, Zscaler's revenue growth forecast surpasses the broader market at 15.9% annually. Strategic partnerships and technology alliances bolster its position in cloud security, potentially supporting long-term profitability as it aims to become profitable within three years.

- Our expertly prepared growth report on Zscaler implies its future financial outlook may be stronger than recent results.

- Take a closer look at Zscaler's balance sheet health here in our report.

Clear Secure (YOU)

Overview: Clear Secure, Inc. operates a secure identity platform under the CLEAR brand name primarily in the United States and has a market cap of approximately $6.90 billion.

Operations: The company's revenue is primarily derived from its Secure Biometric Identity Verification segment, which generated approximately $900.78 million.

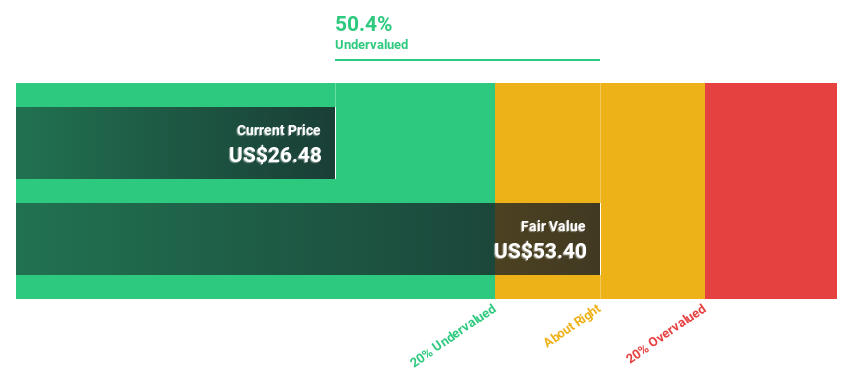

Estimated Discount To Fair Value: 48%

Clear Secure is significantly undervalued, trading at US$52.62 against a future cash flow value of US$101.22. Despite a decrease in profit margins from 22% to 12.1%, its earnings are projected to grow by 23.7% annually, outpacing the broader U.S. market's growth rate of 15.5%. Recent partnerships with healthcare systems like Ochsner Health and Mount Sinai enhance its identity platform's adoption, potentially driving further revenue growth and operational efficiency improvements across sectors.

- In light of our recent growth report, it seems possible that Clear Secure's financial performance will exceed current levels.

- Click here to discover the nuances of Clear Secure with our detailed financial health report.

Turning Ideas Into Actions

- Dive into all 158 of the Undervalued US Stocks Based On Cash Flows we have identified here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com