CIBC Capital Markets’ Q1/26 solid waste earnings preview puts Waste Management (WM) in focus, as the firm highlights sector resilience tied to inflation-plus pricing, margin expansion, AI-driven productivity and ongoing M&A activity.

See our latest analysis for Waste Management.

At a share price of US$233.31, Waste Management has seen an 8.03% 90 day share price return and a 9.41% 1 year total shareholder return. This performance suggests momentum that aligns with renewed interest following CIBC’s sector preview.

If you want to see how other infrastructure heavy names are moving alongside WM, this is a good moment to scan for 28 power grid technology and infrastructure stocks

With WM trading at US$233.31 and priced only modestly below some valuation estimates, investors are left asking whether current strength still leaves room for upside or if the market is already incorporating future growth expectations.

Most Popular Narrative: 8% Undervalued

Simply Wall St’s most followed narrative places Waste Management’s fair value at $253.12, a premium to the last close of $233.31 that frames the current setup clearly.

The company's strategic investments in sustainability, particularly in the areas of recycling and renewable energy, are showing strong, high-return growth, which could drive future revenue increases. The integration and optimization of WM Healthcare Solutions are on track to deliver significant synergies, anticipated to reach $250 million annually by 2027, positively impacting earnings.

Curious what kind of revenue glide path and profit margin shift are baked into that $253.12 figure? The narrative ties them to a rich earnings multiple and long term cash flow profile that many would usually associate with faster growing sectors.

Result: Fair Value of $253.12 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upside story still depends on tax credits and regulation staying supportive, as well as on the Stericycle acquisition bedding down without unexpected cost or integration issues.

Find out about the key risks to this Waste Management narrative.

Another Angle On Value: P/E Tells A Different Story

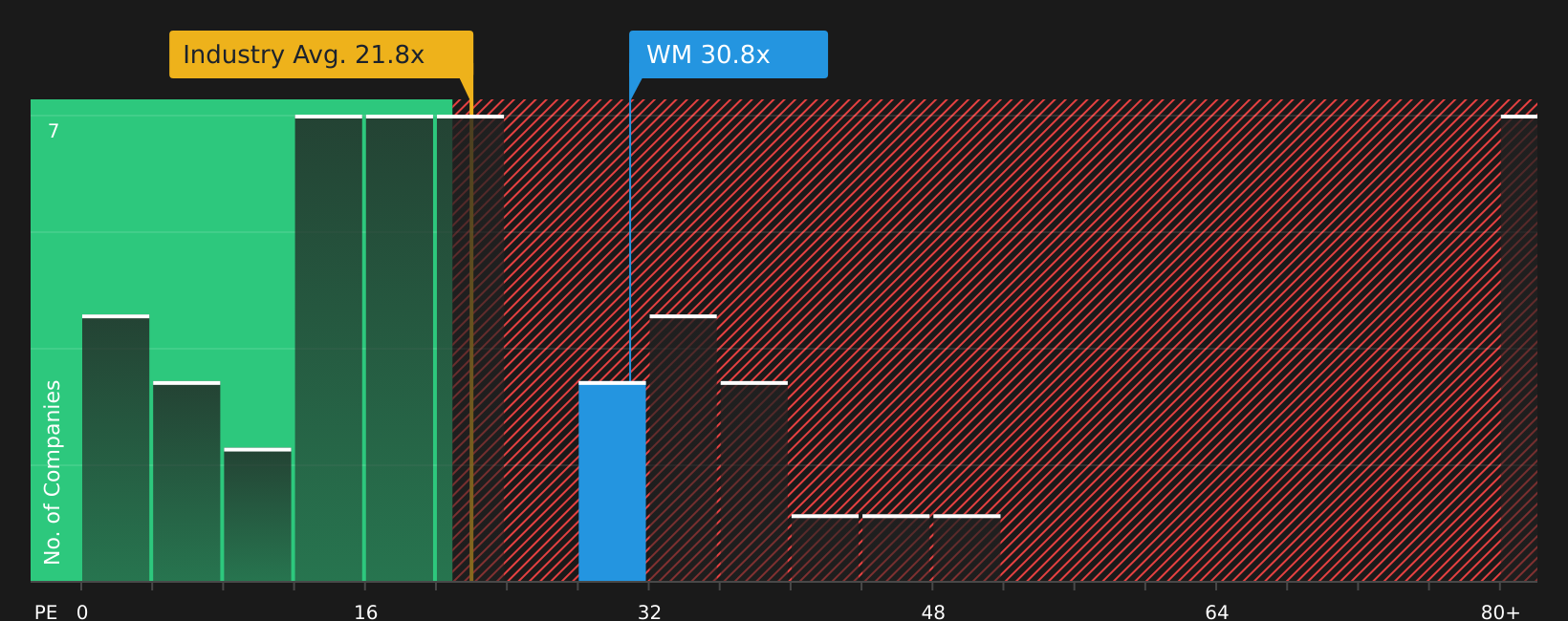

The SWS DCF model suggests WM at $233.31 is about 3.7% below an estimate of future cash flow value of $242.32, which points to a mild undervaluation. Yet on earnings, WM trades on a 34.7x P/E versus a fair ratio of 30.3x and a US Commercial Services average of 22.9x.

In practical terms, that means you are paying more for each dollar of earnings than both the modelled fair ratio and the wider industry. This raises a simple question: is that premium a comfort or a risk for you at this price?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Torn between the upbeat valuation signals and the premiums you are paying today? Take a closer look at the full picture with 3 key rewards and 2 important warning signs

Looking for more investment ideas?

Do not stop your research with a single name. Broaden your watchlist with focused stock ideas that match the kind of portfolio you actually want to build.

- Target quality at a discount by scanning a curated pool of companies that screen as attractively priced using the 61 high quality undervalued stocks.

- Strengthen your passive income plans by reviewing income plays that appear in the 13 dividend fortresses.

- Reduce portfolio stress by concentrating on companies that appear in the 70 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com