Recent share performance snapshot

United Parcel Service (UPS) shares recently closed at US$97.57, with a 0.4% gain on the day. The stock has recorded negative returns over the past week, month, and past 3 months, alongside a 13.4% total return over the past year.

See our latest analysis for United Parcel Service.

The recent 1-day share price gain sits against weaker short term share price returns over the past quarter. The 1-year total shareholder return of 13.4% also contrasts with much weaker 3 and 5-year total shareholder returns, suggesting longer term momentum has faded.

If you are reassessing UPS alongside other opportunities in logistics and infrastructure, it can be useful to see which related names are attracting interest through the 28 power grid technology and infrastructure stocks

UPS now trades at US$97.57, with some indicators suggesting a potential discount while recent returns remain uneven. Is this a genuine value opportunity, or is the market already factoring in expectations for future growth?

Most Popular Narrative: 2.5% Overvalued

According to NVF's widely followed narrative, UPS's fair value sits at $95.21, slightly below the last close at $97.57, which frames a modest premium.

We believe in a cautious approach in our analysis as UPS has been clouded with sustainability issues, higher costs, and internal headwinds. Can UPS navigate financial and operational pressures with resilience? Launched in early 2025, UPS's "Efficiency Reimagined" outlined the company’s largest network overhaul in company history. This multi-year initiative details management's goals to streamline domestic operations.

Read the complete narrative. Read the complete narrative.

Want the full story behind that $95.21 fair value? The narrative focuses on measured revenue expansion, firmer margins, and a higher earnings multiple by 2028. Curious which assumptions really move that valuation and how they balance new debt against profit potential?

Result: Fair Value of $95.21 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this story can shift quickly if cost cuts disrupt service quality, or if union tensions resurface in a way that pressures margins and cash flow assumptions.

Find out about the key risks to this United Parcel Service narrative.

Another angle on value

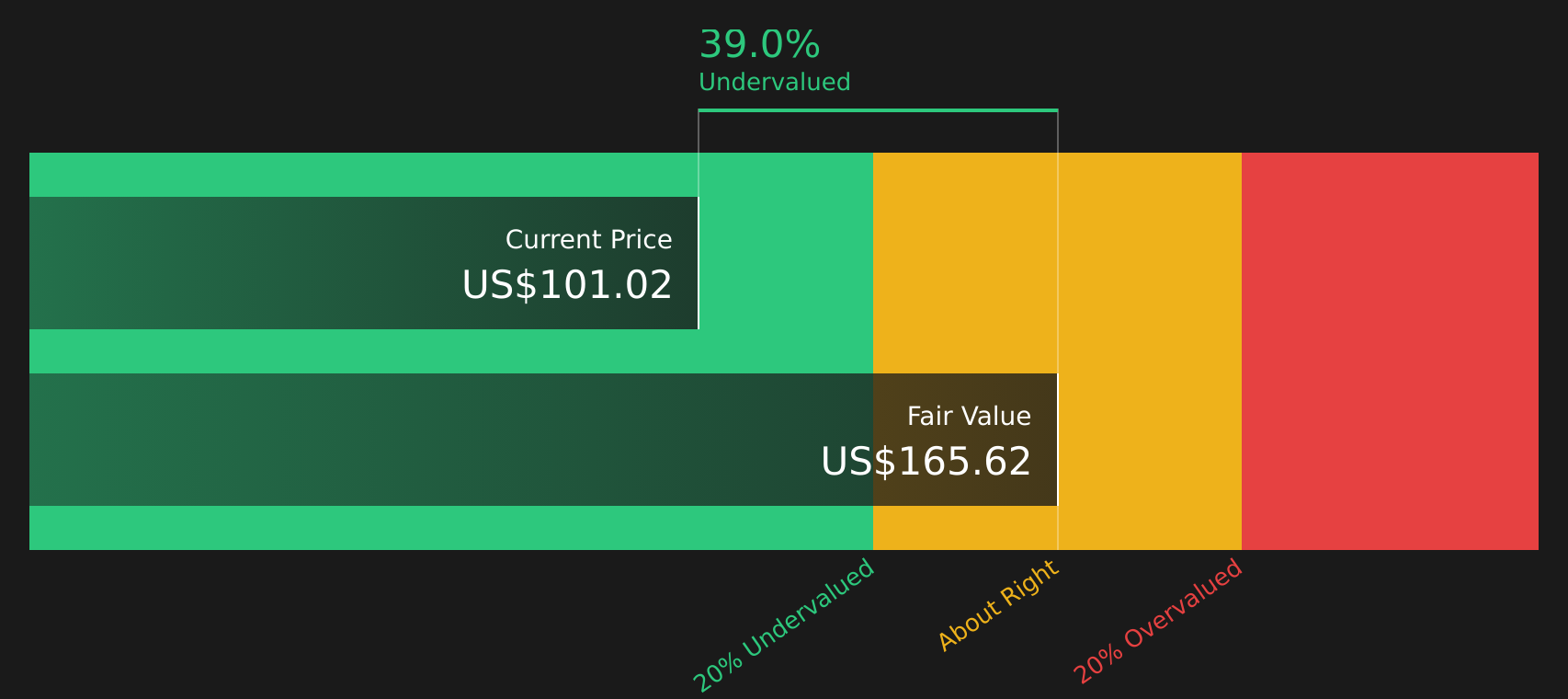

That 2.5% premium to the $95.21 fair value is based on one narrative model using earnings and assumptions out to 2028. Our DCF model tells a very different story, with an estimated future cash flow value of $166 per share, which implies UPS is trading at a large discount. Which version of “fair” do you lean toward?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

With the mixed signals in this UPS story, now is the moment to look through the details yourself and decide what really matters. To get a clear view of both the upside and the concerns investors are watching, start with these 3 key rewards and 3 important warning signs

Looking for more investment ideas?

If UPS has you thinking harder about where to put your money next, do not stop here. The market is full of other opportunities waiting for a closer look.

- Target companies that combine healthy cash generation with attractive prices by checking out 61 high quality undervalued stocks.

- Prioritise strength and resilience by scanning the solid balance sheet and fundamentals stocks screener (40 results) before the next bout of volatility catches you off guard.

- Get ahead of the crowd by reviewing a focused screener containing 25 high quality undiscovered gems that could slip past investors who only follow the headlines.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com